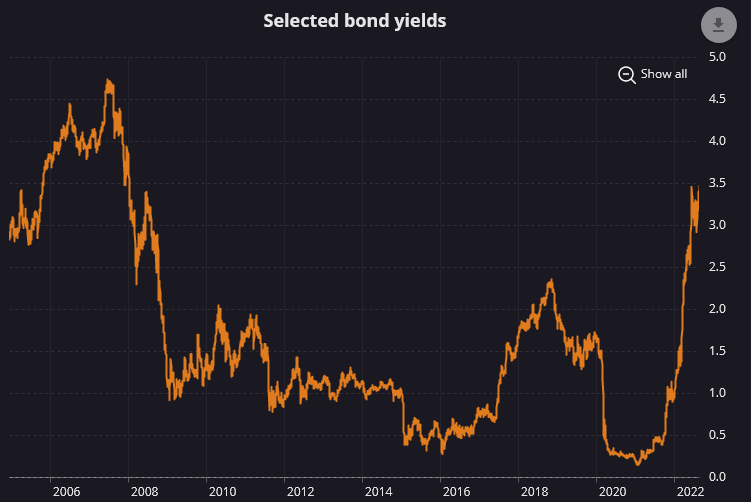

Exciting times in Canadian government interest rates – finally seeing some yields again (2 year Canada government bond chart below):

Short-duration bonds are yielding higher than they were before the 2008-2009 economic crisis. The one-year bond is at 3.67% currently, and the two-year at 3.53%.

I’ve talked about this before, but one theory in finance is regarding the term structure of the yield curve in that the total returns is invariant to the term one invests in – e.g. if you invested in 1-year government bonds 10 times, the net result will be the same as if you invested in 1 10-year bond. Of course, practice is different than theory, but if one were to take this theory and apply it with the existing rate curve, it would suggest that the target rate is going to rise significantly higher than the so-called “neutral rate” which, according to the monetary policy report, is between 2-3% nominal. I’ll leave it up to the reader to decide on the validity of these financial theories.

In the monetary policy casinomarkets, the 3-month Bankers’ Acceptance Rate is currently at 3.46% and has crept up slowly in anticipation of September 7, 2022’s expected rate increase – the September futures indicate a 3.89% 3-month rate. I am not sure if this translates into an expectation of 50 or 75bps for the September 7 meeting, but either way short term interest rates are going up. The next meeting of the bank on October 26 is anticipated to have a 25 basis point increase as well.

All of this means that money is coming harder and harder to come by. Governments will find it much more expensive to borrow money, so I would look carefully at your portfolio for entities that are government-dependent.

The big risk continues to be that interest rates will rise further than the market anticipates – and it likely will if inflation does not reach the magical 2% target.