Things in the real economy are going to get a lot worse. You will see this with a lot of lagging indicators, especially unemployment. Come January and February 2023, the unemployment rate will rise a lot higher than the reported 5.4% for August.

The financial economy tries to predict these changes in advance and indeed, some of this has been already priced in. There are typically two areas where the market does not anticipate very well – when it over-extrapolates a trend, and also the failure to predict second and third order impacts of economic developments. The ability to predict these contributes to a lot of alpha for portfolio managers – worthy of a separate post.

At the end of the day, however, equity markets have some semblance of valuation on the basis of residual profits of the various entities which are given to shareholders. There is never an equilibrium price achieved, it is always fluid and subject to anticipation of changes.

When the so-called “risk-free” rate increases like it has, the comparisons become more competitive as there is always a risk premium between risk-free and risk-taking.

A concrete example of this is looking at a relatively stable equity versus a government bond.

We will use A&W Revenue Royalties Income Fund (TSX: AW.UN) as our example. It is nearly a universally recognized entity in Canada. The business is stable. The debt leverage employed is not ridiculous. While there are some complexities (the controlling interests have somewhat of a conflict with the unitholder trust), all you need to know for the purpose of this post is that the business skims 3% of the revenues of all A&W franchise sales across Canada. After interest expenses and taxes, the cash is passed to unitholders.

Right now this trust yields unitholders 5.4%.

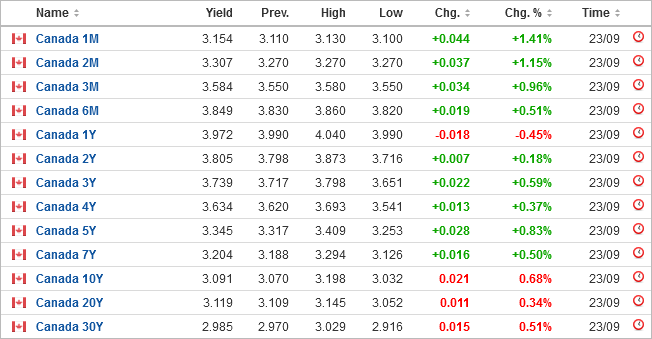

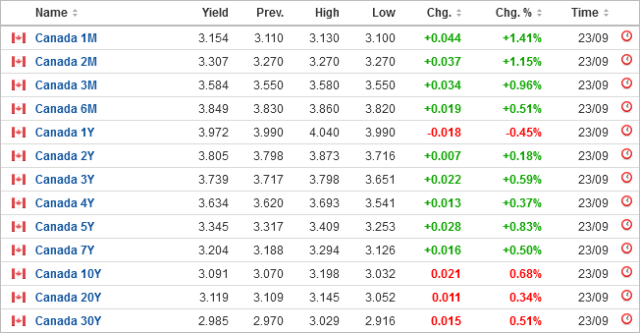

Contrast that with a 1 year government bond, yielding about 4%, or a 10 year government bond yielding 3.1%. If you’re dealing with retail amounts of money and want to put it into a GIC, a 1-year GIC earns 4.53%, while a 5-year GIC earns a cool 5% – that’s a larger rate of interest than it has been for a very, very long time. Savers are finally getting rewarded for a change.

In contrast with units of A&W, you’re not receiving a lot of compensation for your risk. As a royalty business, you are less concerned about profitability and more about gross sales – your incentive is that the business operate rather than thrive. For some reason, the market warrants the risk spread (to government debt) of about 1.4 to 2.3%, depending on time horizon, is deemed to be sufficient. One can argue this is too high or too low, but right now it is what it is.

If interest rates continue to rise from here, it is only logical that the equity risk premium rise as well. In other words, if 1 year rates go to 5%, and 10 year rates go to 4.1%, then all things being equal, the equity should be priced around 6.4% – or the equity should take a 15% price haircut from the current point.

The equity risk taken is absurd especially in light of other perpetual investments that offer a seemingly higher margin of safety than A&W. An example would be in preferred shares of Pembina Pipeline, say PPL.PR.A, which gives you around a current 6.9% eligible dividend (much better tax treatment than royalty income) with a gigantic margin of safety. However, in rising rate environments, many of these entities are extremely leveraged with debt, which may result in credit risk deflating the value of your shares.

There is also the overall market liquidity risk – when liquidity continues to decline (central banks are tightening up the vice with QT as we speak), valuations across the entire market will compress as the marginal dollar does not have the ability to sustain high asset prices.

So how does one survive as an investor in a rising interest rate environment? There are very few escape valves.

One is cash, or very short-term cash equivalents. While you take the inflation hit, your principal will be safe. You will also be the recipient of rising rates when you rollover your debt investments into the like.

However, many do not have the luxury of holding cash (funds are restricted from holding over a certain amount).

Preferred shares in selected companies are another possible escape route. While they do not offer great returns, many of these firms that obviously will be solvent and paying entities are trading at reasonable yields. Your opportunity for capital appreciation is likely to be very limited, but at least you’ll be generating a positive and tax-advantaged return. (I will once again lament the upcoming redemption of Birchcliff Energy’s preferred shares (BIR.PR.C) as being the last redeemable preferred share left on the Canadian marketplace (R.I.P.).)

However, many do not have the luxury of holding fixed income products.

So say there is a gun pointed to your head and you are forced to wade into the equity markets.

The problem is that anything with a yield is sensitive to increasing interest rates. Companies trading at high multiples will have P/E compression and this will kill your equity value.

The formula is that you need to invest in a company generating cash at a very low multiple (well beyond a 2-3% spread from the risk-free rate), the cash flows are sustainable, AND the company can either repurchase its shares at such a low multiple or give out cash to shareholders at a yield well beyond the risk-free rate.

There are not many companies like this that trade. Ideally one day you would find a royalty company trading at a 15% yield. Then you would pounce on it with full force.

There are very few moments where you see this happen, and when it does, it can be very profitable. February 2009, Q1-2016, Christmas 2018, and March 2020 were some recent times where you had a gigantic rush for liquidity in various names.

Execution on the trading is also not easy – before a royalty company reaches a 15% yield, it will have to trade through 8%, 10%, 12%, etc. At these valuation points, it will increasingly look more and more attractive. Back during the economic crisis of 2008/2009, I remember purchasing long-dated corporate debt in Sprint (the telecom) for a 20% yield to maturity and feeling a bit resentful when at one point it was trading at 25% YTM before it slowly made its way back to the upper single digits YTM a couple years later. A similar situation with equities and some distressed debt will likely happen over the next 12 months, so plan accordingly to reduce resentment of not catching the absolute bottom – markets are most volatile at their bottoms and tops. I do not think we are at all close to seeing the peak in volatility for this cycle yet, which is surely a ‘down’ cycle.