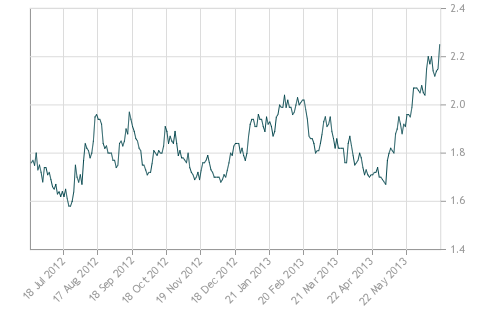

Yields are finally rising. Canadian yields on the 10-year bond:

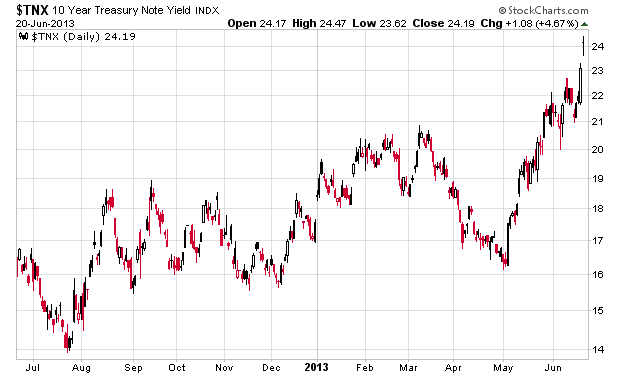

Yield on the 10-year US treasury note:

While this may look dramatic, it should also be noted that yields on the 10-year note in the middle of 2011 was hovering around the 3.2% level, so the current yield of 2.5% isn’t not that high – indeed, it makes the 1.7% range that things were trading at before the spike up appear to be that much more low.

That said, the question remains on how this is going to impact the rest of the credit market, especially the corporate debt market. Spreads between treasuries and BBB-rated type issues are still at relative historic lows and I wonder if we will start to see a pricing of higher spreads once more.

If this is the onset of a market panic to get out of any assets (fixed income, equity, commodity, real estate) then the only safe haven will continue to be zero-yielding cash. The beneficiary in such an instance would be the US dollar.

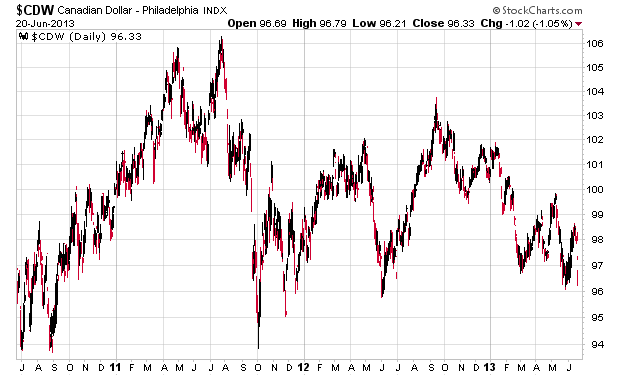

We have the last three years of trading on the Canadian dollar and could this mean a weakening of Canadian currency, relative to the US dollar? Time will tell. I have been more or less positioned 2/3rds in US currency since 2012 so this tells you how I think this is going to be resolving itself.