Bank of Canada, projected QT by year, assuming they maintain the existing trajectory:

2023 Bank of Canada Quantitative Tightening Schedule

Snapshot from January 9, 2023Government of Canada Bonds ($368.3 billion) and Canada Mortgage Bonds ($7.7 billion)

| Year | Amount | Pct |

|---|---|---|

| 2023 | $89,864,250,000 | 24% |

| 2024 | $55,880,720,000 | 15% |

| 2025 | $44,235,821,000 | 12% |

| 2026 | $37,432,059,000 | 10% |

| 2027 | $14,158,340,000 | 4% |

| 2028+ | $134,419,469,000 | 36% |

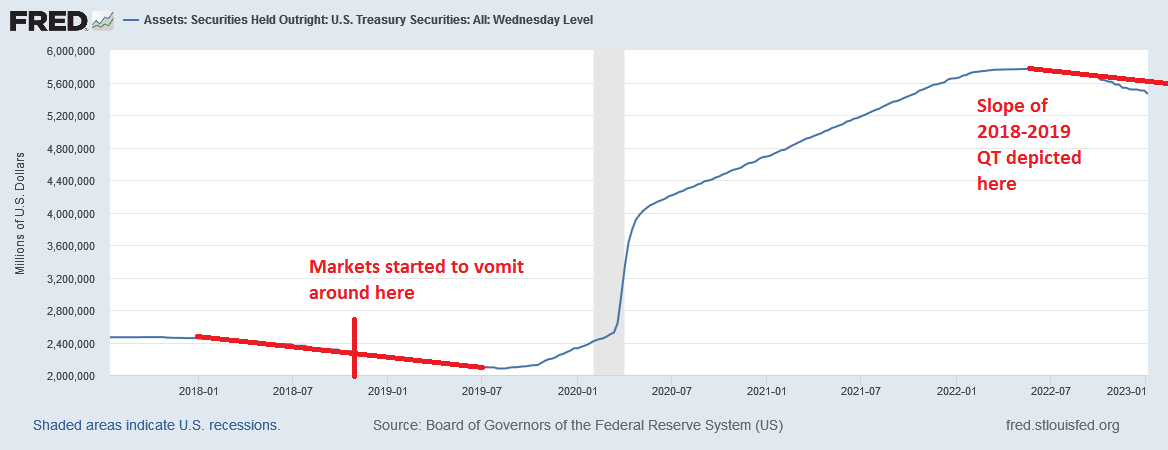

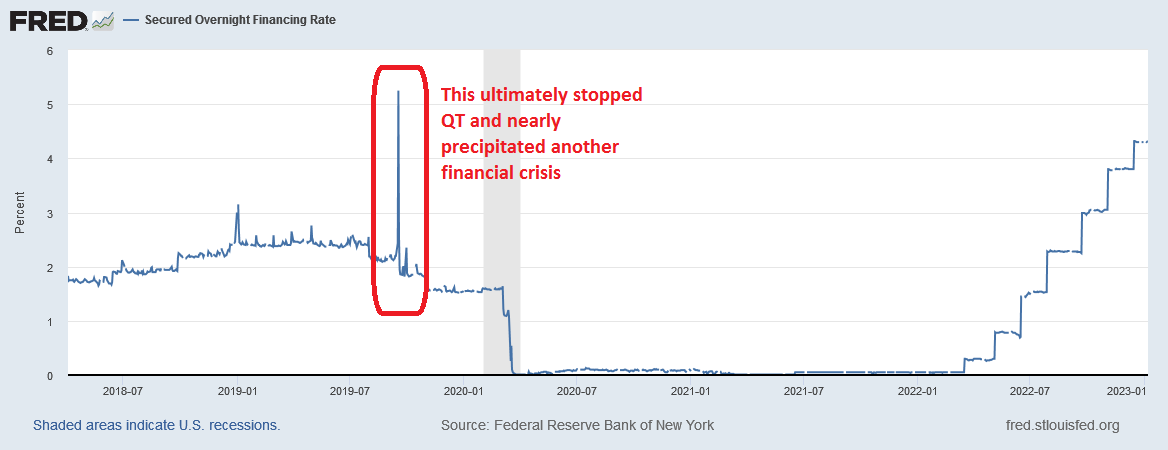

US Federal Reserve, treasury bonds, with some annotations:

And, here is another important chart:

Covid masked up (intentional use of language!) what was probably going to be a recession. The overnight rate crisis was a huge signal that something was wrong in the financial world liquidity-wise and required the intervention of the Fed to keep things steady.

Today, the environment is different. The issue is that there is a general sense of foreboding. If this is sufficiently baked into pricing, then it will become a non-issue compared to the unknown unknowns that are not priced in (which could resolve to the better or worse).

However, one reason why I focus on the progression of QT is because it reflects the extinguishment of credit. There’s a couple analogies for this. One is slowly taking oxygen out of a room. Another is a poker analogy, which I will use the reverse – quantitative easing: imagine you are forced to play poker (a zero sum game) with a lot of other participants (every other person in the economy), but the dealer is consistently giving out chips to people (more chips go to the “preferred” participants such as government-connected entities). Eventually handing out these chips will permeate around the table (more likely to yourself if you demonstrate some skilled play in relation to the rest of the competition). With QT, the poker analogy is increasing the amount of “rake” (the amount of chips removed per game as a house take) and a logical consequence of this is that people (and asset prices) should become tighter.

These (QT, interest rates) are knowns, but when does it get to the point where things structurally blow up? Does it? This line of thinking would also suggest that fixed income should do better than not – although let me tell you, the prospect of lending the Government of Canada money for 30 years at 3.12% is distinctly unappealing.