I used to own shares in Rogers Sugar, back in the days when it was still trading as an income trust. I had a slab of units in the mid 3’s and sold them in the mid 5’s, citing that the upside was probably limited from that point. This was one of the companies that I loaded up on during the economic crisis and it paid off. My selling timing wasn’t ideal as they’ve managed to get up to about $6/share before moderating:

I’ve been asked whether this company is a buy or not. Normally I don’t entertain these requests, but since I don’t need to do any additional research on this company that I’ve already written about, I’ll comment.

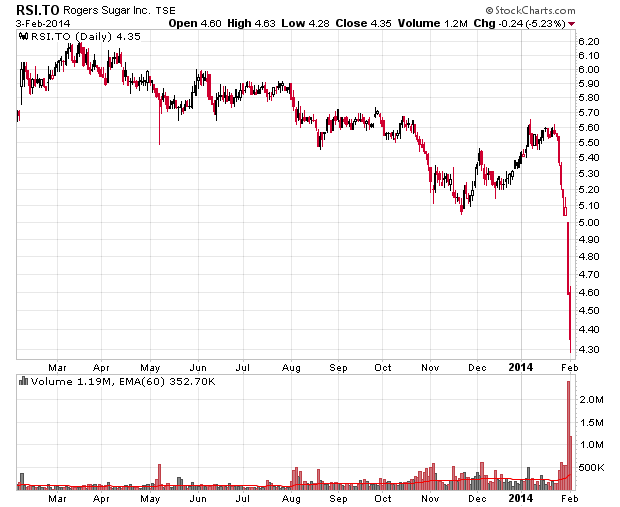

The quick answer is that they are trading within my fair value range. They’ve been well over my fair value range for the bulk of the last couple years. My theory here is that they were perceived as a safe stock with a safe yield, and lumped into every income fund manager’s portfolio as something reliably yieldy but “without risk”. I would say the assessment of income is correct, but the assumption of risk is not, and the market clearly has shown that over the past two weeks of trading.

I’m not sure why they got killed as badly as they have. Their last quarterly report (the catalyst) was not good, but the stock didn’t deserve the 20% bludgeoning they took. There is clearly a lot of other technical factors going on here (stop losses, value investors dumping, margin players dumping, etc.).

Market-wise they are facing a few adverse factors (the crops down south have been better than usual, which will cause over-supply and hence no exports for this year), and also Redpath is seemingly getting good at marketing and beating Rogers – heck, I even notice their product in the local Costco. These margin pressures are not good for the company, but this is the nature of the industry and it has been this way for a long, long time.

They will have to go down further before I’ll consider buying shares.

Also for those wanting to do some fundamental research on the company, just note that reading the GAAP income statement is nearly useless due to the use of derivatives the company engages in to hedge natural gas pricing.