Any time a company you invest in has a significant concentration of its revenues (and/or income) derived from a single geographical source, there is always risk of this sort of thing happening:

DEDHAM, Mass., Sept. 23, 2019 /PRNewswire/ — Atlantic Power Corporation (NYSE: AT) (TSX: ATP) (“Atlantic Power” or the “Company”) disclosed today that its Cadillac biomass plant, located in Cadillac, Michigan, is currently offline following a fire at the plant on September 22, 2019. The plant’s sprinkler system activated and the fire was extinguished by the local fire department. The fire did not result in any injuries or known environmental violations.

The cause of the fire, extent of the damage, and time required to repair the facility are unknown at this time. The Company is assessing the extent of the damage to the facility and will be reviewing the incident with its insurance carriers.

Atlantic Power would like to thank all area first responders for their support during this incident.

The Company expects to provide a further update with its third quarter 2019 financial results when it has determined the extent of the damage, the schedule for the plant’s expected return to service and the financial impact.

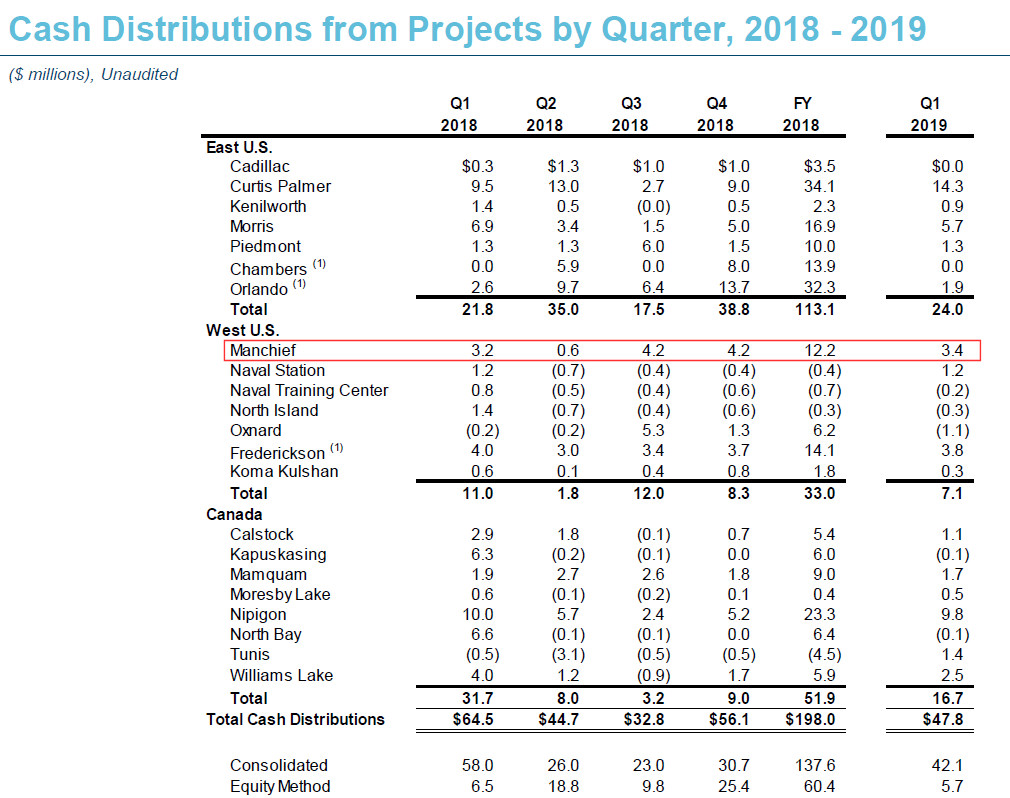

The Company would note that Cadillac contributed $3.4 million to Project Adjusted EBITDA in the first six months of 2019, or 3% of total Project Adjusted EBITDA.

I ask myself whether this could have been picked up in advance, and the answer would have been “yes”.

On the Cadillac News website, early this morning, the following article came up:

CADILLAC — Firefighters battled a blaze at Cadillac Renewable Energy for several hours early Sunday morning.

According to a Cadillac Fire Department press release, shortly after 2 a.m. they received what was being reported as a structure fire at Cadillac Renewable Energy on Miltner Street in the industrial park.

Upon arrival, firefighters noted heavy fire conditions in a large biomass power generation facility. All employees had safely exited the building prior to fire department arrival. At the time, there were three employees on shift.

Firefighters used defensive tactics and elevated water streams to knock down the fire. Once the fire had been reduced in size and severity, conditions allowed firefighters to enter the facility and continue the extinguishment process.

After several hours, the fire was fully extinguished. Damage was primarily confined to one area of the facility, however, significant damages to that portion were noted.

No employees, civilians, or firefighters were injured.

An investigation into the origin and cause of the fire is ongoing. Additional information regarding the investigation will be provided once it becomes available.

The Cadillac Fire Department was assisted at the scene by Haring Township Fire Department, Cherry Grove Township Fire Department, North Flight EMS, Cadillac Police Department, and the Cadillac Utilities Department.

Of course, I’m not the type of person to put an alert on “Cadillac Renewable Energy” or the myriad of subsidiaries that Atlantic Power operates as on my alerts table. I don’t think most people are.

The news hit the airwaves at the first yellow triangle in the following chart:

An enterprising small scale trader could have reasonably gotten about 10,000 shares of liquidity at the bid at the 2.53-ish mark and if they were clairvoyant, could have covered a dime under and made cool thousand. Anything larger than that size and a short term news trader would have run into liquidity issues.

In terms of the actual financial damage, if the plant is out of commission permanently, a very simplistic analysis would be the removal of $6.8 million EBITDA, discounted 10% to June 2028 (when its power purchase agreement expires), or about $39 million present value, assuming EBITDA translates into all cash. That works out to 36 cents per share!

The article noted, “Damage was primarily confined to one area of the facility, however, significant damages to that portion were noted.” – this suggests that there will be a bunch of money spent on repairs and the plant will get up and going again. Insurance should also mitigate some of the damage, although it is not clear whether they just have a facilities insurance or they also have a business interruption policy which would cover the cash flow in the event of a business interruption.

However, the underlying lesson is the following: if a company you owns has one core asset that products the bulk of cash flow (I’m thinking of Gran Colombia Gold and Segovia when I write this), there is always the lingering risk of a single event causing major damage. Hence, there is some value to diversification.