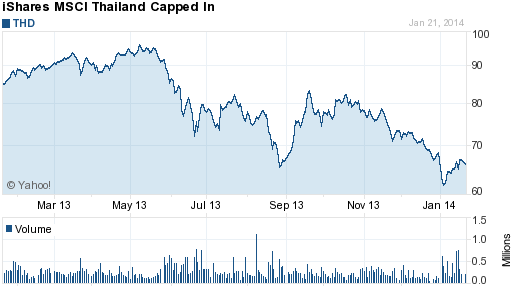

Something that hit my political radar a few months ago was that Thailand is going through yet another political crisis. This has a material impact on their equity pricing, as witnessed by the only ETF available to invest in Thai stocks (and that is THD):

There were two thoughts in my mind as this was going on: Will I be able to get an inexpensive Thailand vacation as tourists flee the country, or will I at least be able to earn one by investing in what will likely result in some sort of economic crisis?

The ETF itself is not of a trivial size – it has $500 million in assets under management, trades about $15 million in volume a day, and has about half of its holdings in the top ten consisting of large cap Thai companies such as financials, telecoms, industrials, and so forth. They represent roughly an equity proxy for the country similar to the Dow Jones Industrial Average. The size of the country’s equity market is large and liquid enough that my comments here will not materially contribute to any price movement, so I can write a little more freely on this topic.

It does not require an experienced lens to figure out that there will be continued unrest in the country going into early 2014. There is a highly polarized political situation with the two factions holding considerable public support – in a constitutional monarchy environment where the monarch does exercise power (a subtle version of power, but to a much greater extent than monarchies such as Canada or the United Kingdom), coupled with democratic culture being a means to an end rather than a process of acceptance for defeated rivals, this will create excessive tension. In addition, the Thai military is a significant third “political party” that any governing party needs the implicit consent in order to govern in the country.

The democratic culture in countries that have not evolved with the British parliamentary system is significantly different in execution than in countries that have been influenced by it. In the Western democracy sense, voting (whether in general elections or within legislative chambers) is the final arbitration of public decision-making. In a good number of developing countries, it is akin to how lines painted on the road: for advisory purposes.

Thailand will survive this political crisis as it has done for the past century. It will do so in typical Thai fashion, and there is no shortage of historical articles one can dredge up to get a fairly good idea how this one is going to turn out. Despite the public mess that is occurring, they will solve their own problems. The only question is when and how much collateral damage is done in the process.

I will be keeping THD on the watch list. There are no exchange-traded ADRs of Thai companies that one can directly trade with any liquidity of significance that I can find.