The last two weeks of summer, psychologically speaking, are the two weeks before labour day weekend. Families are still on holiday (whatever types of holidays are still available with the myriad of Covid-related disruption around us), children are not at school, and the weather is usually warm enough that one wants to stay outside before the big Canadian winter freeze commences.

In the markets, this also means institutional managers are in the same boat – major policy decisions on how to steer the computerized program trading will likely be made after labour day.

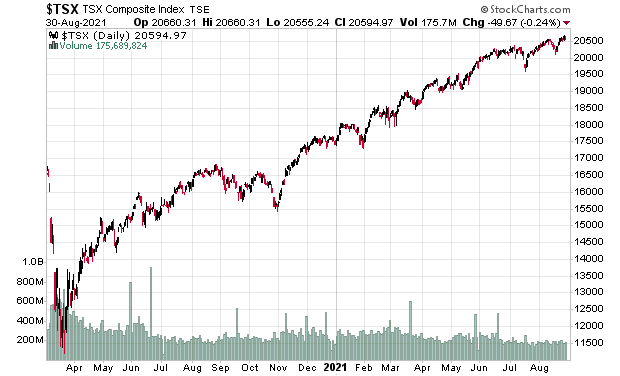

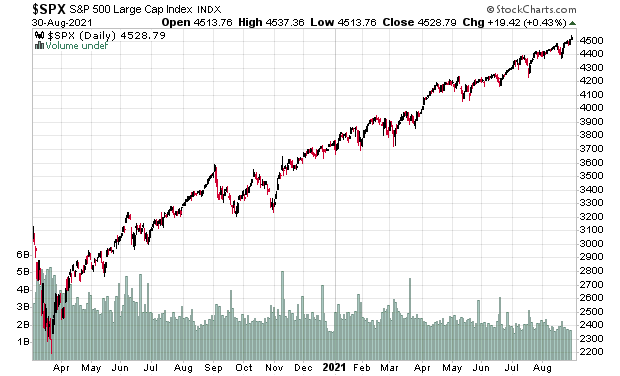

So I do not put much stock in market action that is occurring, other than to observe that the TSX and S&P 500 is at an all-time high:

The Nasdaq 100 is also the same way. Both US indexes are a functional proxy for Apple, Microsoft, Amazon, etc. The S&P 500’s top 10 is about 28% of the index, while the Nasdaq 100’s top 10 is just over 50% of the index.

The TSX’s top 10 are: SHOP, RY, TD, BAM.A, ENB, CNR, BNS, BMO, CN and CP. They are about 40% of the index.

You would think the markets reaching all-time highs would generate some news headlines. It has been exactly the opposite. What do we hear about today?

1. Disaster in Afghanistan

2. Disaster in Covid-19 (take your pick: vaccines not working, variants, travel curbs, ‘fourth wave’, etc.)

3. Disaster in supply chains

4. Disaster in climate (take your pick: hurricanes, wildfires, droughts, heat waves, etc.)

5. Disaster in the Liberal Party of Canada (OK, OK, this was a joke – I will write about the Canadian election later)

The one thing that has clearly NOT been a disaster are people that have their capital in return-bearing assets. Indeed, it has been a disaster if you were NOT in the markets. The TSX is up about 17% year-to-date, while the S&P is up 21%. If you’re lagging this number, you’re effectively ‘falling behind’.

This rise in the stock market continues to be fuelled by monetary policy, with the USA and Canadian central banks still vacuuming up treasury bonds like no tomorrow; and also fiscal policy, with both governments spending like crazy.

The cash will circulate in the economy until the point where it ends up locked in bank reserves, which currently earns a very low rate of interest and will continue to do so for the indefinite future. Individuals that have satisfied their material needs have no other choice but to put their capital into the asset markets, lest they lose purchasing power.

This is the market we have been seeing post-COVID-19, until at such point we do not.

We are well into seeing the price ramifications in this monetary/fiscal regime. The front-row-center for many is the elevated cost of residential housing in urban centers. Indeed, even second and third-tier cities/towns have had an influx of capital just simply because of the people escaping the urban centres. Because of the elevation of such asset pricing, correspondingly, the cost of everything else rises to bake in the extra capital required to use the land.

We also see the impact on the stock market.

The physical world is where things get interesting with regards to the impact of monetary/fiscal policy. Although most of what happens in finance is a transaction of electrons, the physical world is messy. Primary industries produce the raw materials necessary for the functioning of society, and this includes food, energy and minerals. Somebody needs to produce this. As the debasement of currency continues, it stands to reason that the elevated cost structure will result in these commodity prices elevating.

Almost everything (with the exception of gold and silver) has risen since the start of the Covid pandemic.

The result of the increase in commodity prices will be a price transmission on the physical side of the economy that we will have not seen since the 1970’s. This will likely continue until we see a market dislocation event. I do not know what or how this will take place, but when it occurs, it will be like a 9.0 Richter Scale earthquake right next to where you live. And just like earthquakes, it will be very difficult to predict.

Until then, and especially as the conventional media has completely tuned the masses away from the rising stock market, the major indexes are most likely to continue their existing trajectories.