Quiet times

Sometimes doing nothing is the best policy and the last two weeks have been exactly that. There’s been a small amount of portfolio adjustments, but nothing too serious. If I have something more exciting to report, I would have. There isn’t anything. Credit spreads are tiny and investors are generally not being very adequately compensated for risk.

In a “would have, should have” world, Lululemon (Nasdaq: LULU) would have been a short in my portfolio a year ago, but that opportunity has now passed. Coach (NYSE: COH) is also on that short list. Both of these are subjected to confirmation bias by females that I know are into these sorts of things. Both of them are trading at valuations which can (now) be considered reasonable (LULU still being a tad expensive, but not as ridiculous as they were before), but both brand names are clearly on the downtrend. In fashion, trends are everything. Apparently Kate Spade (Nasdaq: KATE) is the next up-and-comer and while traditional valuation metrics say this one is very expensive, perhaps talk to some teenagers that have disposable income and your opinion may change.

No positions, just curious. It makes outlet shopping somewhat more tolerable when looking at these various brands from a purely financial perspective.

Year-to-date

Here are some indicies and their year-to-date performances:

Equities

S&P 500: +4.1%

TSX Composite: +7.2%

Nasdaq Composite: +1.6%

However… the winner so far is bonds!

iShares 20+ Yr Treasury Bond ETF (NYSE: TLT): +12.0%

Who would have ever thought?

In the brains of an institutional pension manager

Just put yourself in the shoes of this person – your pension plan has an expected rate of return on plan assets of 7.1% and your actuarial balance is 90% of funded levels for your plan because of weak market performance.

I picked 7.1% because this is an example of a large-scale pension plan (the British Columbia government, for example – others may vary).

How do you allocate to get a 7.1% return?

Perhaps investing in high quality fixed income – even if you’re the world’s best bond trader and get a 200bps spread over Canadian government bonds on A and AA paper (which you are functionally restricted to in your pension plan), you are still well below the 7.1% threshold.

In fact, simple math would state that if you are 50% allocated in high-quality fixed income (let’s just use Genworth MI’s latest A/AA bond offering as an example – 10 years and 4.24% yield), you still need an allocation of equity that would net you 9.96% to “break even” on your 7.1% expected rate of return.

So obviously the deeper the portfolio dives into high-quality fixed income, the higher the return it needs from other components, which would likely come from equity and further up the risk spectrum.

Further up the risk spectrum are BBB bonds, which is the lowest rated bonds that most pensions are allowed to invest in. The yield premium you get on these versus A/AA investments is presently not much better (a lot of low quality debt is trading as if it is a guarantee), but you incur the risk of defaults down the line (in addition to illiquidity when you’re trying to unload them).

Finally, any bond trader will point out to a yield graph and show you that long-duration bonds are trading at high levels (low yields). Probably the reason why most high-quality fixed income continues to trade at low yields is that whenever yields do pop up, they are snapped up by institutional managers that want to fill in that income component of their asset allocation models.

The point is that while historically you could have run a pension plan in the 1980’s to about the year 2005-ish primarily investing in long-dated high quality fixed income securities, today that is clearly not possible.

The other component is typically equities, but an institutional manager will look at the graph of the S&P 500 (trading at all-time highs never seen before in the index) and ask themselves whether they can squeeze more than their 7.1% threshold out of the index when it is trading so high. Nope! Can’t invest here! Additionally, lower sub-indicies such as the S&P 400, and the smallcap S&P 600 are less liquid. Just as an example, the S&P Midcap 400 index has a market capitalization of about $1,600 billion at present. For smaller players this is liquid, but for larger players (e.g. if you have a $200 billion pension plan), it would move the market.

So you move up the risk spectrum, get into junkier debt issues and “alternative investments”, the latter of which is a codeword for illiquid and speculative. They also are cursed by the fact that there is no active market trading on things such as toll roads and other public-private partnerships, and that these investment decisions have to be made very, very carefully made in terms of valuation and expected business results. Still, institutions that need to do higher-yielding investments in size have to venture into these speculative ventures.

So all-in-all, the low-yield environment we are currently in is a function of yield demand – institutions around the world are starving for yield and they are willing to take more capital risk to achieve it.

The smaller individual investor, however, should figure out where the demand is not located and there should be a higher probability of value being located at such points.

Interest rates and Macroeconomic ramblings

This is a rambling post, so be cautioned that there is little rhyme or reason to the thought pattern here.

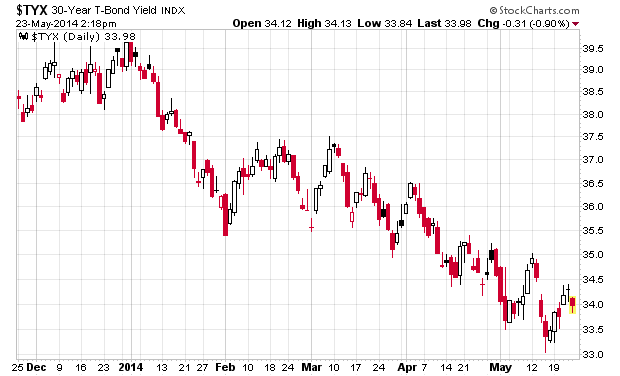

I look at the following chart of the 30-year treasury bond:

The risk-free return is very low at present. Relative to other sovereign entities (e.g. Euro-zone, Japan, Canada, etc.), however, the US 30-year bond actually still looks cheap and this can explain why it is the best performing asset class in 2014 to date.

As an exercise to the reader, please reconcile what we are seeing in front of us:

– S&P 500 is at all-time highs (approximately 1,900 as I write this)

– The economy appears to be plodding along at a low real rate of return

– Inflation is rising but not at ridiculous proportions (yet)

– US currency appears to be making a comeback

– Short-term rates are still basement low (fed funds target is 0-0.25%, but the effective daily rate has been closer to around 0.09%)

– Long-term treasury rates are relative low (see above chart)

– US government is still projecting $500 billion deficits although this is quite better than previous years; other liabilities (e.g. social security) and various other entitlements (e.g. pensions) generally remain huge liabilities and difficult to get a good rate of return

– Almost every retail Joe that is not involved in stock (lottery) picking is dumping their money in a variety of index funds that invest in the same things in the same proportions (Typical Canadian allocation: 40% TSX 60, 30% S&P 500, 30% some fixed-income ETF)

The demographic story is that the bulk of the population pyramid is entering in the stage of life where they are transitioning their capital into income-bearing instruments, which accounts for the very high cost of yield at present.

It remains very difficult to say whether we are entering in the Fairfax world of upcoming deflation despite everything (which would guarantee low interest rates for some time to come), or whether we’re entering some sort of inflationary world (because of all of the available credit, which would presumably translate into spending and consumption).

Although my style of investing does not depend on macroeconomic outcomes, it is always nice to know where you have the winds at your back. In terms of the big world-picture view, it is difficult to tell where these winds are blowing at present.

The only real convictions I have at this point is a general aversion to commodity-related products and a realization that those that are paying for yield are likely paying a premium beyond what the risk/reward ratio would suggest.

In other words, you are more likely than not to find the “hidden gems” amongst the list of zero-dividend yielders (or very low) on the equity side. Due to the “rising tide lifts all boats” phenomenon that we are encountering at present, until we see defaults of junk debt issues that go out for insanely low coupons and high durations, finding these gems is not easy. Most of them have been bidded up.

This leaves potential investment candidates in very un-ideal categories: the nearly illiquid and special situations (e.g. spinoffs, emerging from Chapter 11/CCAA, SEC/SEDAR “fine-tooth comb required because GAAP financials simply don’t explain the story” companies, closed-end ETFs, etc.). Not a lot of pickings here.