ARCH is clearly a type of company where the analysts have most of the information well before the retail investor, which makes short-term trading of it a money-losing venture. You can see this in today’s trading action where pretty much most of the professionals got it right.

There is value, however, in making medium-range outcomes, where the playing field is a lot more level.

This is where it gets interesting today, specifically the question of how long this party in coal will last.

Putting a long story short, the demand for steel has increased since 2020’s Covid hit, while global supply of metallurgical coal has decreased. This is causing the current situation where steelmakers are forced to pay up.

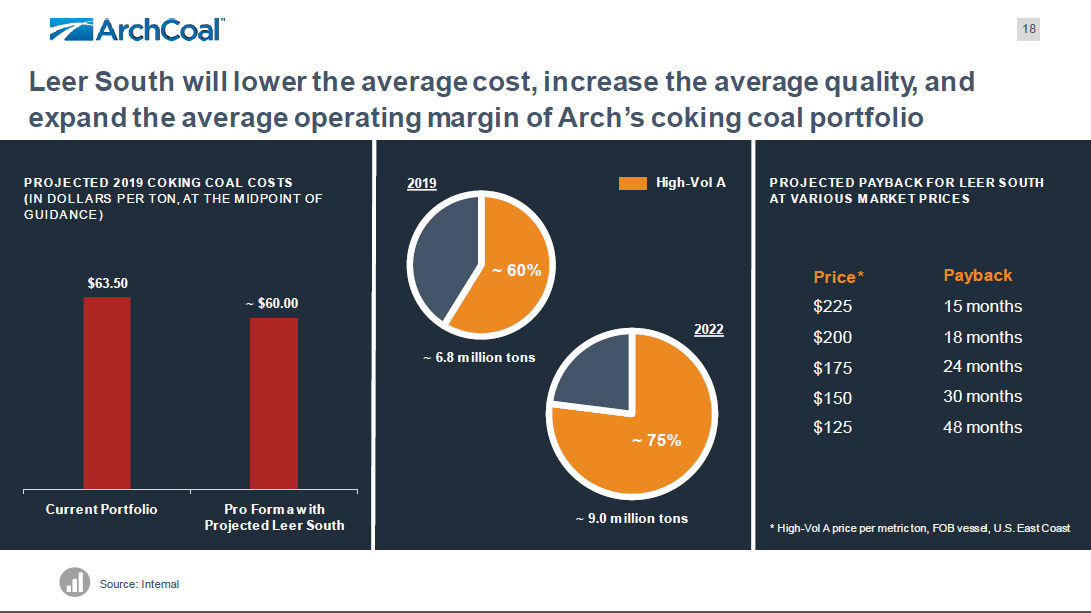

Upon review of ARCH’s Q3-2021 conference call today, we have a company that is working like mad to sell both met and thermal coal. Indeed, they have pre-sold most of their 2022 thermal production at Powder River Basin at a margin that will likely net them about $10/share alone. On the met coal side, they are looking at spot seaborne prices of US$390/ton, and they have already been making sales for next year domestically in the US$200s, plus the added 3 million tonnes that gets produced in the Leer South project.

The majority of 2022 looks locked and loaded and will be incredibly profitable. It’s going to be, conservatively, about $600 million in free cash, probably more. Most of the capital expenditures will taper in 2022 as the last major construction project (Leer South) is done, and will clock around $125-150 million for the entity.

Mentally, this 2022 incoming cash flow can already be subtracted from the valuation as this is a known quantity. Factoring in Q4-2021, you can subtract about $50 of so off the stock price for the rest of 2022. The number might be even more, depending on how much high-priced met sales they can get off.

The question and value that an investor can bring to this point is what the heck is going to happen in 2023 and beyond (they’re already trying to sell 2023 production).

Right now, the stock is trading at a Price/2022 FCF of a low single digit multiple, perhaps around 2 and a half. Your valuation exercise, and what the sharps with the real information do not have, is what economic conditions are going to exist a year from now?

If things continue as-is, ARCH continues to be a dramatically undervalued stock – for each and every year these conditions are expected to continue, you can pack on another $50 or so to the stock price beyond what you currently see.

If you expect a crash in coal pricing (e.g. other international jurisdictions get their act together to ramp up supply, or steelmaking crashes), then you’ll take a hit. Depending on how bad it is, you could see a quarter of your investment evaporate.

Your typical spreadsheet analyst probably loves technology companies because their revenue curves fit really well to models. Earnings are predictable, and everybody is happy. However, the real value in investing is made in very jagged situations like this one.

Management is taking a very cautious approach with capital allocation. Their first priority is to pay down as much debt as possible (which they will be able to do in 2022) and then pre-pay some asset retirement obligations with the thermal business. They should be able to do both in the first half of 2022. They instituted a nominal dividend (25 cents/share/quarter) which will get some income ETFs in the mix, and then sometime in 2022, if the stock is still at their current levels and the commodity is still at highly profitable levels, will probably institute a buyback, although at a lesser scale than the overkill they engaged in 2019. I would expect the dividend to also increase in 2022.

Considering that costs on their met coal side is around US$60/ton and the commodity price is well into the triple digits, there would have to be a considerable crash before that business reverts back into a breakeven mode. It’s a pretty big cushion, albeit the coal market at this moment must feel like the conditions that traders of GME were facing at the end of January this year.

I think once the coal tourists get shaken off with the existing volatility and relative price disappointment (“Why isn’t this thing trading higher than 2 times earnings???”), the stock heads higher. The tough part, however, will be the day where you sell it at 4 times. Not today.