I rarely make investment decisions as a result of macroeconomic analysis. I find that it is too easy to confuse correlation and causation, and also it is too easy to miss data that one should be considering as part of an analysis – i.e. it is the things that you don’t know that kill any way to glean superior insight.

I still try my best to piece together certain pieces of information to strengthen my belief on where the market currents are headed – even if something gives you a half percentage point edge on a coin toss, while you might not notice it if you flip a coin a few times, over a period of time it will give you a statistical edge. Better having it than not!

The Federal Reserve yesterday raised interest rates another quarter point. Given the reaction in the fed funds futures, this was entirely expected, but the details are in the implementation note. In this note, I draw attention to the two paragraphs:

The Committee directs the Desk to continue rolling over at auction the amount of principal payments from the Federal Reserve’s holdings of Treasury securities maturing during December that exceeds $6 billion, and to continue reinvesting in agency mortgage-backed securities the amount of principal payments from the Federal Reserve’s holdings of agency debt and agency mortgage-backed securities received during December that exceeds $4 billion.

Effective in January, the Committee directs the Desk to roll over at auction the amount of principal payments from the Federal Reserve’s holdings of Treasury securities maturing during each calendar month that exceeds $12 billion, and to reinvest in agency mortgage-backed securities the amount of principal payments from the Federal Reserve’s holdings of agency debt and agency mortgage-backed securities received during each calendar month that exceeds $8 billion.

Normalization started in October 2017 with the $6/$4 billion in maturities. The new information is the step-up in January 2018.

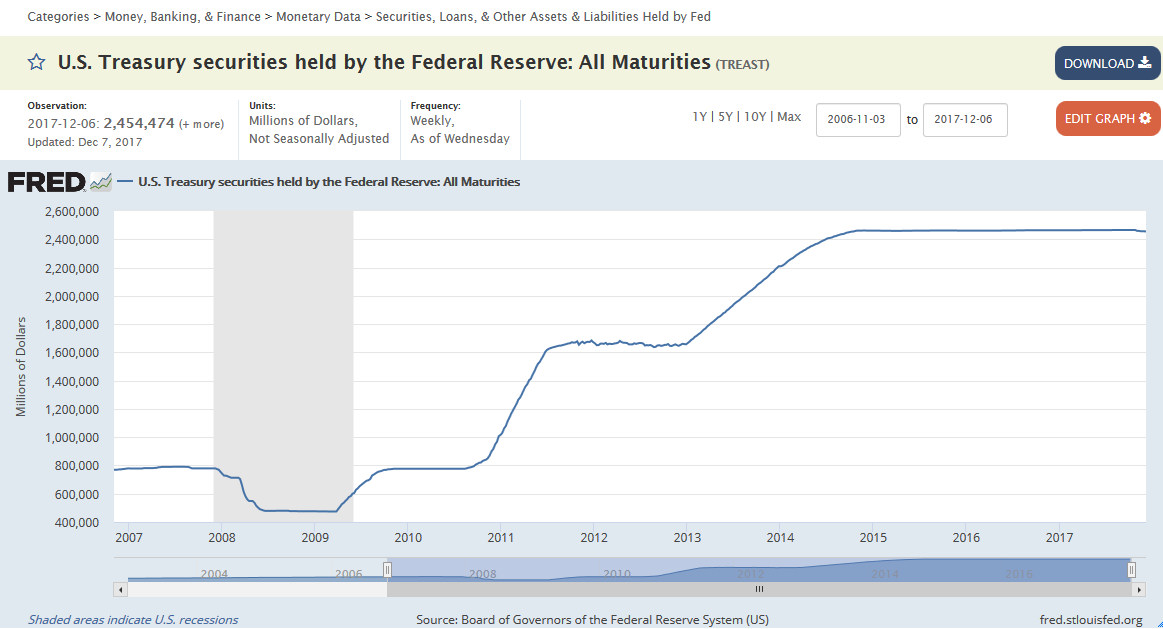

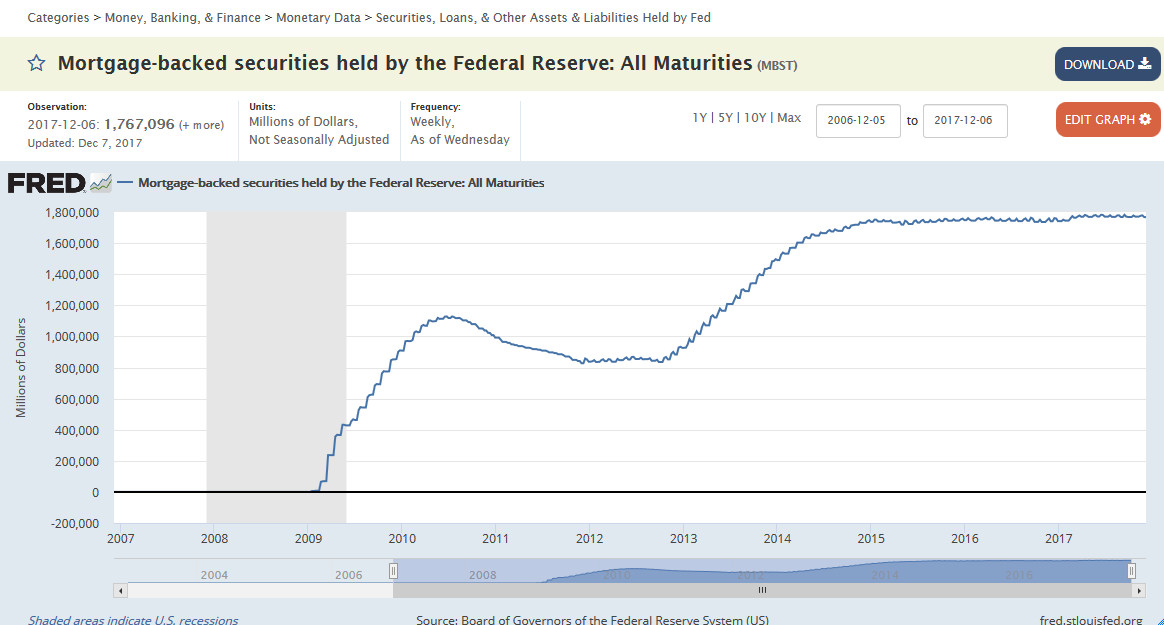

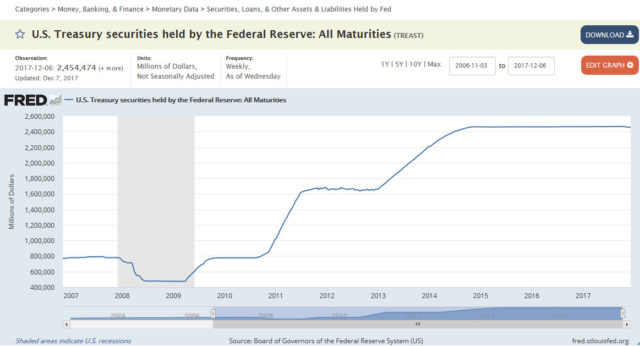

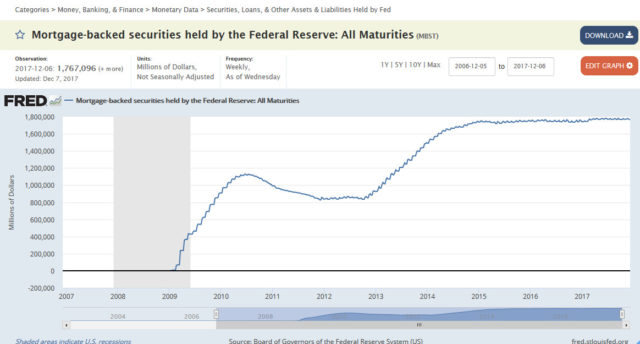

We look at the Federal Reserve’s actions since 2007 and observe during the economic crisis they have pumped a gigantic amount of money into the economy (mostly held up in banks, but still available nonetheless):

(On the top graph you can see a tiny, tiny dip in the holdings on the right hand side – this is the start of the “normalization”).

(If you wish to play with the data yourself, just go to https://fred.stlouisfed.org/categories/32218 and have fun).

As of today we have 2.454 trillion dollars of US treasuries held and 1.767 trillion dollars of mortgage-backed securities. The mortgage-backed securities are an artifact of buying off garbage assets from banks that were afraid that securitizations of such debt would fail – the federal reserve essentially back-stopped this marketplace until it normalized (and given real estate valuations, it has mostly succeeded in doing this, and more).

The point here is that there is $4.221 trillion in cash floating around, mostly in the vaults of banks, but this money has been creeping its way into the asset markets, causing considerable inflation of asset prices (but not inflation of consumer prices, which is why the reported CPI is still so low).

The Federal Reserve has been reinvesting proceeds of these securities until now – they will be maturing off another 0.010 trillion in December and 0.020 trillion in January. For the next two months that will amount to 0.71% of the Federal Reserve’s balance sheet. If they keep the January 2018 pace for the rest of the year, it will amount to about 5% of their balance sheet drawn off.

The question that I am asking is when this will have an impact on asset prices. Cash is still cheap to obtain, but clearly it is going to get more and more expensive as the year continues.

For comparative purposes, the Bank of Canada is relatively boring – they hold roughly a hundred billion in government debt. Most of the financial action in Canada is with the “big banks”. The only on-balance sheet action the Bank of Canada took with respect to real estate-related financial activity was the $35 billion they accumulated in securities purchased for resale in 2008, and the majority of off-balance sheet actions were in the form of guarantees during the financial crisis.

My suspicion is that the Canadian dollar will weaken, but correspondingly US equities as an aggregate will have their gains capped. There will of course continue to be opportunities, but the headwinds are starting to build up.