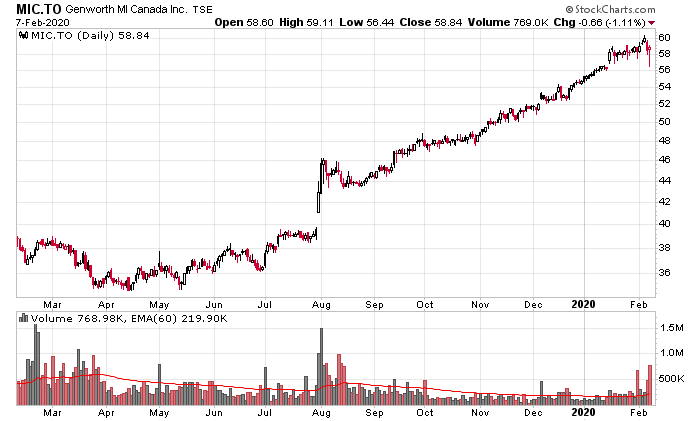

Genworth MI (TSX: MIC) reported their year end results last week.

Operationally they’re still minting a lot of money – loss ratio is 20% for the quarter, expense ratio is 20%, so they continue to earn 60 cents pre-tax for every dollar of insurance premium revenue they book. There doesn’t appear to be any storm clouds on the horizon.

An observation I will make is that with the new majority shareholder (Brookfield), they appear to now be deliberately targeting a higher return on equity policy. The company has been distributing a lot of cash in the form of special dividends:

During the fourth quarter of 2019, the Company paid a special dividend of $1.45 per common share, for an aggregate amount of approximately $125 million, on October 11, 2019 and a special dividend of $2.32 per common share, for an aggregate amount of approximately $200 million, on December 30, 2019. On January 15, 2020, the Board of Directors declared a special dividend of $2.32 per common share for an aggregate amount of approximately $200 million. This special dividend will be paid on February 11, 2020 to shareholders of record at the close of business on January 28, 2020.

In the span of a few months, the company has given off $6.09 in special dividends. Obviously I sold my shares too early! With these special dividends, however, the company is trading at about a 30% premium over book value, which is uncharted territory. Clearly given the cash generation capability of this business, it is likely to continue, but I have always wondered when there will be more competitive pressures in this market space – which if it occurs, will result in a dramatically reduced profitability landscape for the company. It won’t be triggered by the federal government – CMHC makes the lion’s share of the profit in this marketplace.

The company is obviously going to increase its leverage in the near future – on January 16, 2020 they took out a credit facility to allow them to borrow $200 million for a year, and another $500 million for 5 years. Part of this will be to rollover the $175 million in debt they have that will mature on June 15, 2020 but the remainder of it will probably head out the window in the form of special dividends so they can increase their return on equity from 11% to something higher.

Such strategies work until they start to face a large amount of mortgage claims whenever this near-mythical next recession occurs!