It looks like things are getting heated in the board backroom of Slate Office REIT (TSX: SOT.un). 17 days before the scheduled Annual General Meeting, George Armoyan decided to let loose a proxy solicitation to install two additional directors out of six. If he won, including himself, that would constitute a board of six directors – George himself, two controlled by him, two directors (the co-founders, who are brothers) and an independent.

To take action this late in the game suggests that there was some sort of board decision that pissed him off.

Armoyan controls 17.7% of the units, or 15.1 million units of Slate, which gives him huge sway considering that only 36 million units voted on the resolution to increase the gross book value to debt ratio of 65% earlier this year. When adding the 1,123,880 units that one of the director nominees owns, it’s a near majority. 32 million units voted in the 2023 annual general meeting. It’s quite likely that Armoyan will find at least a million or so disgruntled Slate Office holders to vote in his direction to put him over the top.

Part of the previous vote was a consent to decrease the board size from 8 to 6 trustees, which means there are less people for him to take out. If he is successful, he will effectively have at least a veto on every decision from the board, which is close enough to having control of the entire operation.

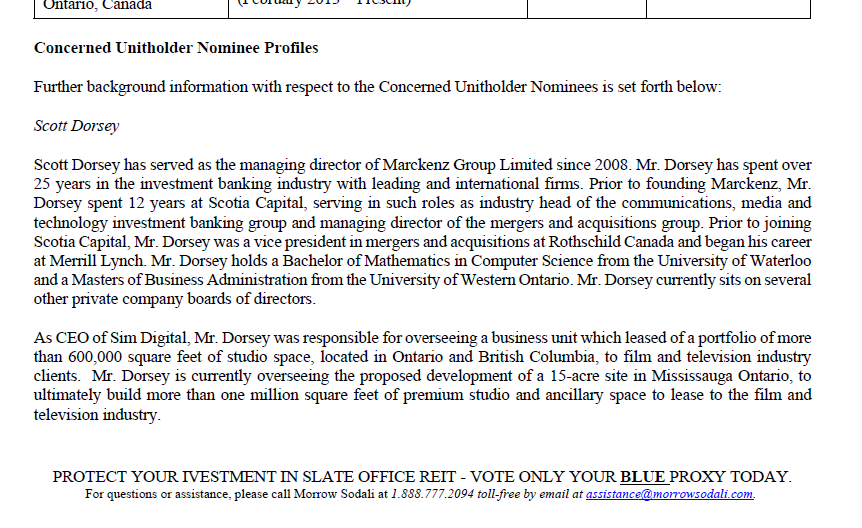

I do note, however, when reading the proxy solicitation statement, that it must have been hastily constructed. Witness the following from their proxy solicitation:

On the bottom, “PROTECT YOUR IVESTMENT IN SLATE OFFICE REIT”. Not the greatest look for the professionalism of Morrow Sodali, the firm being engaged to solicit the proxies.

Perhaps they all just need to hold on until after June 25 before going into CCAA – at least when everybody disposes their units for zero, they get 2/3rds and not 1/2 inclusion on the capital loss. To be clear, this was a joke and not a prediction although the last financial statement released by the trust is not looking that good!