BMO and its advisors are getting sued by clients. In the article, it claims the advisor in question in 2017 and the first half of 2018 traded on behalf of clients a leveraged short treasury, long preferred share strategy.

Both client groups allege that throughout 2017 and the first half of 2018, Mr. Liu recommended a new investment strategy that “assured safety” of their principal and provided “reasonable” investment returns.

Shortly after, clients allege they were instead placed in a high-risk strategy that involved short-selling bonds – particularly Canadian government bonds – to purchase long positions in preferred shares, many of which had variable rates or rates that reset based on interest rate movement.

According to court documents, Mr. Liu further advised the clients to begin trading on margin – investing using borrowed money – in order to purchase a larger amount of preferred shares. In some instances, clients allege Mr. Liu engaged in this strategy without informing them or seeking their permission.

I’d love to read the court documents.

I’m guessing the pitch was that you could borrow around 1.5-2.0% (short treasuries) and re-invest the proceeds in (relatively high quality rate reset) preferred shares yielding around 5-5.5%. Just throw in some cash and we can leverage this thing 5:1 and earn you a cool 15% return on equity. Sounds great!

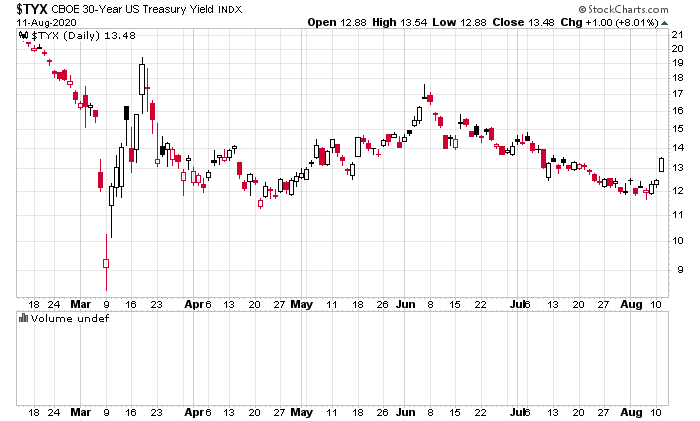

Canada’s 5 year bonds in the first half of 2017 spent most of their time around 100-125bps, and the second half around 150-175bps. In the first half of 2018, they were at 200-225bps. So this pair of the trade would have surely lost money, but it would have been more than offset by appreciation of the preferred shares. In fact, during 2017, the trade would have looked really good and I would not be shocked if clients added more money to it:

The second leg of the trade (preferred shares) didn’t do that badly until about the fourth quarter of 2018, where preferred shares lost about 15% of their capital value. The bonds during this time would have appreciated somewhat, but depending on the amount of leverage employed, the trade would have been a significantly losing one. By the third quarter of 2019, the preferred shares would have declined another 10%.

I’m guessing it would have been after the 4th quarter in 2018 that clients came asking why they were seeing negative returns in their accounts. “Oh, don’t worry, these are normal market fluctuations, just look at the yields you’re getting!”. By the time the third quarter in 2019 came along, it looks like client losses would have been another 10% times whatever leverage factor they engaged in.

Back in June 2019 I mused about this, but it looks like others actually engaged in this trade, which is a classic example of leveraged yield chasing! It rarely ends up well unless if you close out the trade when you least want to – when the trade is working.