Disclaimer: My prediction of winners has nothing to do with the endorsement or non-endorsement of any particular candidates or policies.

Canadian Finance and Economics

Disclaimer: My prediction of winners has nothing to do with the endorsement or non-endorsement of any particular candidates or policies.

KCG Holdings (NYSE: KCG) is probably best known as previously being “Knight Capital”, which was one of the top-tier US market-making firms back in the days when the Nasdaq traded in quotations of 1/16ths.

The second reason why they are well-known is because due to a badly botched software upgrade on August 1, 2012, where their algorithms managed to incur $440 million in 30 minutes of trading losses before technicians were able to pull the plug. I am quite confident with an unlimited amount of equity on my Interactive Brokers account I could not manage to lose that much money using my fingertips and mouse.

The company was forced to recapitalize and what incurred after was a reverse-takeover by the algorithmic trading firm GETCO. The existing shareholders were massively diluted and this functionally served as a way for GETCO shareholders to liquidate their holdings (backed by General Atlantic). The combined entity was renamed “KCG” (yet another example of a firm acronym-ing their name) and what ensued was an internal purge of legacy Knight Capital personnel. The transition at this time is more or less complete.

The corporation still makes the bulk of their money through market making and related trade execution services. Their prime competitors include other high-frequency trading firms, including the newly public Virtu (Nasdaq: VIRT). In general, the firm makes money when market conditions are volatile and they operate at a loss when volatility is quite muted.

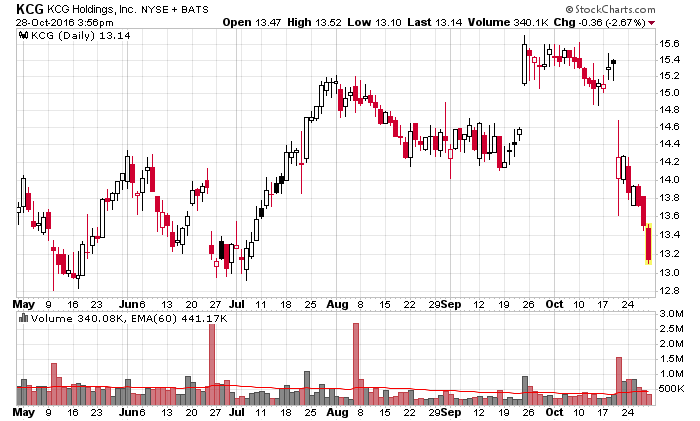

The July to September quarter was a disaster for KCG (and other market-making entities, including Interactive Brokers), while the April to June quarter was quite profitable (think about Brexit!).

Since the last quarter’s results, KCG shares have tail-spinned:

The business, quarter by quarter, is highly volatile. In the Q2-2016, they reported operating revenues of $280 million, and in Q3-2016 they reported $200 million. As you might tell by this seasonality, it creates volatility in the stock as quantitative algorithms that purchase and sell shares on fundamental data generally go wild with companies like these.

Profitability also varies. The corporation is still trying to cut costs and become lean and mean (like Virtu), but it is taking them time to get to that position where they can be profitable in a very low volatility environment like the last quarter. On the aggregate, they are profitable in the medium run, which means I do not regard them as much of a risk at this moment (unless if their programmers decide to botch up another software upgrade like what happened in August 1, 2012).

The balance sheet is a little more interesting.

Its tangible book value is $15.54/share at the end of September. The underlying corporation has $508 million in cash, and a whole host of financial instruments that vary from quarter to quarter as they maintain an inventory for market making purposes (13F-HR form attached for illustration). In addition, they also own 13.1 million shares of BATS (Nasdaq: BATS), which is presently in the middle of getting acquired by the CBOE (Nasdaq: CBOE) sometime in 2017. The BATS stake is worth a pre-tax amount of about US$380 million at current market value.

Where my accounting experience comes in handy is how this is reported. You would think that owning US$380 million in a publicly traded entity would be reflected as US$380 million on the balance sheet, but this is not the case with KCG’s BATS stake. Instead, it is reported under the equity method of accounting. I will leave out the complications and state that it is reported as $94 million at present on the balance sheet. As KCG sells their BATS shares, the differential between sale price and their carrying value on the asset side will be reported as a gain (subtracting a provision for income tax).

So there is actually about $285 million of pre-tax money that is bottled up and waiting to escape. After taxes, this will be about $200 million leftover (using 30% as a basis – the actual rate may be higher).

You can see why most people do not have the time or patience to go through this minutiae.

On the liability side, we have one significant liability – $465 million face value outstanding of secured senior debt, with an 6.875% coupon maturing March 2020. The debt restricts the corporation to repurchasing shares at a fraction of KCG’s income (if you care to read the fine print, it is available on this 8-K filing) in addition to other nitty gritty details that I will omit from this post.

KCG initially issued $500 million in debt, but decided to repurchase debt at a discount to market earlier this year, when their debt was trading at about 89 cents on the dollar.

Readers of this site perhaps would not be surprised to know that I decided to purchase a decent-sized block of debt at around 90 cents earlier this year. My first disclosure of that purchase is in this post. Unless if the corporation decides to do an August 1, 2012-style blow-up, I regard it as virtually impossible that they will be unable to pay back this debt.

The company has also been actively engaged with the repurchase of its equity (and warrants related to the GETCO merger) at values that have been below book. They conducted a dutch-auction tender last year with excess capital, and they have not made sufficient amounts of money this year to conduct further stock repurchases – their authorization after the previous quarter was a paltry $2 million. However, they can liquidate BATS shares and use those proceeds for equity buyback purposes.

Considering the firm is now trading at a 15% discount to tangible book value, any equity repurchases would be accretive to their book value, in addition to being an EPS boost whenever the markets are volatile enough for them to make money.

So this is a compelling business with a relatively wide moat (market-making is not as easy as initial perceptions may seem), a decent balance sheet, and reasonable prospects for much better business conditions (did I say anything about Donald Trump in my previous post?). It is a company that would find better business conditions when there are higher amounts of market volatility, and assuming they can keep some sort of competitive business edge on the algorithmic side of things, they should be able to generate positive cash flows.

In other words, the downside appears limited, but the upside is less defined.

A question of what their terminal value would be is an interesting study – one would think that if they decided to go private (which would be a legitimate avenue considering everything presented above) that they could do so at a share price obviously above the US$13.10 they closed at today. Management has made promotions of aiming for a “double digit return on equity” in 2017, which I believe is generous, especially on the operating side, but if they get anywhere close to this (or even half of it), the market should value this well north of US$13.10.

So I’m in. Both the equity and debt.

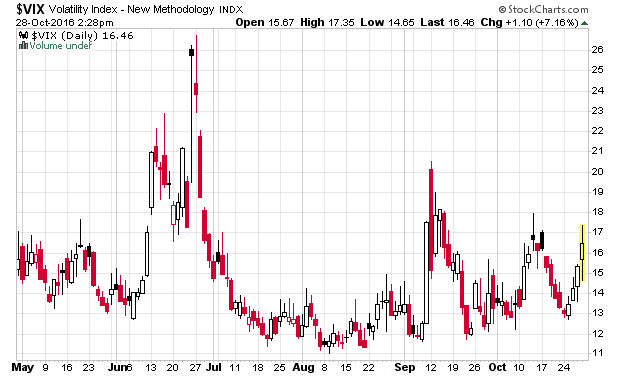

Mark November 8, 2016 on your calendars – the date of the US Presidential Election.

Until then, no major market participant is going to be doing anything, short of the knee-jerk reactions from quarterly earnings reports.

You’re also starting to see a build-up of volatility which bettors are using to hedge:

And yes, Donald Trump becomes the next president. This isn’t an endorsement of him, but rather what I have been saying for the past year and a bit. This is an election where the standard calculus does not work, and people are continuing to make the mistake of using those lenses in a very different environment (similar to the error that the Conservative Party of Canada in the lead-up to the 2015 election).

Pinnacle Sports had Trump at +580 (roughly 1-in-7) to win a week ago and now he is at +280 (roughly 1-in-4), so the betting markets have been very volatile.

Also I have noticed most Canadians use Canadian lenses to look at what is going on in this very American election. Most of the time the political culture is similar, but this is a very special situation.

Once upon a time, I had invested some money in David and Henderson Income Fund, which was back in the days when a lot of viable corporate operations were structured in the form of an income trust. I made some reasonably quick capital gains, sold, and never looked back.

Davis and Henderson, similar to Kentucky Fried Chicken, Ernst and Young, PriceWaterhouseCoopers and many other establishments, decided to abbreviate their corporate name to their initials and become D+H Corp (TSX: DH). Considering that their previous business was the printing and processing of Canadian (paper) cheques, diversification of their business was correctly considered and for the most part, they made a fairly good transition into the broader realm of providing financial technology services for big banks.

You can see in the 10-year chart that this has really worked for them, and the market has been on their side, until recently:

What you don’t see is that in today’s trading, they fell 43% on a quarterly announcement (closing at $16.25/share, with a low of $14.97), bringing their stock price to levels frighteningly close to what I had invested back in 2010 with a cost base of $16.10 per unit. This was certainly a case of “back to the future” for Davis and Henderson.

The question of course is whether the six or so years it has been since I had last invested in them, whether they were worth taking another stab at again.

D+H’s fateful decision was the acquisition of Fundtech on March 30, 2015 (which closed a month later). In this acquisition, they issued many hundreds of millions of debt (in addition to doing a secondary offering at $37.95). Unfortunately, while the acquisition was designed to represent a diversification away from their traditional businesses, it has not materialized into anywhere that could be financially rationalized with the price paid. It has also bloated D+H’s balance sheet with the haunted scars of an additional $1.7 billion in goodwill and intangibles, and when considering their pre-existing goodwill and intangibles, they are sitting on a negative $1.3 billion of tangible equity.

Putting this into plain English, their balance sheet is a train wreck.

Train wreck balance sheets can only sustain themselves with positive cash flow, and continued good credit, as the generosity of lenders will be able to see them through.

For the first 9 months of the year, they have generated $167 million in free cash flow. A majority of this goes to dividend payments ($90 million), and the rest of it goes to debt repayment and acquiring other intangibles.

The problem is with the last quarterly result – it is quite evident that the corporation, on a consolidated basis, has flat-lined. While they still generate a very healthy amount of cash, it is obvious that they will be receiving future stress in the form of being able to repay debt as it matures.

They face the following debt situation:

They have an immediate maturity coming in June 2017, which they should be able to pay off with existing cash flow and/or their revolver without issues. The issue is what happens when they start getting into the bulk of their 2021-2023 maturities.

The math is simple – if they continue paying dividends at their current rate, they will have about $100 million a year in cash to acquire businesses (more intangible assets on the balance sheet) plus debt repayment. They will not have nearly enough to pay off the bond maturities without getting another extension of credit from bondholders.

Considering all of the bond issues and the revolving facilities are secured debt, you can be sure that the banks that supply the revolving debt are going to be nervous about using their money which is pari-passu to bondholders – which means that something is going to have to be negotiated in a couple years.

My guess is that the dividend is going to get slashed in half.

In terms of valuation, the balance sheet situation would make me quite uncomfortable as an equity investor. While I see the value in the cash generation potential of the underlying businesses (notwithstanding the fact that cheque processing is a dinosaur industry and is decreasing accordingly), I do not believe a leverage-adjusted valuation of this business is attractive at present prices.

For now, D+H is still a “pass” in my books. I did sell them at $21 back in the year 2010.

Imagine my initial surprise when I saw a news feed that Genworth had been bought out. Unfortunately for me, it was Genworth Financial (NYSE: GNW) and not Genworth MI (TSX: MIC).

Genworth Financial is being taken over by China Oceanwide Holdings, chaired by Lu Zhiqiang, who apparently has a networth of $5 billion.

In the press release, there are scant details. They mentioned the buyout price and the intention of the purchaser to inject $1.1 billion of capital into Genworth to offset an upcoming 2018 bond maturity and shore up the life insurance subsidiary, but the release also explicitly stated a key point:

China Oceanwide has no current intention or future obligation to contribute additional capital to support Genworth’s legacy LTC business.

The LTC (long-term care) insurance business is what got Genworth into trouble in the first place, and its valuation is the primary reason why the company’s stated book value is substantially higher than its market value.

The press release also declared that this is primarily a financial acquisition rather than a strategic one, with management and operations being intact.

One wonders how long this will last.

Since Genworth Financial controls 57% of Genworth MI, it leads to the question of what the implications for the mortgage insurance industry will be – and it is not entirely clear to me up-front what these implications may be. Will the government of Canada be comfortable of 1/3rd of their country’s mortgage insurance being operated by a Chinese-owned entity? What is the financial incentive for China Oceanwide’s dealings with the mortgage insurance arms of Genworth Financial (noting they also own a majority stake in Australia’s mortgage insurance division)?

One thought that immediately comes to mind is that if Genworth Financial is not capital-starved, they will no longer be looking at ways to milking their subsidiaries for capital. In particular, if Genworth MI decides to do a share repurchase, they might opt to concentrate on buying back the public float (currently trading at a huge discount to book value) instead of proportionately allocating 57% of their buyback to their own shares (in effect, giving the parent company a dividend). This would be an incremental plus for Genworth MI.

Finally, one wonders what risks may lie in the acquisition closing – while it is scheduled for mid-2017, this is not a slam dunk by any means. Genworth Financial announced significant charges relating to the modelling of the actual expense profile of their LTC business and it is not surprising that they decided to sell out at the relatively meager price they did – there’s probably worse to come in the future.

However, as far as Genworth MI is concerned, right now it is business as usual. There hasn’t been anything posted to the SEC yet that will give me any more colour, but I am eager to read it.

(Update, early Monday morning: Genworth 8-K with fine-print of agreement)

Yes, I’ve read the document. Am I the only person on the planet that reads this type of stuff at 4:00am in the morning with my french-press coffee? Also, do they purposefully design these legal documents to be as inconveniently formatted as possible, i.e. no carriage returns or tabs at all?

A lot of standard clauses here, but some pertaining to subsidiary companies (including Genworth MI), including:

(page 47): Section 6.1,

the Company will not and will not permit its Subsidiaries (subject to the terms of the provisos in the definition of “Subsidiary” in Article X) to:

…

(viii) reclassify, split, combine, subdivide or redeem, purchase or otherwise acquire, directly or indirectly, any of its capital stock or securities convertible or exchangeable into or exercisable for any shares of its capital stock (other than

(A) the withholding of shares to satisfy withholding Tax obligations

(1) in respect of Company Equity Awards outstanding as of the date of this Agreement in accordance with their terms and, as applicable, the Stock Plans, in each case in effect on the date of this Agreement or

(2) in respect of equity awards issued by, or stock-based employee benefit plans of, the Specified Entities in their respective Ordinary Course of Business and

(B) the repurchase of shares of capital stock of Genworth Australia or Genworth Canada by Genworth Australia or Genworth Canada, as applicable, pursuant to share repurchase programs in effect as of the date hereof (or renewals thereof on substantially similar terms) with respect to such entities in accordance with their terms);

(note: Genworth MI’s NCIB expires on May 4, 2017)

(page 53): (e) During the period from the date hereof to the Effective Time or earlier termination of this Agreement, except as set forth on Section 6.1(e) of the Company Disclosure Letter, or as required by applicable Law or the rules of any stock exchange, the Company shall not, and shall cause any of its Subsidiaries that are record or beneficial owners of any capital stock of or equity interest in Genworth Canada or any of its Subsidiaries not to, without Parent’s prior written consent (which consent, in the case of clauses (ii)(B) and (iii) below (and, to the extent applicable to either clause (ii)(B) or clause (iii) below, clause (iv) below) shall not be unreasonably withheld, conditioned or delayed):

…

or (z) any share repurchases that would not decrease the percentage of the outstanding voting stock of Genworth Canada owned by the Company and its Subsidiaries as of the date hereof)

(note: Hmmm… this does open the door for repurchases).

I’m still unsure of the final implication on Genworth MI other than the fact that if this merger proceeds that the parent company is going to lean less on their subsidiaries for capital.