Most of the financial world tries to anticipate what actions Jerome Powell and the Federal Reserve decide to make with monetary policy.

For the past year, markets have been trying to anticipate the so-called “pivot”, i.e. the point in time where the Federal Reserve will stop raising interest rates and eventually lower them. The thinking is that lower costs of capital will usher in a new era of demand and we can party like it is 2009 with a rush of quantitative easing.

One problem, however, is there is a deeply psychological component to the inflation going on. The inflation expectation itself is a determinant of real interest rates. I’ll give a very simple example.

Let’s say the nominal interest rate is 5% and inflation is 2%. The real rate of interest is +3%.

However, if you expect inflation to be +4%, the real rate goes down to +1%.

The higher the inflation expectation, the lower the real rate.

An extreme example would be if you anticipated your currency turning into Argentinian paper, with a 50% inflation. Your real rate of interest goes very negative, very quickly and you suddenly will have a very large incentive to spend everything you can today.

We fast forward to today, where you still have the chairman of the Fed saying that inflation is too high. In Canada, Tiff Macklem more or less said as much.

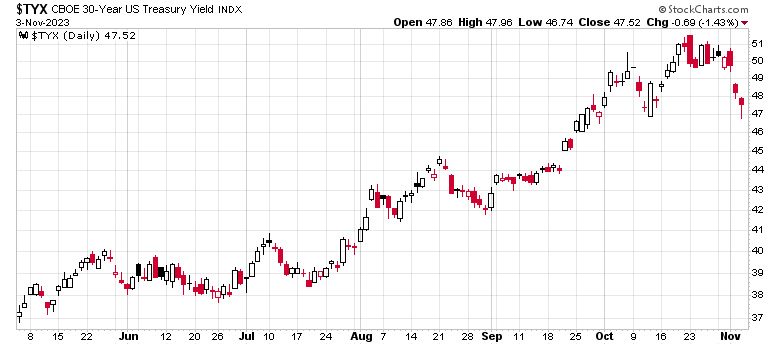

There is the makings of a chaotic system. While nominal interest rates are elevated and real interest rates are still quite positive in relation to past norms, the inflation expectation (the Bank of Canada has referred to this as “entrenched expectations”) continues to render the effective real rate down, if not negative. However, market participants are anticipating a halt in the increase of nominal interest rates and the Fed Funds Futures suggests that there will be 100bps in cuts by the end of next year.

It is precisely this expectation of lower interest rates that is preventing the nominal increase of interest rates to have their desired effect by central banks. As a result, demand is still high because inflation expectations remain high – practically speaking, the real rate of interest in the minds of a lot of people is negative. When the purchasing power of your cash continues to erode, why not spend?

The chaos factor is anticipating when there will be a turnaround in expectation. Psychological whims are fickle – much more so than nominal interest rates.

To use a science analogy, the economy is feeling like a super-saturated solution – one minor intrusion away from reverting into another state of matter. I can’t anticipate when this will occur. However, when it does, it will be relatively swift. I don’t want to use the word “crash” to describe it, but there is a possibility, albeit I would not rank it as probable at the moment.

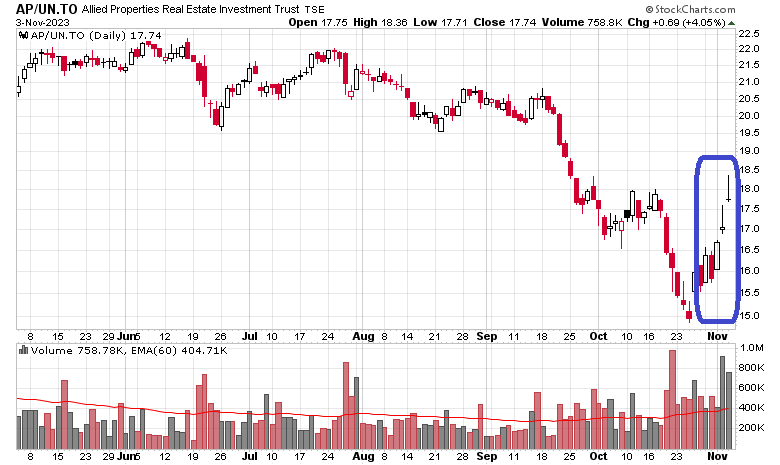

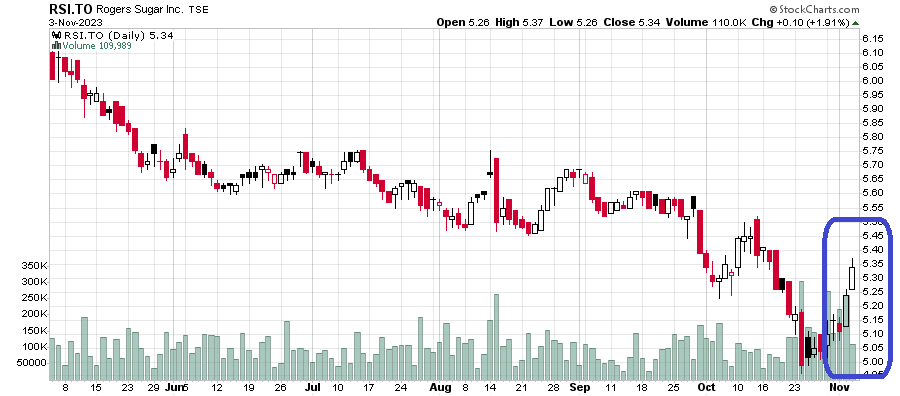

What are some defences to this scenario? Holding cash is good, although my gut instinct says it is a crowded trade. The trade is crowded enough that it will probably buffer the impact of lower prices. A scenario I see more likely is the long-term (10 year) risk-free rate rising to a point that suppresses equity valuations like a wet blanket on a campfire. Although this is hardly a scientific sample, stable royalty income trusts such as the Keg (TSX: KEG.un) have recently exhibited some degree of price contraction, likely due to the yield competition with cash. Why bother holding risky units in a steakhouse chain when you can just hold onto (TSX: CASH.to)? Is that truly worth a 250bps equity premium? It even looks worse for A&W (TSX: AW.un), which is at a 50bps premium at the moment. Maybe I should be shorting it!

Finally, let us not discount the slow impact of quantitative tightening. In Canada, we have $23.9 billion in government treasuries maturing on September 1, and another $558 million in mortgage bonds maturing on September 15. This is about 7.75% of the Bank of Canada’s balance sheet of treasuries and mortgage bonds. Funds parked at the Bank of Canada by banks remain plentiful, however – nearly $157 billion is still parked at the BoC at last glance. Credit is still available – you just have to pay a lot more for it.