This will be a rambling post in no particular order.

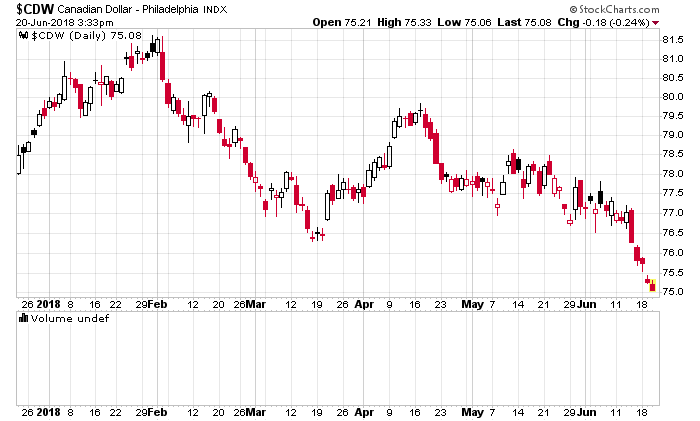

1. The Canadian dollar has tumbled with Donald Trump beating the war drums on the trade portfolio:

This will keep going lower and lower until the Government of Canada realizes that a lower currency doesn’t mean you’re more competitive when you’ve basically killed your own industry. Normally there is correlation between oil prices and the Canadian dollar but this linkage has now been considerably more muted because of WTIC to Alberta oil differentials. Investment has been flowing away from Alberta/SK oil and everything is on maintenance mode.

This will clear the way, however, for the Bank of Canada to raise interest rates another quarter point.

Domestically, this is going to be a disaster for general Canadian standards of living. It seems to be that our largest urban export is continuing to be real estate.

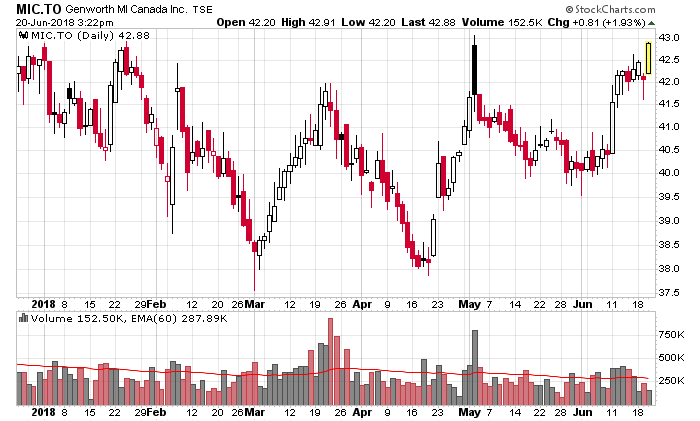

2. Speaking of real estate, bearish market participants in Genworth MI are going to face a short squeeze:

I’m not sure why anybody would want to use Genworth MI as a proxy for Canadian housing when there are so many more other investment vehicles to express this sentiment, ones that are trading well above book value and are making nowhere close to as much money as Genworth MI is on their insurance portfolio.

I’ll send a “hat tip” to Tyler, who writes infrequently at Canadian Value Stocks, for the brief mention of my continuing analysis of Genworth MI. The best analogy I can give is “picking up hundred dollar bills in front of a steamroller” instead of the usual cliche of “picking up nickels”. Genworth MI is claimed to be poised to have a giant collapse, but the variables required to make that happen seem distant at this point in time. Hint: Pay attention to China.

3. Speaking of real estate, the most hyped investment seems to be mortgage REITs and also residential REITs. The cap rates received by purchasers are incredibly low. Example press release linked here, key quotation in the first paragraph:

Northview Apartment Real Estate Investment Trust (“Northview”) (TSX:NVU.UN) today announced that it has agreed to acquire a 623 unit portfolio of six apartment properties (the “Acquisition Properties” or the “Acquisition”) from affiliates of Starlight Group Property Holdings Inc. (“Starlight”). The aggregate purchase price of the Acquisition Properties is $151.8 million (excluding closing costs), representing a weighted average capitalization rate of 4.5%.

A 4.5% cap rate? Do I even need to open a spreadsheet to know that the purchasing side of the transaction is wholly reliant on capital appreciation of the underlying properties for this to make financial sense?

The big favourite in this market is Canadian Apartment Properties (TSX: CAR.UN) and they probably can’t even believe how much their equity has traded up over the past year. They did a secondary at $35.15/unit and probably feel like idiots since just three months later they’re trading at $43/unit.

We drill down into their financials and see that from the last quarter, extended to 12 months, their normalized funds flow through operations (recall that accounting rules will add gross amounts of volatility in REITs due to mark-to-market rules when properties are re-appraised and this difference will be added or subtracted from income, making standard income statement comparisons incomprehensible without going through mental gymnastics) results in a net yield of about 4.3%.

An investment in CAR, therefore will expect to receive 4.3% plus the variable components of changes of rental amounts, property values, financing and operating expenses, and vacancy rates. Will these variable components be enough to give a rational equity investor a higher rate of return as surely nobody would want to take equity risk for a measly 4.3% gain?