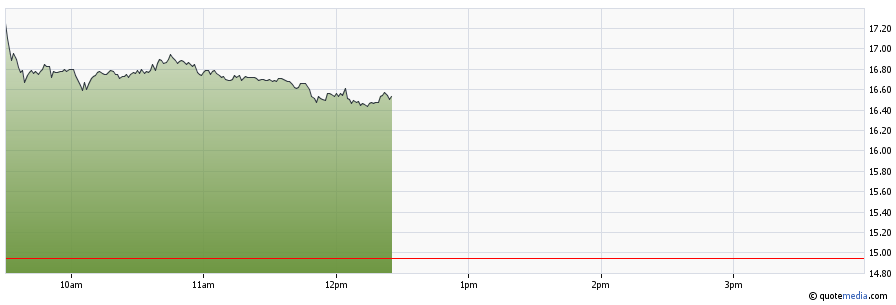

Home Capital – Don’t know why it is trading up

The power of Berkshire is strong – why would shares of (TSX: HCG) go up when the acquisition price is so dilutive to existing shareholders (selling 19.9% of the company for CAD$9.55 and another substantial chunk of equity at CAD$10.30 to a 38% ownership interest) and the company cannot even obtain a better rate on a secured line of credit than 9%?

They managed to sell $1.2 billion dollars of commercial mortgages between 97 to 99.61 cents on the dollar, which leaves the question of how much their residential portfolio is worth. How can this investment by Berkshire and the line of credit be good for anybody but Berkshire, or more specifically anybody but common shareholders?

Now that short sellers have been crushed to death, I’m going to guess the next month or so will likely represent the “top” of their stock price. Borrow rates are 75% right now so I’m not touching it.

Book value with this stock purchase, FYI, goes down to under CAD$20/share. So even on a price-to-book metric, HCG is almost trading like a regular mortgage provider – except with the very relevant fact that their cost of capital is well above what they can receive in mortgage interest! How they plan on making money by issuing 5% mortgages and loaning money from the credit facility at 9% or 10% is beyond me. Maybe they’ll make it up on volume!

There is absolutely no reason why Genworth MI should be trading up 10% on this news either. They are in much, much, much better financial shape than HCG, and shouldn’t be trading at less of a discount to book value than HCG is!

Stress in Canadian oil and gas

I wrote earlier this year about the downward slopes of Canadian energy companies and six months later, nothing appears to have changed – the trajectory for most of these companies continues to go down.

Commodity pricing is also highly unfavourable – WTIC crude is at US$43/barrel as I write this and the CAD/USD exchange is around 75 cents on the dollar.

So at these price levels, there are going to be plenty of companies that will find it very difficult to make any money.

What hit my radar today is Cenovus (TSX: CVE) taking a hit after their investor day presentation – their CEO is calling it quits at the end of October and planning a $4-5 billion asset disposal. The stock is down to about CAD$9.20/share – noting they raised $3 billion in capital back in April at CAD$16/share when they purchased back their 50% of their partnership in the Foster Creek/Christina Lake projects. Those shareholders must be feeling pretty “steamed” right now, having experienced a 42% depreciation on their capital in a few months.

In their presentation, they stated that the company is break-even at US$41/barrel. You can be sure that if present pricing stays at the current levels, there are going to be a lot more medium-cost producers that are going to start feeling the pinch on their balance sheets – the “bunker down and wait for better pricing” strategy only works when your rivals are out of money and you’re sitting on a treasure chest. Right now, everybody has enough liquidity to last another year or so before things really start hitting the fan.

Equity holders, in addition to feeling already light-pocketed, should continue to worry as debts rise and creditors start taking more and more of any available cash flows out of these corporations.

And as readers know, when there is desperation in the financial markets, that’s usually a good time to invest money. But now still doesn’t feel like the right time.

Amazon – Whole Foods

This is a rambling post with thoughts and no coherency.

Amazon and Whole Foods are two companies are at a larger market capitalization than what I normally would research, but I do take interest in the business strategies involved.

Here in Canada, there have been two retail developments in the larger player space over the past decade – the collapse of Target’s entry (despite a few billion in capital invested in the venture), and the merger of Loblaws and Shopper’s Drug Mart. The consolidation of Shopper’s Drug Mart has been more successful for Loblaws than I originally thought it would be. The collapse of Sears Canada was inevitable and I generally do not consider this significant other than another multi-decade titan fading into dust. Walmart Canada and Costco appear to be untouched at present. Amazon’s presence in Canada is still considerably limited and this is likely due to a function of geography and scale (most of the stuff gets shipped out from the Greater Toronto region).

I do notice that Loblaws (via Superstore) is trying to get into the digital presence – they do have parking stalls that are reserved for online ordering pickup and I am fascinated to see how that process works out (I have not used their service).

So I am asking myself what Amazon is trying to do with the Whole Foods merger and I think it is a reasonable gamble on their part. First, the chain itself is profitable and although their margins have compressed like a typical grocery store chain (it is a miserable industry to compete in), they do have excellent mind-share and geographical presence in upper-scale urban areas.

Amazon is trying to expand its retail physical presence and one area where they do not compete in currently is food – the question is whether they are trying to invade this space (i.e. going after Costco directly) or whether they are using it as a shipping hub (which in this case, they paid a lot of money for what are effectively large-scale post office boxes). I also do not believe that remaining in the premium food space is going to continue to be economically viable since the proliferation of other chains (e.g. Market of Choice, Metropolitan Market, to use a couple West Coast analogies, but even a franchise such as Trader Joes should be quivering at Amazon right now) is continuing to cut away at Whole Foods’ dominance. Using this analysis, Whole Foods’ decision to sell out was probably a good one for their shareholders, but the strategic benefits to Amazon still remain at the “reasonable gamble” stage. It must be nice to be able to throw US$13 billion in pocket change (they have $21 billion in cash and equivalents on their balance sheet as of March 31, 2017) at something and see if it sticks.

In terms of how this will impact Canada, it will not be clear until we see what happens in the USA – in Vancouver, there are five Whole Foods stores (and a couple of them were purchased from a company that marketed the stores as “Capers” which started quite some time ago).

So the questions here:

1. Is Amazon trying to augment its food offerings online (which generally have been lacklustre and expensive?)

2. Is Amazon trying to use Whole Foods as a moderate geographical footprint in major urban centres? What is the benefit of having more geographical pick-up locations instead of at-home delivery?

3. Is Amazon just bored and looking to invade another market where they are not dabbling in as one huge experiment? They tried this before with the Amazon Fire phones – RIP (and this also was the final nail in the coffin for Blackberry’s BB10 operating system, which I am still lamenting over since it is soooooo much better than Android).

All things considered, I still don’t think Costco has anything to worry about, but definitely this market space is getting quite cozy.

No positions in any of these stocks. Amazon does look like, however, it will need to raise another 15 billion in debt financing, which they should have no trouble doing.

Dividend suspensions – Aimia, and soon-to-be Teekay Offshore

Aimia (TSX: AIM) suspended their common and preferred share dividends today. While this decision could have been entirely anticipated, the market still took the shares down another 20-25%. If you read between the lines from my previous post on them, this should not have been surprising. Nimble traders that were awake around 9:40am Eastern Time could have capitalized on an intraday bounce, but the current state of the union is likely to be short-lived since the company still has to figure out how to work its way out of a negative $3 billion tangible equity situation and pay the deluge of rewards liabilities. This will probably not end up well.

And in a “tomorrow’s news today” feature, it is more probable than not you will see Teekay management finally tuck in their tails and suspend dividends entirely on Teekay (NYSE: TK) and distributions from common and preferred units of Teekay Offshore (NYSE: TOO). When the announcement will be made is entirely up to management but it will likely be before the end of the month. What is funny is that I called it a couple weeks in advance (post is here), while it took a Morgan Stanley analyst a few days ago to actually cause a significant market reaction in the share price while everybody rushes for the exit. Teekay Offshore unsecured debt is now trading at 17% and with their preferred units still at 12%, it doesn’t take a rocket scientist to figure out what’s going to happen next – they desperately need a few hundred million in an equity infusion and they will be paying for it dearly.

As a bondholder in Teekay’s unsecured debt, I’m curious to see how management will bail themselves out this time. Since I do not believe they are interested in losing control, I still believe the parent company’s unsecured debt looks fairly good since there isn’t much ahead of it on the pecking order in the event of an unlikely liquidation event.