Teledyne (NYSE: TDY) is undergoing the process of acquiring FLIR (Nasdaq: FLIR) for half-cash, half-stock.

The cash component is about US$3.7 billion.

They have a credit facility for $1.15 billion and they performed the following bond offering for $3 billion total:

$300 million aggregate principal amount of 0.650% Notes due 2023

$450 million aggregate principal amount of 0.950% Notes due 2024

$450 million aggregate principal amount of 1.600% Notes due 2026

$700 million aggregate principal amount of 2.250% Notes due 2028

$1.1 billion aggregate principal amount of 2.750% Notes due 2031

Needless to say, considering the 10-year government bond yield is around 155bps, this is cheap financing.

From their GAAP earnings, FLIR earned $1.60/share diluted in 2020 and at an acquisition price of US$56/share (assuming TDY at $390), that’s 2.9% without growth or synergies.

There’s still a bit of a merger arbitrage (about $1.30/share) which is a moving target because TDY has been gyrating since the merger announcement, but I am looking to dispose of the stock eventually once I have found a more suitable USD target for capital.

I don’t talk about IPOs very often, but this one caught my attention because of its presence in the agricultural space. Farmer’s Edge (TSX: FDGE) went public at an IPO price of $17/share, raising $125 million in gross proceeds ($117.5 net), and started trading on the TSX on March 3rd. Unlike many other technology IPOs, they have at a modest premium to their offering price:

There is a customary 30-day option by the underwriters to purchase more shares, which at the current market price of CAD$18.80 is likely to happen. I will assume so – the company will have 41.8 million shares outstanding if this happens.

Fairfax (TSX: FFH) owns 60% of the company after the offering and is the only 10%+ shareholder.

(Update March 8, 2021: The stock is now trading under CAD$17/share, that was quick… FFH will own 62% without the exercise of the over-allotment).

(Update March 9, 2021: Underwriters have exercised the over-allotment option – gross proceeds $143.8 million).

Company’s Operations

FDGE offers a package called FarmCommand. It is a piece of software which integrates with provided hardware (CanPlug) which facilitates a data conduit to the software relevant to measuring grain weight by location during a harvest. The software beams the information to the cloud using cellular data, and the software crunches the metrics and presents it to the end-user. Likewise, they also sell weather probes and soil moisture probes that can send data to the server (and this data can be used to make correlations at future times). Finally, they do have a soil sampling service that looks painfully manual and will test the soil for composition, using their own lab equipment. This information can be used later to suggest fertilizer solutions.

They use Google to store the data to the cloud, and Airbus to provide satellite imagery.

Revenues are obtained by selling farmers the FarmCommand package on a per-acre-per-year basis and also collecting such data to sell to crop insurance companies.

Relevant quotes:

FarmCommand is sold on a subscription basis, per acre per year, and is offered in five principal tiers. We focus on selling our $3.00 Smart package but offer price points starting at $1.50 for a basic Smart Imagery package, scaling to $6.00 for our comprehensive Smart VR package, with these list prices and packages varying marginally by geography. Our customers have historically subscribed to four-year contracts. Recently, we have introduced our Elite Grower program which allows our customers to trial our platform for free for up to one year before subscribing to a four-year contract.

…

Crop insurance partners form part of our go-to-market strategy and we expect them to sell our subscription products to their agriculture customers. Once our program is deployed on the farm by a crop insurance company, Farmers Edge will be able to provide reporting, analytics and predictive modeling to the crop insurance industry players on demand.

This reminds me of car insurance companies getting people to voluntarily put a device in their car dashboards for the purpose of insurance assessments. If you are a “safe” driver, as in you don’t drive that much and when you do, you drive at low speeds, then the insurance company will give you a discount. In reality, they will use this information to determine more accurate pricing, which is why there is a significant degree of selection bias with such offerings.

I also believe certain farm operations have proprietary methods that they would not want to disclose, which would work to the detriment of FDGE.

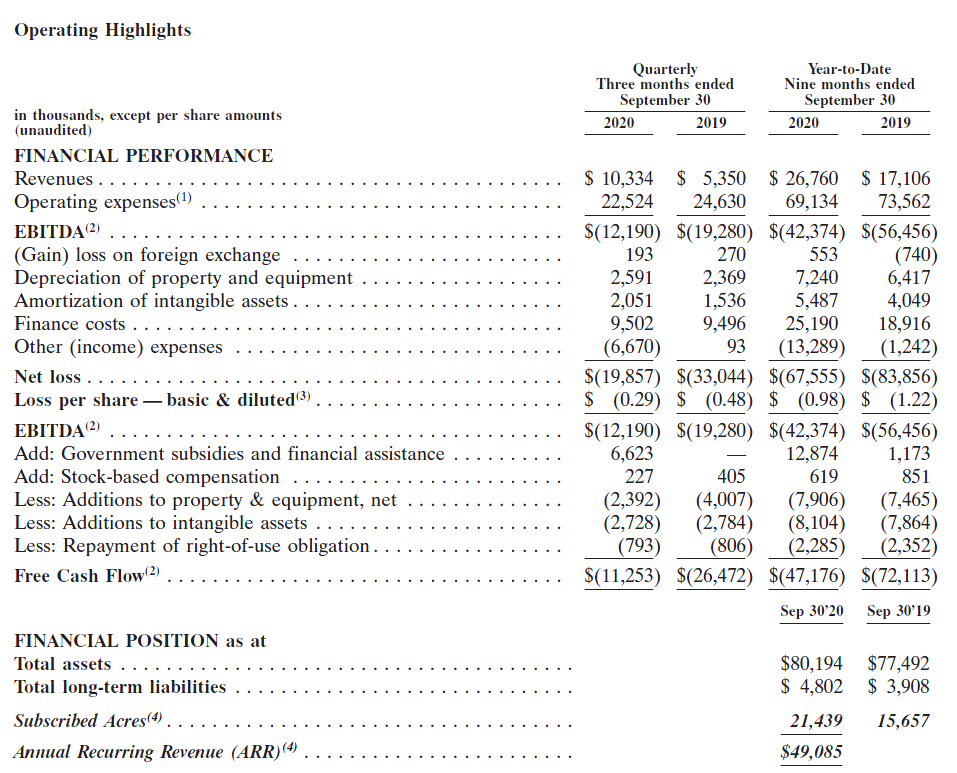

FDGE states they estimate at the end of Q4-2020, they have 23.4 million acres of subscribed farmland, and an estimated revenue of $45-47 million for 2020. 54% of this was Canada, 28% was USA, and 13% was Brazil, and the remaining 5% is Australia and Eastern Europe.

Keep in mind rough estimates are that Canada has 90 million acres of cropland, the USA has 250 million acres and Brazil 150 million. The total addressable market in these geographies assuming 100% penetration and the $3/acre package would be about $1.5 billion a year in revenues.

The company claims it adds value:

The ROI our solutions provide farmers vary by product and region. As additional examples, corn farms implementing our solutions earned farmers roughly $52 more per acre in Nebraska, and $36 more per acre in Kansas, compared to state averages, in 2019.

Clearly if this is the case and if they can establish this with better studies and have a proprietary advantage with their software to make it happen, then one can presume they can capture more margin than $3/acre.

In terms of competition, they list John Deere (NYSE: DE) and Bayer-Monsanto (OTC: BAYZF), but they allude to a “Point and regional solution providers” which is clearly referring to Ag Growth (TSX: AFN), but they are never named quite likely for the reason that they are the true competition.

Finances

The company has lost a lot of money over the past 3 full fiscal years. The “finance costs” is somewhat misleading as the company has been financed with debt before the IPO and this was equitized for the IPO.

In terms of raw EBITDA, and the accumulated non-capital loss for tax purposes (which is a rough proxy for true expense), we have:

2017: $53.8 million loss / $130 million

2018: $76.4 million loss / $199 million

2019: $74.2 million loss / $309 million

9 months in 2020: $42.4 million loss (annualized, $56.5 million) / tax NOLs not disclosed yet

This is also ignoring capital costs, which are not inconsiderable as the company has to get the hardware into the farmers’ hands (in addition to the installation) in order to do the data collection.

The company gave projections for 2020 and is expected to have burnt $52-56 million. Because of the renegotiation of the Google contract and the satellite imagery contract (which has been re-contracted to a subsidiary of Airbus), they are expected to save an annualized $15 million in costs (makes you wonder how they managed to negotiate the deals in the first place – this was not an inconsiderable cost savings).

The company has been mostly funded by Fairfax during inception. There are a couple other under-10% holders, one of which (Osmington Inc.) has the right to a board seat as long as they maintain at least 5% ownership.

After the IPO they will have converted all of their debt into equity, and have a pro-forma $106 million of cash on the balance sheet as of September 30, 2020 and the only significant debt being $6.5 million in future lease obligations.

They claim “break-even for Free Cash Flow in the medium term, assuming growth in Subscribed Acres remains consistent with the above expectations” (45-50% annually). Of course you will if you grow high-margin revenues at that rate! While achieving that percentage growth is indeed possible, the question remains whether they can do it profitably (it is difficult to make money giving out 1-year free trials and not cashing them into 4-year contracts), and the terminal growth rate of the business (it will not be 45-50% annually for a very long time, especially given the acreage penetration they have already achieved).

I’m not going to comment on the management suite or the board of directors, but I have reviewed them.

Some analysis on the software

There’s a lot of interesting information on how to use their product online. For instance here is one particular function within their FarmCommand software, but also as part of a series of instructional videos:

This competes with AGI’s Suretrack Compass software:

I’m finding this comparison between the two softwares to be interesting. AGI’s solutions are obviously vertically integrated with some of their products (their grain silos), while FDGE’s solutions are a horizontal turnkey solution. There is a lot of overlap. I would suspect that part of the reason why FDGE has spent a ridiculously large amount of money to date is to just get farmers aware of the software – they don’t have any inroads to the end-customers that a company like AFN or John Deere would have.

The other observation is that these Youtube videos that I linked to have views that are measured in the low hundreds. Almost nobody has watched these videos. There appears to be zero public awareness of agricultural software. If at some point these companies receive more eyeballs (heaven forbid if /r/WallStreetBets decided to hit it), there aren’t a lot of public companies in this space that would receive instant elevation to their valuations.

Consider that the weekend market capitalization for FDGE is $765 million – higher than Ag Growth’s $715 million (albeit, Ag Growth has a considerable amount of debt on their balance sheet, about $870 million), it makes one wonder how to reconcile the valuation differential. Is this attributed to FDGE as being some sort of “pure SaaS play in the Ag Space”, while Ag Growth is a much larger conglomerate (set to exceed a billion dollars in revenues), primarily concerned with the (relatively more boring) design and construction of grain towers and movers rather than having their own piece of software, which by all accounts does mostly what FDGE does?

I’m not interested in FDGE at current valuations, but I’ll watch it. If it turns out the current valuation of FDGE is “correct”, Ag Growth is incredibly undervalued.

Disclosure – I presently own shares in Ag Growth (posted here).

James J. Moore Jr. has done an incredible job with Atlantic Power – it is unfortunate the IPP industry as a whole has faced significant headwinds over the past decade. In what is (hopefully) his final letter to shareholders, he writes the following (underlining is my emphasis):

What about the new green energy policies? Shouldn’t they have a positive impact on Atlantic Power?

I have said in the past the power business is cyclical, capital-intensive and commodity-priced. I also have cited the Warren Buffett adage that when a management team with a reputation for brilliance tackles an industry with poor economics, it is invariably the industry that survives with its reputation intact. More money has been lost in the energy space by investing in themes (surfing green waves, combined-cycle gas plants in the late 90s, YieldCo’s, peak oil, etc.) than any other way I have witnessed. I have repeatedly noted to shareholders the challenging markets for power and the poor fundamental outlook. Public policies pushing green energy and electrification have not pushed demand up as much or as quickly as taxpayer subsidies, state Renewable Portfolio Standards and corporate commitments to green energy have pushed up the supply of generation. Our hydro portfolio contributed 24% of our 2020 Project Adjusted EBITDA, but that EBITDA was generated under PPAs which were signed in the pre-fracking era when power prices were substantially higher. Market prices today are a fraction of those PPA levels. Green policies in places such as New York may provide some uplift in demand or power prices. However, the continual extension of tax subsidies at the federal level is likely to continue to incentivize the addition of supply to power grids that don’t require more intermittent generation but will get it, needed or not.

Before making a decision on the value of your shares, you may want to consider the fundamentals, such as: What are prices today for new PPAs or for projects without PPAs? Is more supply being added to the grid than there are retirements? Where is demand headed? Will demand for things like electric vehicles grow nearly as quickly as new supply is added to the grid? Be aware that new technologies can be very destructive to commodity prices. Fracking was truly an energy revolution, but it also killed the natural gas market in the United States for a decade, as was predicted by Mark Papa (the brilliantly successful CEO of EOG Resources) about a decade ago.

The stumbling block for this transaction is most likely going to be the preferred shareholders – when this acquisition was initially announced, there were those that claimed they should hold out for par ($25) but even they I think are starting to realize that it is the common shareholders that got (mildly) the short end of the stick in this transaction – the value that accrued to the preferred shares should have gone to the common shareholders. Indeed, this is one of the rare times where pronouncements of “fairness” actually appears to be the case.

Long-time readers here should remember that I referred to a specific security as cash parking vessel. I didn’t make it much of a secret, but I was referring to DREAM Unlimited’s preferred share, which has been redeemed at the end of 2019.

There has been a lot that has happened since then and now! During the COVID crisis, there were a lot of good opportunities for fixed income investors in the form of bonds, preferred shares and income-bearing equity (in addition to others). Today, however, when scanning my fixed income lists, it is a total wasteland – generally the reasonably safe returns will give you a 5% dividend, while marching up the risk spectrum (e.g. Bombardier’s BBD.PR.B) will get you about 7.3%. It is slim pickings.

The next nearest cash-parking vessel is Birchcliff Energy’s (TSX: BIR.PR.C), which I have written about during the COVID crisis. Unfortunately, it, along with its twin cousin, (TSX: BIR.PR.A) is likely to get called out over the next 1.6 years – I am expecting the company to redeem the latter for par on the September 30, 2022 rate reset date.

It is very tempting to leverage up on “safe” preferred shares yielding 5% or so and finance it with 1.5% margin debt, but as the market instructed people 12 months ago, doing so can be very financially hazardous in the event of a collapse in asset prices.