Typically the price of gold is anti-correlated to market fortunes. However, during last week’s market calamity, it has seen a huge price influx, even when adjusted for Canadian currency. When all the world currencies are seemingly being debased, investors retreat into hard assets – this means claims to cash flows (through shares), bonds, and also commodity assets.

My only fundamental issue with gold is that it doesn’t serve much function other than being the psychological crutch of the monetary system. It is a good commodity to store value simply because of other people’s perceptions that it is valuable – paper currency works exactly the same way. When I go to a grocery store and exchange green pieces of paper for actual food I can consume, the person on the other end of the counter presumes they can buy something with the green pieces of paper. The same works for gold.

If you were to take out $100,000 in value in gold you would still have to carry 2.6 kilograms (about 5.7 pounds) of gold. Gold’s density is 19.2 grams per cubic centimeter, so this can be represented in a cube about 5.1 cm on an edge. This is slightly smaller than stacking a 3×3 cube of Las Vegas craps dice. This is quite practical when you consider that the equivalent in paper currency would be 1,000 $100 bills (think about how thick a 500 page laser printer stack is when you shop for office supplies), and you would presumably be able to avoid counterfeiting issues with a gold cube.

I am wondering why a more useful commodity, such as crude oil, has not been bidded up. Maybe one reason is because it would be difficult to stuff a few barrels of oil in your pocket or inside your safety deposit box. Knowing something about regulations concerning the storage of petroleum, it would also be impractical to pump thousands of barrels in a backyard tank.

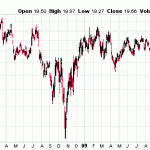

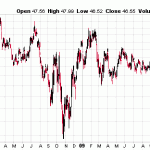

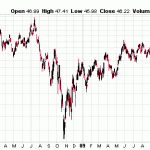

What is mysterious, however, is why shares of gold production corporations haven’t risen in relation to gold prices:

Maybe there is value somewhere in gold equity?