Normally when a corporation is buying out another entity (especially at a premium), the market’s instinctive reaction is to jettison the shares of the purchaser.

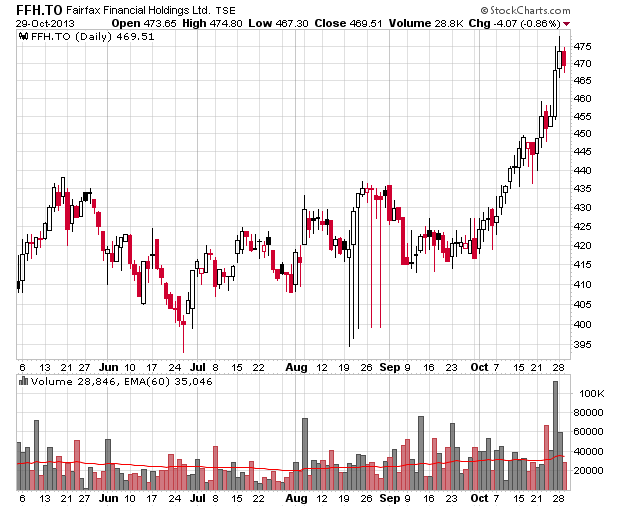

Fairfax’s slow attempt to take Blackberry out has a rather odd effect: Fairfax’s common share price has skyrocketed (at least relative to its historical trading patterns, which has been relatively boring):

There is a deep insider’s game being played with Blackberry and some of this information leaks into Fairfax’s stock price. Maybe I’m reading too much into this (realizing that Fairfax’s 10% stake in Blackberry is only about 5% of Fairfax’s market cap).

My hunch:

1. The terms of the deal were materially struck on October 25th and will likely be announced on November 4th in absence of any other deals;

2. Facebook getting into the scene is priced in as a negative (i.e. potential to pay more, hence worse for Fairfax).

3. The market believes Fairfax is getting a good deal.

Zuckerberg at Facebook is not an idiot and realizes that his $120 billion market cap is not going to last forever and the company needs to branch out. Similar to what Steve Case did with AOL and Time Warner, there is an interesting business case of just sheer diversification of doing an all-stock deal for Blackberry at some double-digit per share price – Facebook stock is now expensive currency and why not do a late 1990’s internet stock type move and purchase something tangible?

Its a low probability outcome, but right now capital is cheap and the market is giving the titans lots of currency to play with.