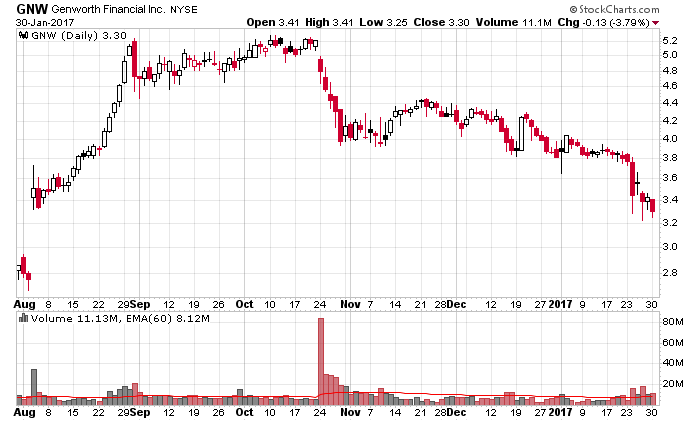

The market is projecting that Genworth’s (NYSE: GNW) US$5.43/share cash merger with China Oceanwide will fail:

The issue revolves around the insurance unit that contains their long-term care insurance liabilities – the theory would be that the Genworth is unlikely to obtain state approvals without taking the full burden of the LTC division.

The salient part of a piece of nearly unreadable verbiage from the finalized merger proxy form is the following:

In addition, it is a condition to the obligations of Asia Pacific and Merger Sub to consummate the merger that certain affiliates of Genworth shall have received regulatory approval (or non-disapproval, in certain instances) from the Delaware Department of Insurance and the Virginia Bureau of Insurance to effect the U.S. Life Restructuring, including the unstacking and the following intercompany reinsurance and recapture transactions between GLAIC and GLIC: (i) a reinsurance transaction pursuant to which GLIC will reinsure certain long-term care insurance business from GLAIC (which we refer to as the “Long Term Care Reinsurance Transaction”); (ii) separate reinsurance transactions pursuant to which GLAIC will reinsure from GLIC (A) certain universal life insurance business and term life insurance business, (B) certain company-owned life insurance business and (C) certain single-premium deferred annuity business, single-premium immediate annuity business, structured settlement annuity business and fixed annuity business (which we refer to as the “Life Restructuring Reinsurance Transactions”); and (iii) a transaction pursuant to which GLIC will recapture from GLAIC certain single-premium deferred annuity business that is currently reinsured by GLAIC from GLIC (which we refer to as the “Recapture Transaction”). GLIC and GLAIC have received approvals for the Long Term Care Reinsurance Transaction from the Delaware Department of Insurance and the Virginia Bureau of Insurance and completed the transaction effective November 1, 2016. Genworth made regulatory filings with respect to the unstacking with the Delaware Department of Insurance on December 21, 2016 and the Virginia Bureau of Insurance on January 3, 2017. Genworth made regulatory filings with respect to the Life Restructuring Reinsurance Transactions and the Recapture Transaction with the Delaware Department of Insurance and the Virginia Bureau of Insurance on December 16, 2016. In addition, the merger agreement provides that Genworth, in consultation with China Oceanwide and applicable insurance regulators, may explore the feasibility of the transfer of GLAIC’s 34.5% ownership interest in GLICNY to GLIC and, if approval from such regulators is received, to pursue such transfer.

If, for whatever reason, you believe these applications will succeed, then there is a very easy method to turn $3.30/share into $5.43/share in less than six months. Won’t tell you what I think, but I’ve been digging.