I don’t like using this sort of language (mainly predicting a crash), but the following are some tea leaves that I am reading in the teacup:

* The market has completely baked in the fact that the money spigots from the Federal Reserve is coming to a close. Yields are rising (take a look at the Bank of Canada).

* Speculative issues (specifically on housing, and small-cap venture type firms) are getting dumped away. Just look at the TSX Venture, or anything resource-based on the TSX (including most commodity issues).

* Likewise, leveraged financial products (e.g. most REITs, financials) are trading down. For example, Genworth MI (TSX: MIC) has traded down over the past month from its highs of about $40/share (where I was fortunate enough to get rid of a bunch of it). I will be able to attribute this due to the implied real estate market risk in Canada, combined with an anticipated increase in interest rates. Compared to the financing firms (HCG, EQB), I would view mortgage insurance as being relatively better in terms of continuing to provide earnings and cash flows. Tangible book value is $34.11 from the previous quarter so the company is still not a huge bargain at present prices.

* The strength in the US currency is now starting to weigh in on commodity prices and this is not good for Canada’s economy in general.

* Liquidity appears to be entirely centered around large cap issues.

So here are some general ideas with the assumption that you’re going to bank on a market crash (or less dramatically, a correction):

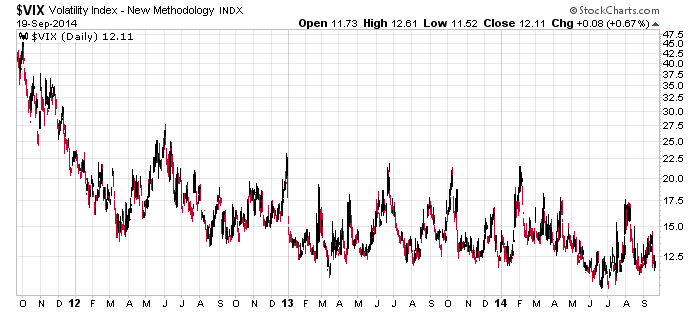

* Volatility futures – I bring to your attention the following 3-year chart of the VIX, which is correlated deeply to the implied volatility you get on short-dated S&P 500 index futures:

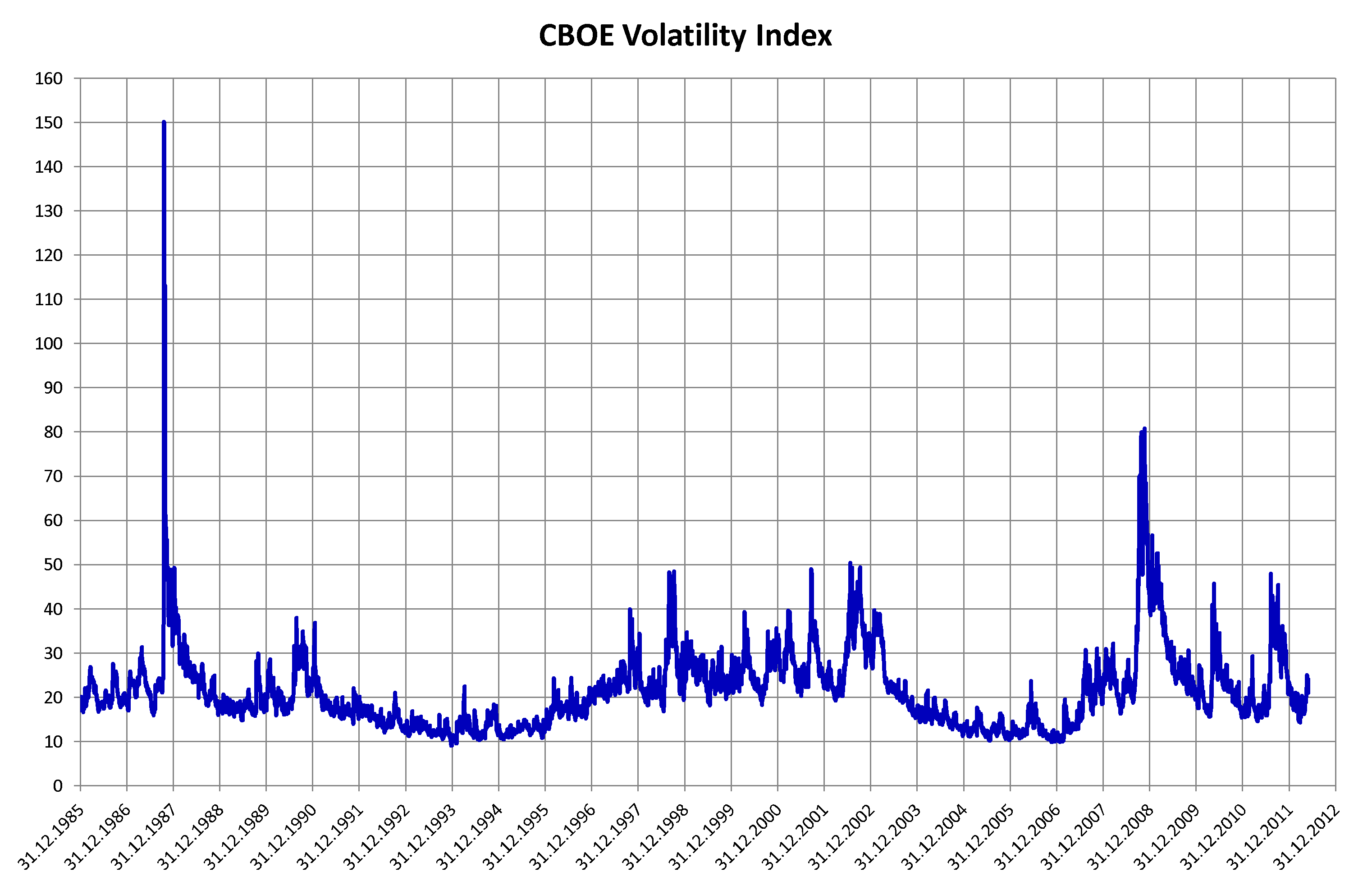

Be warned that it is not unusual for this index to be well below 20 for extended periods of time (e.g. a long-dated chart is here).

* Buying puts on the Russell 2000 (IWM). If there is a flight to liquidity, almost by definition less liquid small-cap issues are going to receive the brunt of increased demand to offload them into the marketplace, resulting in lower prices.

You do pay for this, however – a January 2015 at-the-money put on the Russell 2000 is at about 18% implied volatility, while the S&P 500 is at 12%. The S&P 400 midcap (considerably less liquid) is around 14.5%.

* Buying long-dated treasury futures.

* Or even more conservatively, just holding onto plain old cash and brace for impact.

In general, it appears that we’re headed to some sort of decompression of the utilization of leverage, which will have ripple effects.

{kind=link}