Some very random scattered observations. It’s been very difficult keeping your wits together in this environment. I’ve had to limit my “screen time”.

TSX Composite is down 31.3% YTD

S&P 500 is down 25.8% YTD

Canadian dollar is down about 10% YTD

Spot Crude (Western Texas Intermediate) is down 66% YTD

The TSX is down more probably due to the energy-intensive aspects of the Canadian stock market.

Crude, in particular, is trading at a curve that is utterly crazy:

Near month (May) $23.75

December 2020 $30.70

December 2021 $35.55

December 2022 $38.50

December 2023 $40.74

Want to dig a huge hole in your back yard, store 10,000 barrels of oil in there (this is about 1.6 million litres, so not a trivial amount!), and then sell it back to the market in a year and a half? If you can do it for less than about $120k, you’ll make a profit out of it…

I am puzzled how Natural Gas, for the most part, appears to be taking things relatively well – perhaps because they’ve already been beat up so badly? AECO daily pricing has held up quite well.

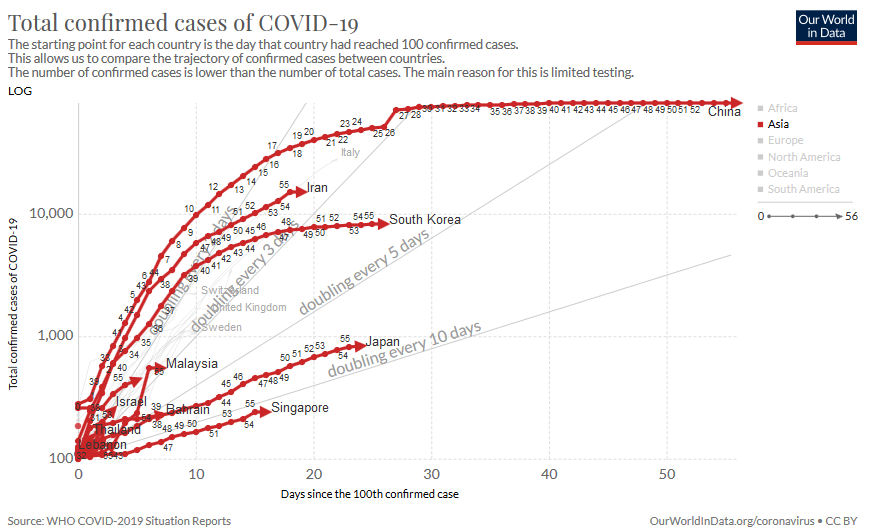

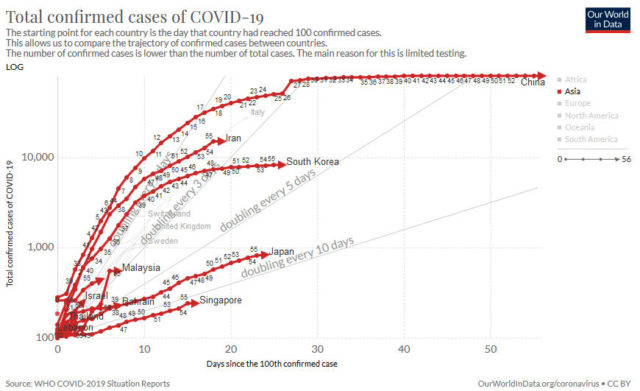

“The World in Data” guy is doing a huge public service by keeping the COVID-19 statistics accurate.

I don’t trust the data out of China (it’s also easier to treat the flu by sending people into virtual prison!) but South Korea’s ability to track and isolate this is quite impressive.

Hong Kong is also another jurisdiction that has very good capacity to deal with these sorts of things.

A silver lining is that we will soon be able to get more data out of Italy and other European countries to reliably tell us what risk factors are in play – i.e. the Chinese data from the studies of the people that died we can test whether they are reliable or not.

We don’t hear much about the inverted yield curve anymore – the 30-year US bond rate is now 1.9% and rising – inflation?

There has been too much on the radar in terms of what appears attractive if your hurdle rate is a 15% return on investment. If you’re looking for some “safe” investment products, I think the debenture complex of Ag Growth International (TSX: AFN.DB.E, F, G) look pretty attractive – they will give you roughly 17%, 14% and 14% CAGR, respectively over 2.8, 4.3 and 4.8 years, respectively. This has to be weighed against buying the equity (currently at $18) which you can make a pretty good argument that it will trade at its previous historical levels at $45 after everything is said and done. You’ll make 50% on the safer debt investment, but you’ll presumably make 150% on equity in a normalization scenario.

I have taken a position in Chemtrade debentures (TSX: CHE.DB.D, specifically) – this company produces sulfuric acid, water treatment chemicals, and sodium chlorate – these chemicals are really basic for industrial processes in electronics, pulp and paper, and other industries. Their equity (in the form of an income trust) has typically been a yield darling, but I suspect they are going to cut even further as a result of Covid-19. But the company does generate plenty of cash and while they are over-leveraged, they will survive this. They have a senior debt to EBITDA covenant which they may get close to but this is rectified by pulling the plug on the distribution. I’ve been watching Chemtrade for ages now, and while I was never thrilled about the relatively high valuation of their income trust (it traded as a yield vehicle) the underlying business is strong.

A comment on Canadian REITs – For the last five years or so, RioCan (TSX: REI.UN) has been trading at a close level to around CAD$27/unit. Today it is $15.69. While obviously there is going to be some lease impairments on companies that simply can’t afford to pay the bills anymore (restaurants, mom and pop shops, and just retail overall in general even without the assistance of Covid-19), eventually this land will get repurposed and produce income yields again. With interest rates being very low, when this rush for cash is abated, these types of income vessels are going to be very popular again. Don’t even get me started on residential entities like CapREIT (TSX: CAR.UN) that are still trading at levels that astonish me. There aren’t that many REITs to sift through, and while I think they are not going to post extraordinary returns when there is the inevitable bounceback, they are relatively “safe” – you can be sure those mortgages will be renewed on even the worst retail properties.

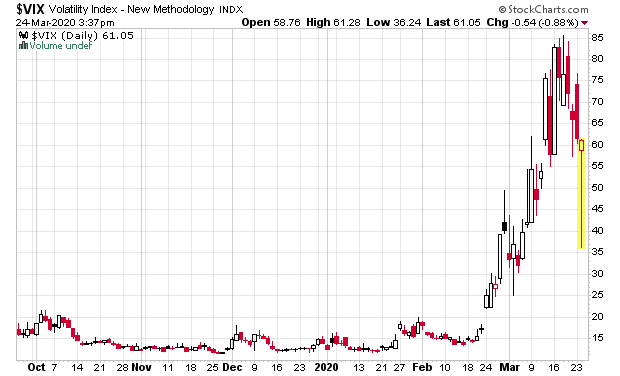

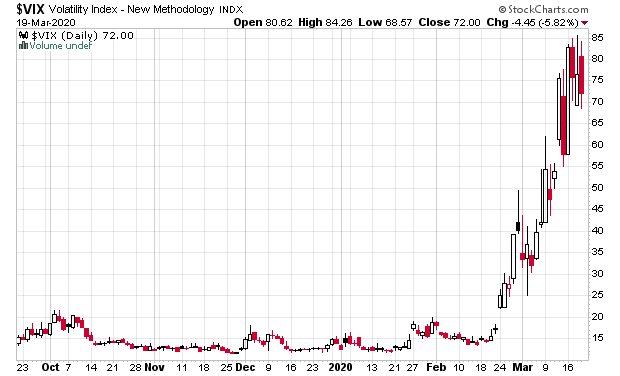

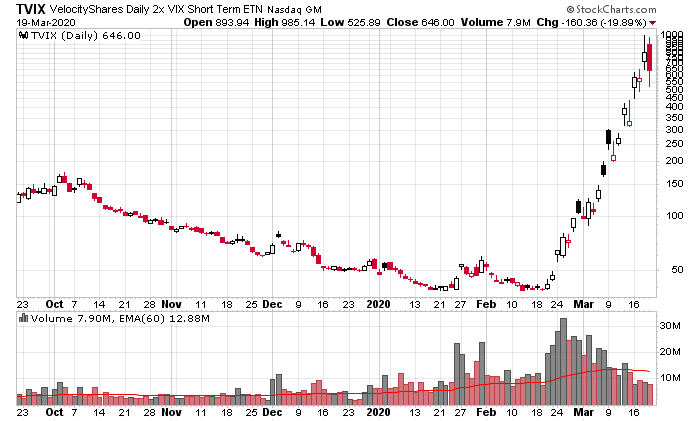

The markets have been limit-up, limit-down so many times over the past two weeks I have lost count when there have been volatility pauses. But these are also markets where if you want to sell, you should only do so on one of those limit-up days, and if you want to buy, you have to do it on one of those limit-down type days. This volatility has been more insane than I have ever seen it, and this includes the global economic crisis of 2008-2009. This probably also means that if you can keep your sanity you might be able to make some money out of it, but it requires a seriously wild ride to get to and from – if you don’t get cashed out.

Almost everything is trading at elevated yields that we have not seen in ages. Dividends are probably going to get cut across the board from a lot of companies, and P/Es are going to be sky-high after Q1/Q2 results get reported.

GFL’s IPO (TSX: GFL) was done at the cusp of the market meltdown, and they’ve held up surprisingly well. Considering that garbage collection is one core duty of society that can’t be stalled out, I can see why. They might stand a decent chance of recovering quite well (I’d choose them over the REITs for example).

Throughout this process the supply chain has been quite resilient. It has only been a week since the lockdown and as far as I can see, things are still available. Aside from some silliness involving toilet paper and other products, goods are still flowing. This is important. There are two large logistic companies in Canada, Transforce (TSX: TFII) and Mullen (TSX: MTL), and both are very well run, and both are trading at lows. While this sector will obviously take damage during the lock-down, it is a privileged sector that currently has priority.

Finally, quant funds have had their models absolutely destroyed, and just like Long Term Capital Management, are being forced to rapidly unwind. Leveraged funds, especially on fixed income, for example, have likely tried to scramble. As soon as this supply pressure abates, there will be upside volatility. Traders that are keeping cash on the sidelines likely won’t have much time to take action in this event – it will probably be just as violent going up as it was down. I’ve been on the wrong side of a lot of this to date, so take these words with grains of salt!