It has almost been a month since I have posted, but I have been quietly stalking targets of opportunity but still remain very defensively positioned. The economic landscape out there has deteriorated somewhat and central banks are trying to get ahead of the curve by cutting interest rates. Everybody has been pointing out that this is usually indicative of bad things happening and as a result, there has been a grab for yield, especially when you look at the Canadian preferred share market.

However, something quite interesting flashed on my radar – something that I would have never anticipated taking a position in a year ago, but have just done so.

I have (post-crash from their last quarterly report) taken a modest position in Dollar General (NYSE: DG), the largest dollar store chain in the USA. With the onset of inflation, “Dollar Store” is a misnomer now, but if you want a close comparison, just walk into a Canadian Dollarama and you will have the same feel (although I must say the American dollar stores tend to have better selection and value than the Canadian version!).

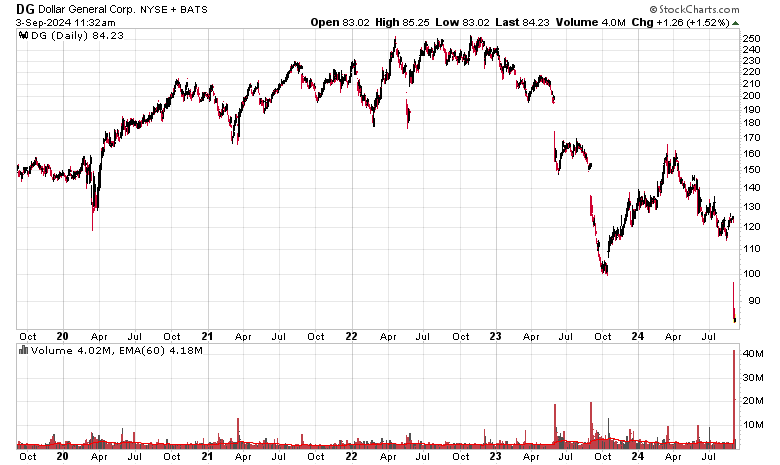

The chart is an absolute train wreck:

You have to go back to late 2017 since the stock traded this low.

I’ve done the core of my research on this just over a year ago when it started to fall from market grace from US$250 in November 2022 and I closely examined it at September 2023 but decided to take a pass. The last quarterly report had me dusting off the cobwebs from my notes and memories and re-reviewing the situation and I think it is more favourable today than it was back then.

To summarize the thesis of this investment, it is a simple regression to the mean thesis, coupled with some economic protection by virtue of the sector that the lower half of the economic cohort flock toward (in other words, economic misery should benefit this company as a consumer staple provider). As investors of Dollarama (TSX: DOL) know, the store features “Amazon protection” but also a degree of Walmart protection. Temu is probably the largest competitor in this respect. The market segment is stable and there is a consider amount of incumbency protection with amortization of fixed supply chain costs.

The stock has gotten nailed on not meeting expectations – primarily that net margins have fallen off a cliff. While gross margins have remained relatively steady, SG&A expenses have ballooned considerably and this has resulted in reduced profitability.

This suggests that there is a management problem. That said, most of the upper executive suite are only in their capacities from 2023 – notably the CEO was the CEO from June 2015 to November 2022 and only took the reigns again on October 2023. Corporations of this size and scale will take some more time to regress to proper metrics. The issues should have been acutely obvious, but being able to make adjustments financially will take time – historical contracts that get signed (e.g. crappy lease locations, supply agreements, etc.) will need to run off before being renegotiated on more favourable terms.

I also note that in the 2021, 2022 and 2023 fiscal years (note: ending January of the year), they blew nearly $8 billion in share buybacks – buying back stock at their all-time highs and at levels wayyyyyyyyyy higher than what they are trading at today.

Wage and cost inflation is also an issue, but this competitive matter will affect other industry participants and will get baked into selling prices.

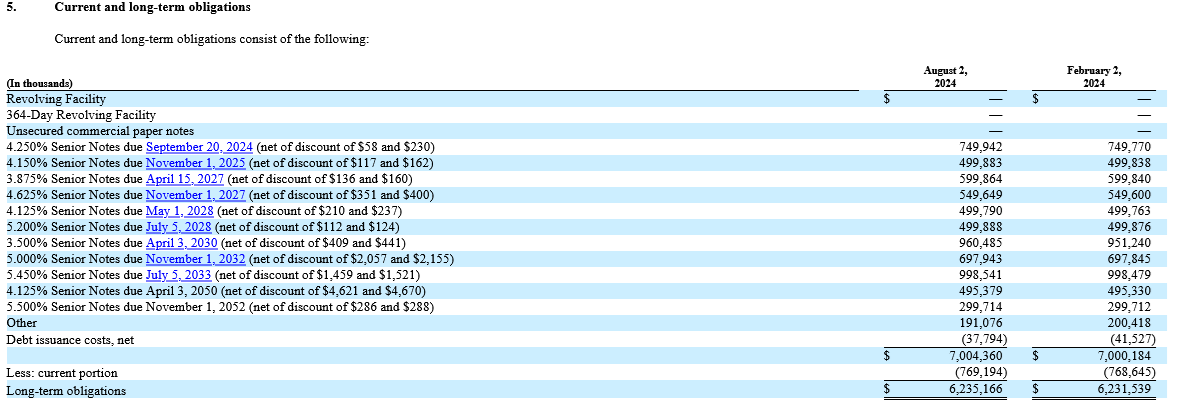

Other than the large amount of lease liabilities outstanding (which is natural for a retail business), the company has about $7 billion in debt outstanding which, given their cash flows and presumed stability of their business, is not excessive:

One would have wondered how stronger the balance sheet would have been had they not engaged in value-destroying buybacks, but I digress!

I do note that the July 2028 and April 2030 tenor of debt trades at 4.9% and 5.0% yield to maturity, respectively – they should have no problem refinancing current maturities at acceptable coupons. There is also a $2 billion revolving facility that remains untapped.

I expect, after some fireworks, that the company in a few years should be able to post EPS well north of $10/share. Choose your P/E multiple to slap onto the stock price and it seems like a reasonable risk-reward.

Finally, I will make one last comparison. DG had about $40 billion in sales in the last 4 reported quarters. With a market cap of $18.5 billion, this gives it a P/S of less than a half. We look at Dollarama and they have CAD$6 billion in sales and a market cap of CAD$37 billion, for a P/S of over 6! You would think Dollarama is selling AI chips or something, but instead the only chips they are selling are Pringles and Lays! Buying some long-dated puts on DOL (and indeed, the implied volatility on them is rather cheap) is something I’ve been toying with – if they break it is going to be as hard as Dollar General and you’ll see at least a 50% correction in the stock price.

Hey Sacha,

Did you look at Dollar Tree as well and possibly willing to share a comment or two? Equally beat up, just reported some bad earnings, also had a bit of a management shake-up, and have a mess at Family Dollar that should give some low hanging fruit to possibly improve operations and earnings.

After today, DLTR’s comps are roughly in the same league as DG. Both are suffering from the same broad issues. Retail is a miserable industry, after all……

Five Below has also been smoked this year. I think Dollarama’s management is way better than DG and DLTR. The stores are stocked and a lot cleaner.

Btw, majority of DG arguments here (financial position, valuation, market conditions etc.) are also applicable to EMPa, which also looks extremely cheap vs other Canadian competitors.

Not sure I would agree with this, specifically comparing EMP.a with DG/DLR/etc. L is a better comparable. That said EMPa’s valuation doesn’t look outlandish although it should be valued as a zero to rate-of-GDP+inflation in terms of profit potential given its market.

missed this reply somehow…

No, obviously EMPa’s network / business is not comparable to DG / DOL, but other features are very similar:

I’d agree EMPa’s valuation is relatively cheap, although on an absolute basis can be arguable. Almost everything yield-y or income trust cashflow-like is getting bidded up with these expectations of rate cuts. It is quite annoying.

Really nice write up, thanks

Dollarama (TSX-DOL) continues to post incredible results all things considered: 45% gross margins and insane amounts of profitability. For all that people like to complain about grocery retailer’s price gouging, they should be looking at DOL! (44% gross margins vs. 32%!).

It is pretty obvious a bunch of short sellers got burnt today in trading. For sure DOL might be looking at using its inflated stock as currency for a cross-border merger in case if they wanted to compete in the USA…

DG reported today. Stock is down slightly, it was somewhat elevated due to competitors (DLTR, FIVE) reporting relatively better than expected results, while DG’s performance was slightly more tepid. Market is taking down the stock presumptively due to lack of anything concrete (e.g. no stock buybacks, no 2025 visibility on results, etc.) but in my books it looks like the second derivative inflection (i.e. the stabilization of results from the artificially high Covid period) is in course.