I do not post about taxation much in this site simply because it is too depressing.

The last analysis I performed was in the last year of the Trudeau administration, where inclusion rates above $250k would be taxed at 2/3rds of regular income instead of the 1/2 it is today. This proposal got delayed to 2026 on January 31, 2025 and formally shelved by Prime Minister Mark Carney on March 21, 2025.

I identified that the big target of this was not necessarily the doctors and lawyers investing through their corporations (although this was certainly a side target), but rather going after estates and situations that were likely to incur large deemed dispositions.

A story was making the rounds a few days ago where the CRA sucked up about $670k of an (inferring from the tax bill and facts reported in the story) approximate $2M estate. The long story short is that a husband and wife died within a year of each other in their early 60’s and they sold their primary residence 5 years earlier and moved to a ‘cottage’ which was held since 1998 and were only able to claim a partial principal residence exemption. The beneficiaries were complaining that the RRSP collapse coupled with the deemed disposition sucked away most of the liquid RRSP cash, leaving the beneficiaries with “nothing” (let’s ignore the fact there is a cottage remaining at a relatively high cost basis).

At a 2/3rds capital gain inclusion rate, the tax bill for them on the deemed disposition of the cottage would have been an extra $100k or so.

My post is not about the ignorance and feigned outrage of having a large amount of money sucked up but rather the manner of taxation that will increasingly be exhibited in the future. Inheritance taxes are going to increase in countries as the baby boomer generation dies off and the demographic inversion accelerates. The amount of wealth that is transferred will be an irresistible target for governments – we already see countries like Japan that will apply 30% marginal rates above CAD$500,000 equivalent and 40% over CAD$1,000,000. In Canada, the deemed disposition of capital assets on death acts as an effective inheritance tax.

It is pretty obvious at this point that governments are quite keen to collecting higher amounts of taxes through inflation.

The other aspect of capital is while dollars and cents in the monetary system are mobile between countries that have free capital controls, if the taxation and/or inflation situation is too punitive, capital will flow out of the jurisdiction in question. The taxation of immovable or geographically locked assets such as land titles and mineral resources will be subject to increasing scrutiny. In Canada, the administration and taxation of land titles is under the provincial jurisdiction and in British Columbia, land titles have been picked away at with the speculation and vacancy tax (essentially a 1% yearly tax on assessed value if you do not occupy or rent it out), the federal underused housing tax (effectively a tax on foreign ownership) and also the elevated “school tax” (an additional property tax levy on properties assessed at more than $3 million).

There is a Laffer curve that applies to taxation on these immobile assets and this is typically indicative of the pricing of these assets. When projected carrying costs of land titles (taxes, insurance, maintenance, and carried interest) increase, it has an effective of decreasing the capitalized value of the property at hand. There is also a reverse causation – a perceived increase in land title value will also trigger increased interest in land titles. In addition to capturing a captive value on land titles (note: this is irrespective of actual assessed value – rates can simply be increased further in times of decreasing net aggregate assessed values), governments in appreciating markets will capture capital gain value, in addition to property transfer taxes.

It is difficult to say when the tax market has been saturated but on the real estate front, it appears we’re getting close to that point, if not exceeded it. Hence, the lever that is being pulled currently is reducing the cost of capital and trying to instigate demand in the asset markets – to increase volume and also to generate those precious capital gains taxes.

We have a federal government that is going to announce a budget on November 4, 2025. It’s no secret that this budget is going to contain a gigantic amount of spending investment.

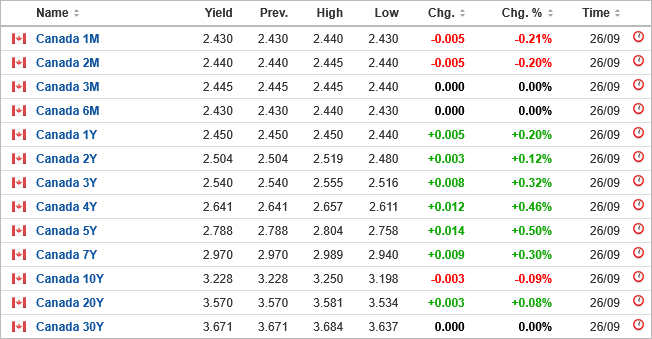

At 3.2% on 10-year government debt, why not? To the government, it is virtually free money. And if you’re one of the institutional fund managers out there looking at the bond offerings, where else are you going to put your capital and clear a 300bps equity risk premium? It will simply be paid for in a hidden manner with debasement. For those saying that Japan’s government pulled it off without causing huge amounts of inflation – different culture! North American culture is much more predisposed of spending and debt.

Did I begin this post by saying I don’t write about taxation too often because it is too depressing?