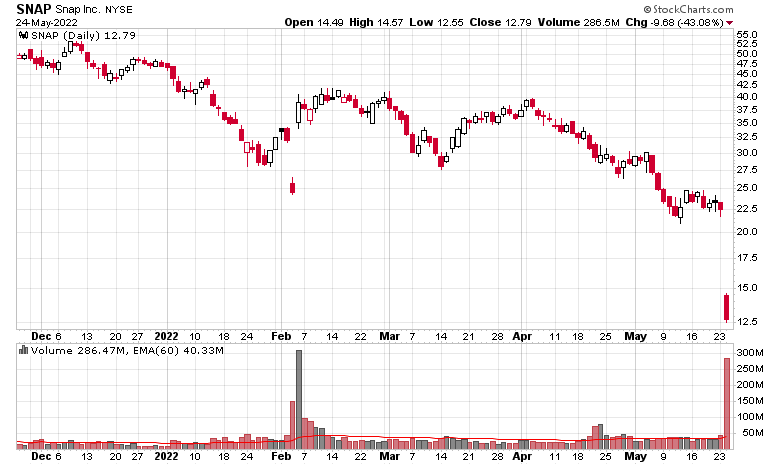

I look at the carnage going over in technology (today’s slaughterhouse featured SNAP, down 43% on an earnings report I never bothered to read) and ask myself if I am vulnerable to any of this.

I am guessing all of the tech-driven spending, including advertising, is just falling off the proverbial cliff. Everybody’s starting to tighten.

Economically, experiential spending will dominate 2022 (hospitality/entertainment) entirely due to Covid, the deferment of this type of stuff for the past two years is causing this year’s demand.

Just get on Expedia and look up prices of car rentals and hotels, they are higher now than I have ever remembered them. Just as an example, looking here in the Vancouver area, your average 2.5 star hotel is going for roughly C$250/night plus taxes (domestically), and it isn’t even peak summer season yet. Car rentals are $100 a day, even for a compact vehicle.

The demand/supply dynamic is causing these huge price spikes. People have money to throw at ‘experiences’, while providers are short-staffed and facing the same increased costs for labour, supplies, food, etc., hence everything is going to be at a premium.

This goes on until people’s money runs out.

2023 will probably be a better time to take a vacation. After all these tourist agencies increase capacity they will discover that nobody’s coming next year.

The flip side is that discretionary goods in the second half of this year will go on a huge sale. Home renovation season this summer will be totally dead.

Portfolio-wise, the best thing for me to do at the moment is to just sit on my rear end and take no action. It helps when I do not own anything like SNAP, although I do note the closest thing I have to a technology holding is down about 30% peak to trough. I am not particularly concerned for this holding, which used to be my largest last year. What happened instead, however, is that fossil fuels started to take over the portfolio through appreciation.

I see people switch from large cap to small cap energy names, but I am quite happy with the mish-mash that I’ve selected from my DCOGI index. I have no desire to deal with the sub-50k boe/d sector.

As long as the commodity price environment continues, these companies will continue to make a fortune. It will get to the point where governments will try to steal more shareholder profits and when they start to make their cash grabs, it probably will signal a time to lighten.

In the meantime, I think the fundamental argument for oil and gas continues to be very good. Chronic under-investment since the 2014 boom for various reasons (economics, ESG, Covid) has significantly changed the demand/supply dynamics in a manner that will take years to rectify itself. Only now some people are dimly waking up to the possibility that “renewable energy” is not going to be replacing fossil fuels in any substantive amounts and that there is an insatiable and growing demand for energy. This energy is functionally a first claim on any input in society – even before the taxman, which is saying a lot. You only generate taxes through income or consumption and you don’t get either without energy!