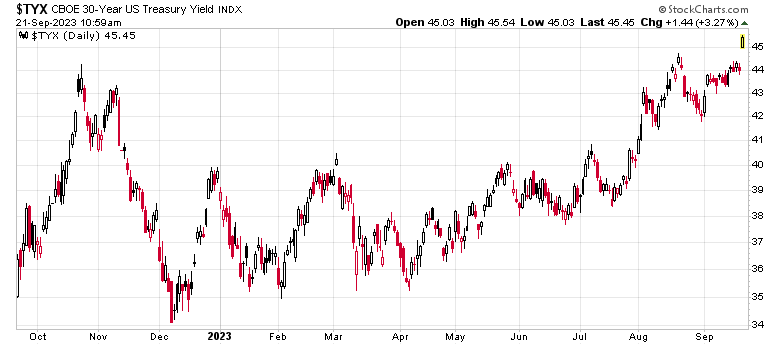

Today in finance we have 30-year government bond yields the highest they’ve been in a long time (early 2011 to be precise):

This yield is a fundamental variable in a lot of risk-free calculations out there. The higher that yield goes, the lower the capitalized asset prices go! After all, if the US Government is going to give you 4.5% a year for 30 years, why should you bother investing in NVidia that is trading at 50 times earnings?

My suspicion, despite all of the dysfunction about the congressional debt limit, is that the world is finally reaching a limit in terms of how much US debt they can swallow.

This doesn’t bode well for Canada either – although our fiscal situation is better than what is going on in the USA, given our economic linkage to the USA we are going to be along for the ride.

There are potential future outcomes where inflation is not contained and rates have to rise further. Already we are seeing the economic stress and strain of 5% short term interest rates. Economically it is akin to a submarine approaching crush depth. If inflation refuses to taper off (just look at the last CPI report and their components), Tiff Macklem (and Jerome Powell) will have to continue plunging the submarine deeper.

One frequently cited counterargument I hear is that by diminishing demand from higher interest rates (people that are choked with debt will have to spend their money servicing debt instead of engaging in discretionary consumption) will have an effect on lowering inflation. This may not necessarily be true considering that it does not factor in the supply side of the argument. For example, in the current Canadian real estate market, demand (based off of sales volume) has definitely tapered lower, but prices have remained relatively high because there has been an equivalent decrease in supply – listings are very low. Currently in that specific market we are at a sort of “Mexican standoff” where there is no volume at the current price.

However, for the overall economy, it appears that non-discretionary components of inflation are continuing to increase in price while discretionary items are being held in check. A great example of this is mobile phone plan pricing – instead of getting 10 gigabytes of data for $40 a year ago, you can now get 20 gigabytes for the same price. That’s a deflation of 50%!

Survival is the name of the game here – look carefully at your portfolio and avoid companies with excessive debt leverage. Keep that cash handy. Finally, the only glimmer of green that I see in the markets today is that of crude oil futures – at US$90/barrel for spot WTI, many of the well-known names out there are pulling in a huge amount of cash flow.