I did not write an update to Genworth MI’s first quarter as it was relatively routine (albeit a slightly negative quarter in terms of premiums written). This decrease was due to the corporation being more conscious of what they were underwriting, in addition to slowdowns in oil-producing regions. Financially they continue to be wildly profitable, with a combined ratio of 42% and continuing to build book value (sitting at $37.23, about a 10% discount to market).

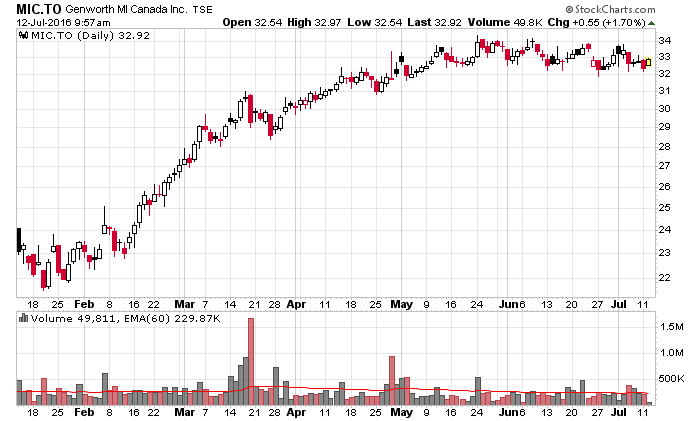

The company’s stock price has not gone anywhere over the past couple months:

I look at peer companies, both in the financing and REIT domains and see nothing catastrophic occurring there.

There are a few interesting undercurrents that Genworth MI is facing, including:

1. Issues at the Genworth Financial parent company (this may result in financial pressure on their holdings – indeed, one scenario for Genworth MI is that they will be liquidated, hopefully at book or a premium to book value!);

2. The new Liberal government elected in Canada may introduce some curbs or regulatory burdens (via OFSI) which would encumber the insurance operation and/or empower CMHC;

3. Impact of oil prices and on the Alberta/Saskatchewan housing markets, although delinquencies have not risen beyond expectations to date;

4. The general insanity that can be found in the Vancouver/Toronto housing markets;

5. Provincial governments enacting curbs on transaction volumes and generally suppressing volumes that would otherwise stimulate the mortgage insurance market.

In addition, there are known regulatory changes concerning portfolio insurance transactions that were effective July 1, 2016 which would serve to decrease premiums received in what would be a fairly low-risk insurance market (such loans have loan-to-values ratios of less than 80%). Fortunately, these transactions have typically only been 10-20% of the premiums written in any single quarter.

About CMHC, they continue to deliver worse results than Genworth MI (quarterly reports for CMHC here) and their fraction of insurance covered in the Canadian market continues to decrease – a question remains whether they will attempt to take more market share, which would serve to deflate Genworth MI’s future premiums written.

With their present insurance book, as long as there is no general property market crash, they will continue to book revenues as mortgages are amortized and converge to at least book value. They also will be generating an excess of capital which management can decide to repurchase shares or declare a special dividend (which they typically do in the second half of the year). At present prices both are acceptable options although I really thought they should have bought back shares in January and February.

Genworth MI is still valued cheaply, but of course was not the screaming bargain it was when it was below $25 earlier this year. There is still capital appreciation yet to be had. In the meantime, shareholders are paid to wait.