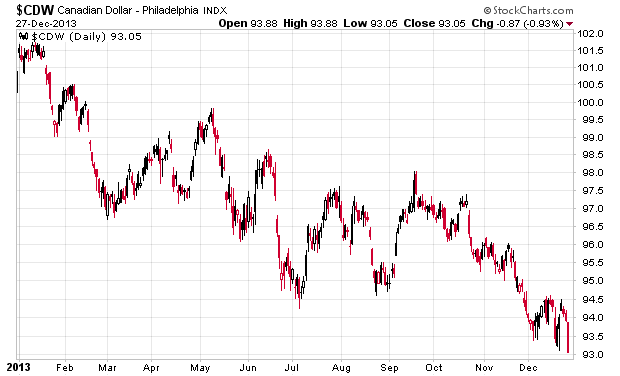

Other than the usual stuff about the S&P 500 being up a huge amount for the year, perhaps the unexpected financial highlight for most Canadians is in the following chart:

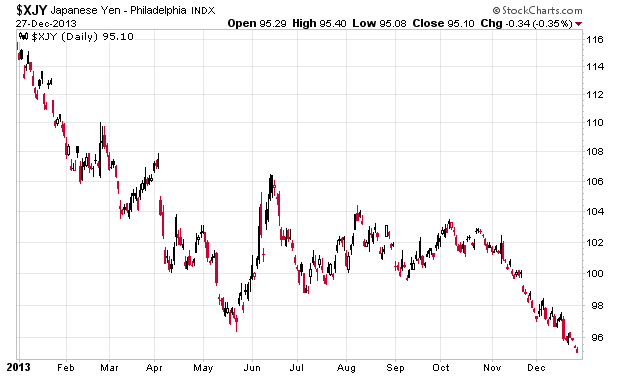

Looking at the other major currencies, the Euro has appreciated slightly against the USD over the year (from US$1.32 to US$1.38 per Euro), while the Yen has weakened considerably, with 87 Yen being one USD at the beginning of the year – now this is 105!

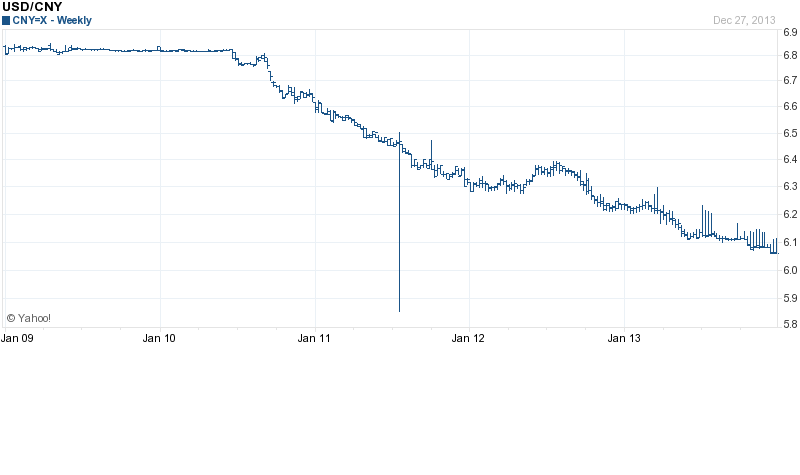

The Chinese Yuan strengthened against the USD of the year, 6.23 CNY per USD, while today it is 6.07. This continues a very slow trend of appreciation for the Chinese currency since they changed their monetary policy since 2010:

Some questions for 2014 will be:

– Will the Canadian dollar continue to downtrend?

– How low will the Yen go before Japan collapses its economy?