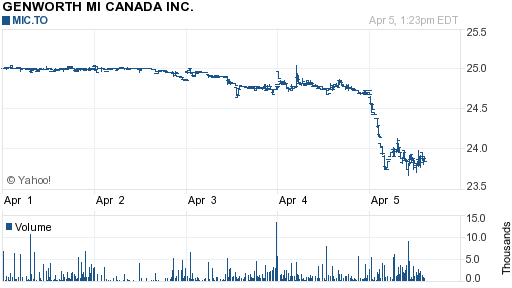

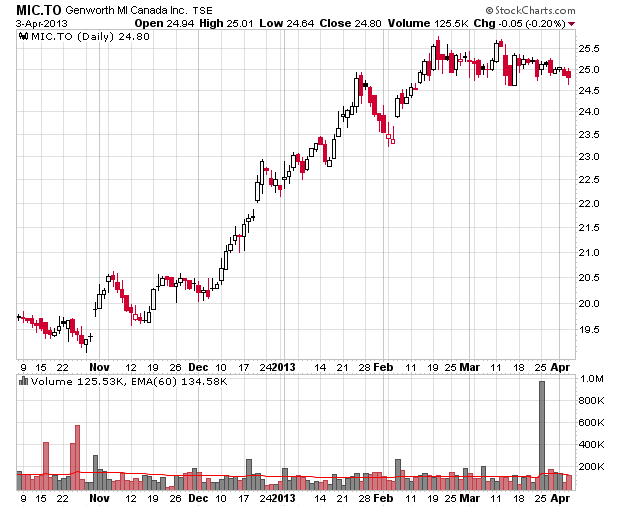

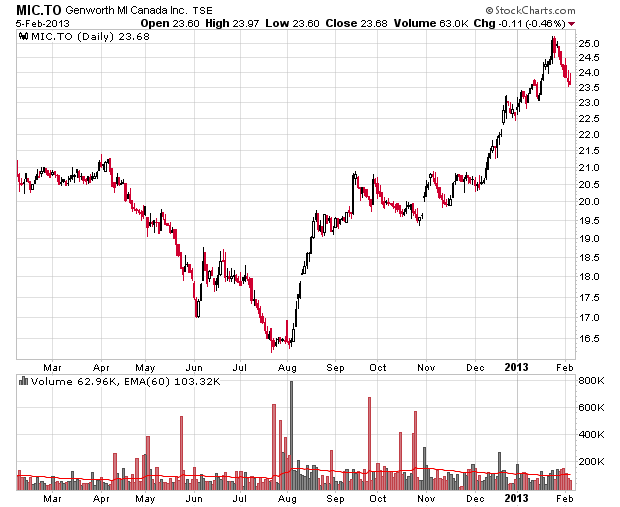

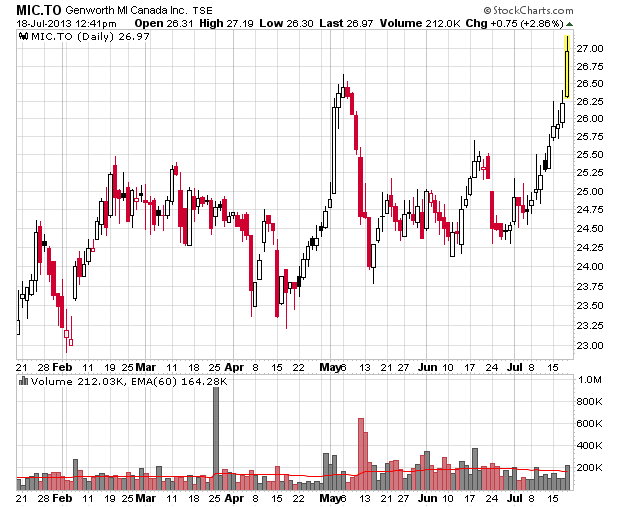

Genworth MI (TSX: MIC) has been treading water since last March, but lately seems to have caught some upside momentum:

Possible substantiations why the price is rising:

– Macroeconomic aspects of the Bank of Canada determining to keep short term interest rates low (which will enable more principal payments on mortgage and thus reduce default risk);

– No big blowups in the Canadian housing market;

– The stock repurchase of 71,540 shares a day since the last course issuer bid has been announced. In May and June they took about 2 million shares out of circulation – just over 2% of their shares outstanding, which will boost earnings per share by about 7 cents a year. This will also save the corporation about $2.5 million in cash flow a year from not having to pay out the associated dividends. They have sufficient cash reserves to keep this up for quite some time.

– Notably such buybacks (especially at around the $25 price they executed the buyback with in May and June) are accretive from a tangible book value perspective, i.e. every dollar spent in repurchasing equity actually increases the per-share tangible book value.

It looks like they were able to mop up the willing sellers out there at the $24-25 price range and the market is now bidding the shares at a price that is closer to fair value, but my own calculations suggest that there is more upside.

Management should continue repurchasing shares until roughly $30/share as these repurchases are clearly adding value. After that, they should taper the buyback and accumulate cash and consider a special dividend.

The corporation is generating considerable sums of cash and will not be in a position needing to raise capital. Its next debt maturity is December 2015, where they have a $150 million issue outstanding at a coupon of 4.59%. Considering they currently have $289 million in free cash balances, this will not be a problem to either just pay it off or to re-borrow the amount for a modest amount of financial leverage. This decision will likely take place sometime in the first half of 2015. If interest rates rise, they’ll just repay the debt. If interest rates continue at the historically low rates we are currently experiencing, then they’ll be able to get a good rate.

Disclosure: I do own shares, it is just over a year since I last took my position.