Needless to say, along with the rest of the financial universe, I’ve doing some very rapid weekend research, but have also taken the time to get outside, exercise, enjoy the somewhat cloudy weather and thank my blessings that my fever-free cold that I caught a week and a half ago is finally going away. I’m really getting the impression that a lot of people’s mental health has been sharply declining – decades later, I’m sure historians will figure out that rapid-fire social media is the root cause of all of this social insanity.

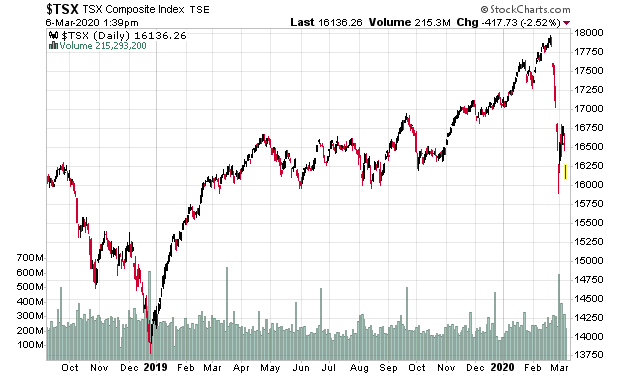

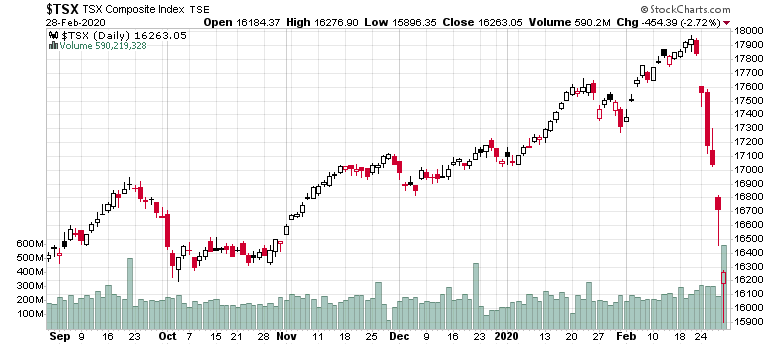

Anyhow, over the past 5 trading days the TSX Composite has dropped 8.9%. It has been one of the sharpest short-term market declines I can ever recall in my history in the stock market – only rivalled by the 2000 tech crash and 2008 financial crisis. Going further back we also have the 1987 and 1989 analogies which exhibited huge one-day crashes, but what we have seen were multiple gap-down days.

See the big volume spike on Friday? That’s a lot of demand for people to flush stocks into cash. It didn’t help that the TSX itself shut down mid-day during one of those panic days. Always remember that in a given trading day the total shares outstanding and the cash outstanding is always constant, it is the price level of the stocks trading that is different, representing a higher “pressure” to unload shares and obtain cash vs. the opposite.

Presumably a lot of stocks have gotten hit in the past five days. When looking at the large-cap market, most of the major names (e.g. ENB/PPL, banks, energy producers, SLF/MFC/GWO/IAG insurers) have been hit pretty badly, but in general, the hit has been a relatively even distribution. Even boring staple companies like Rogers Sugar are down about 10%, the index average. One can infer that the selling pressure has been blanket-wide.

On the US side, even Berkshire (the whole world knows Buffett is sitting on a huge cash stack waiting for the markets to crash) is down 10% from a week ago.

When looking where the damage is disproportionate (which is where you can usually find the better bargains, ideally through mass margin selling) we have the following screen of companies (one day I will increase the width on the template of this site so these tables can display better):

TSX losers at the end of February 2020

5-day change in share price below -20%;

Market cap above $100M;

Share price above $1

| Rank | Symbol | Name | Last | 5d%chg | MktCap ($M) | Comments |

| 1 | ALS-T | Altius Minerals Corp | 9.13 | -82.56 | 384 | Metals |

| 2 | IMV-T | Imv Inc. | 2.95 | -52.5 | 149 | Preclinical Bio |

| 3 | DRT-T | Dirtt Environmental Solutions Ltd | 2.42 | -41.4 | 205 | Manufacturing |

| 4 | MUX-T | Mcewen Mining Inc | 1.21 | -30.86 | 481 | Metals |

| 5 | AXU-T | Alexco Resource Corp | 2.01 | -30.45 | 239 | Metals |

| 6 | BLDP-T | Ballard Power Systems Inc | 12.06 | -30.45 | 2,816 | Alt. Energy |

| 7 | OSK-T | Osisko Mining Inc | 2.8 | -30 | 811 | Metals |

| 8 | PTM-T | Platinum Group Metals Ltd | 2.52 | -30 | 157 | Metals |

| 9 | BU-T | Burcon Nutrascience Corp | 1.23 | -29.31 | 118 | Plant Protein |

| 10 | DII-A-T | Dorel Industries Inc Cl.A Mv | 4.2 | -29.05 | 122 | Wholesale Retail |

| 11 | VET-T | Vermilion Energy Inc | 13.46 | -28.93 | 2,093 | Energy |

| 12 | TMR-T | Tmac Resources Inc | 1.6 | -28.57 | 184 | Metals |

| 13 | SBB-T | Sabina Gold and Silver Corp | 1.33 | -27.72 | 394 | Metals |

| 14 | APY-T | Anglo Pacific Group Plc | 2.2 | -27.63 | 430 | Metals Royalties |

| 15 | SEA-T | Seabridge Gold Inc | 13.22 | -27.24 | 830 | Metals |

| 16 | OVV-T | Ovintiv Inc | 15.51 | -25.75 | 4,030 | Energy |

| 17 | STLC-T | Stelco Holdings Inc | 7.14 | -25.63 | 633 | Base Metals |

| 18 | USA-T | Americas Silver Corp | 3.15 | -25.36 | 260 | Metals |

| 19 | MAG-T | MAG Silver Corp | 11.38 | -24.59 | 985 | Metals |

| 20 | FVI-T | Fortuna Silver Mines Inc | 3.93 | -24.57 | 630 | Metals |

| 21 | EQX-T | Equinox Gold Corp | 9.73 | -24.52 | 1,104 | Metals |

| 22 | LMC-T | Leagold Mining Corp | 3.25 | -23.89 | 926 | Metals |

| 23 | TVE-T | Tamarack Valley Energy Ltd | 1.29 | -23.67 | 290 | Energy |

| 24 | OGC-T | Oceanagold Corp | 1.96 | -23.14 | 1,220 | Metals |

| 25 | FR-T | First Majestic Silver Corp Common | 10.13 | -23.02 | 2,125 | Metals |

| 26 | SVM-T | Silvercorp Metals Inc | 4.27 | -22.64 | 739 | Metals |

| 27 | SCL-T | Shawcor Ltd | 8.42 | -22.25 | 591 | Energy Services |

| 28 | ORL-T | Orocobre Limited | 2.31 | -22.22 | 618 | Metals |

| 29 | WPRT-T | Westport Fuel Systems Inc | 2.53 | -22.15 | 344 | Alt. Energy |

| 30 | BBD-A-T | Bombardier Inc Cl A Mv | 1.02 | -22.14 | 2,320 | Aerospace |

| 31 | MDNA-T | Medicenna Therapeutics Corp | 3.19 | -22 | 112 | Preclinical Bio |

| 32 | SSL-T | Sandstorm Gold Ltd | 7.84 | -21.91 | 1,401 | Metals Royalties |

| 33 | SMT-T | Sierra Metals Inc | 1.8 | -21.74 | 292 | Metals |

| 34 | GOLD-T | Goldmining Inc | 1.45 | -21.62 | 210 | Metals |

| 35 | HEXO-T | Hexo Corp | 1.46 | -21.08 | 415 | Cannabis |

| 36 | PG-T | Premier Gold Mines Ltd | 1.24 | -21.02 | 261 | Metals |

| 37 | DOO-T | Brp Inc | 55.03 | -21.01 | 4,882 | Snowmobiles! |

| 38 | MOZ-T | Marathon Gold Corp | 1.26 | -20.75 | 225 | Metals |

| 39 | EDR-T | Endeavour Silver Corp | 2.14 | -20.74 | 295 | Metals |

| 40 | HSE-T | Husky Energy Inc | 6.39 | -20.72 | 6,423 | Energy |

| 41 | LAC-T | Lithium Americas Corp | 5.53 | -20.55 | 496 | Metals |

| 42 | PRN-T | Profound Medical Corp | 17.5 | -20.53 | 267 | Medical |

| 43 | WDO-T | Wesdome Gold Mines Ltd | 8.54 | -20.48 | 1,178 | Metals |

| 44 | IFP-T | Interfor Corp | 11.93 | -20.41 | 802 | Forestry |

| 45 | PAAS-T | Pan American Silver Corp | 26.57 | -20.33 | 5,574 | Metals |

| 46 | LGD-T | Liberty Gold Corp | 1.1 | -20.29 | 261 | Metals |

| 47 | AYM-T | Atalaya Mining Plc | 2.62 | -20.12 | 397 | Metals |

| 48 | NEO-T | NEO Performance Materials Inc | 7.97 | -20.06 | 305 | Metals |

| 49 | OR-T | Osisko Gold Royalties Ltd | 11.03 | -20.01 | 1,738 | Metal Royalties |

The metals companies (mostly gold-related) are all crashing simply because the price of gold itself has gone into the gutter after day 2 of this crash – gold is not a safety valve if your desire is to hold onto cash rather than assets (think 1929-style deflation). In general, I do not see much value in these types of companies. Thankfully my exposure to gold is strictly limited in (TSX: GCM.NT.U) which will be automatically cashed 30% at the end of March, and it would take a catastrophe of huge magnitude for the rest of the notes to not mature gracefully.

The other companies are energy, and for obvious reasons they are not doing well.

The remainder of companies have interesting features, but for example, a company like Dorel Industries (TSX: DII.B) has exposure to China simply because they have some manufacturing operations there.

So oddly enough, despite this crash in stock prices, I don’t see too much value in the TSX directly as a result of this. Yes, things are cheaper relative to a week ago, but they don’t appear to be dirt cheap.

Even when scanning the TSX fixed income list, the debentures that are trading low are doing so for very obvious reasons (e.g. Just Energy is sitting at 38 cents on the dollar because there is a very real risk that their senior secured creditors are not going to allow a refinancing). There are some issuers in my opinion that are trading near par that should be trading much lower (i.e. their actual credit quality is less than the price of their debentures indicate), but very little in the way in the opposite direction.

The preferred share market has also slide down and has not been immune to the downturn, but this is probably because the 5-year government of Canada bond rate has also slipped – from 1.29% beginning the week to 1.07% ending. This has a disproportionate effect on those rate-reset preferred shares.

When there are huge volatility spikes down like this, there are likely to be soul-crushingly large rallies up, usually at the point where most of the active sentiment has already shifted into a “cashed out” mode. The “risk on” stocks that get hit the most are typically the ones to bounce back up, at least in the very short term. After that, it’s anybody’s guess.

Finally, my barometer of the “Coronapanic” is Alpha Pro Tech:

This measures people’s psychology in a stock chart. This company has 13 million shares outstanding and one look at the volume chart shows the story – it’s traded its entire stack of shares outstanding more than 5 times as people have flipped shares like pancakes.

I must say I badly under-estimated the impact of this Coronavirus and I can clearly be counted in the leagues of people that thought this would blow over and life would go back to normal after a brief panic. When this will stop, who knows – but there is one constant in the markets and that is there is the most money to be made and lost in panics, which is why I’m paying hyper-vigilance despite being poorly positioned going into this thing.