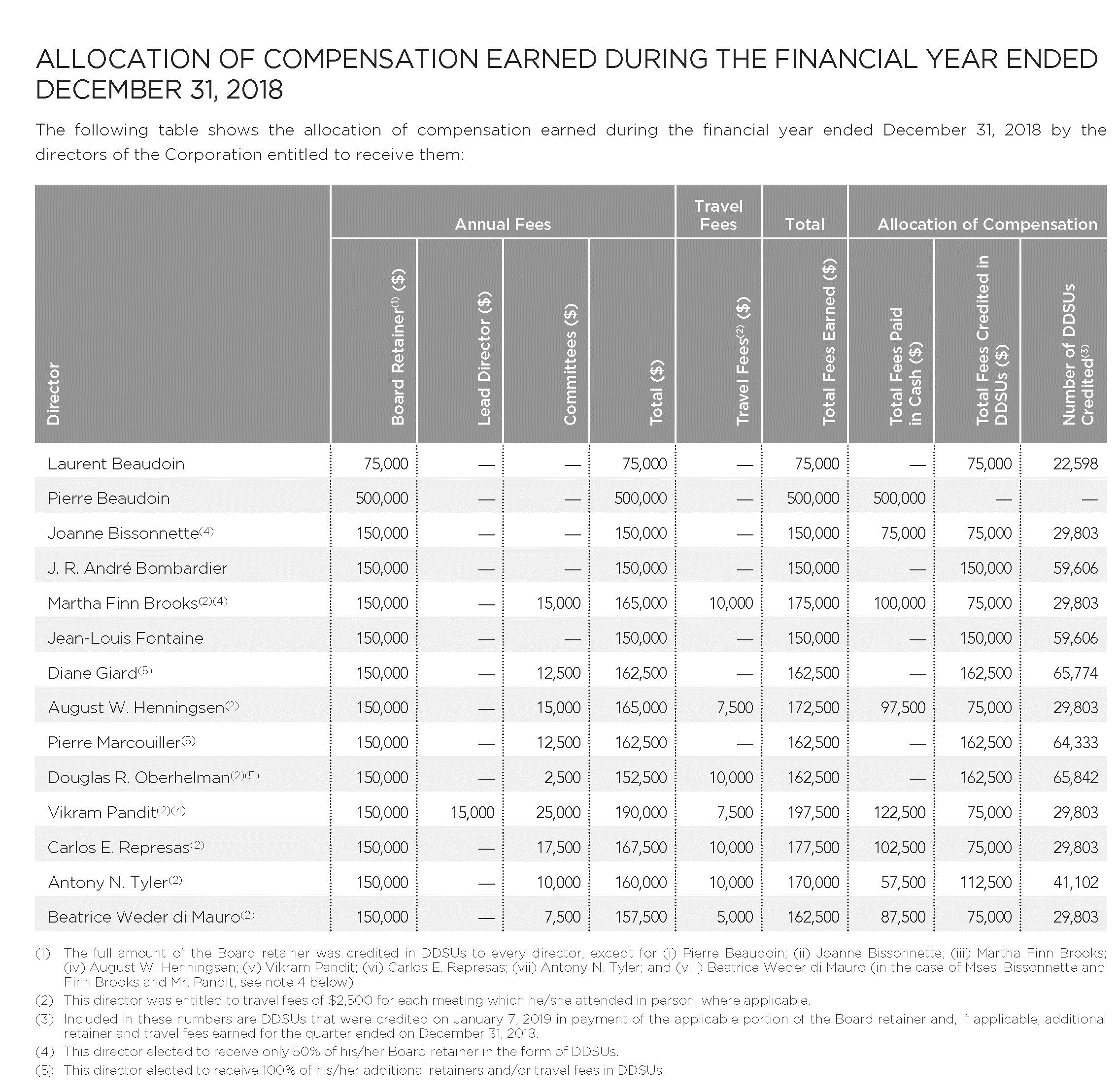

(Part 1 on June 12, 2019; Part 2 on November 16, 2019); Part 3 on February 7, 2020)

This just gets better and better.

On February 6, 2020, after raising CAD$40 million in an equity offering (at CAD$5.60/share with a healthy dose of 3-year warrants at CAD$6.50) they announced they will be repurchasing 30% of their senior secured notes (TSX: GCM.NT.U) which I thought was a good use of capital (their rate of return will be in the teens for this repurchase).

They spun off their Marmato mine into an entity called Caldas Gold (TSXV: CGC) – this mine is going to require a ton of capital investment to ramp up gold production (it produces about 2k ounces per month prior to this investment). On March 17, they announced they spent $2.4 million to purchase off the open market stock in Caldas.

Then things get a little weird. On May 5, they announced they were going to invest in a solar project. The capital cost of this project is $8 million, and “may be financed by up to 70% through local banks”. Although this isn’t going to cost the company too much, it does seem like a deviation.

Then the company on May 11th announced they were proposing to merge with Gold X (which they held a 19% interest in) and Guyana Goldfields (TSXV: GLDX and TSX:GUY), which would have rendered existing GCM shareholders with 60% of the company. The justification was that the mines involved in Guyana were 50km apart and they were able to realize synergies between them. My quick take, without much mining engineering knowledge, was through a simple Google Satellite view of where both mines would operate and I realized that it would be a monumental undertaking to join them together. GCM shareholders avoided disaster on May 25th when there was a superior offer floated by a competing entity and they decided to drop the bid.

So this wasn’t enough. On June 30, GCM announced they invested another CAD$14 million in Caldas to pursue a project called the Juby Project, which is approximately 15km WSW of Gowganda, Ontario. To acquire this interest, they had to give shares of Caldas to the point where GCM has a 57.5% equity stake in Caldas.

This is very puzzling to me since it isn’t clear that the Juby Project will actually generate a dollar for the company. All that was advertised is they will do drilling in 2021, after “incorporating machine learning and other studies”.

Finally, today (July 19), GCM announced they invested another $1.4 million in Western Atlas Resources (TSXV: WA) to bring their ownership to 25.8%.

What’s the conclusion here? Gran Colombia, by virtue of their Segovia operation and a US$1,800 gold price, is making plenty of cash flow. However, they are proceeding to blow it on everything else at a rapid pace, probably for the reason that grades in Segovia are going to decrease and the economic utility of the mine is continuing to drop and they need to start selling promise rather than actual results.

In particular, I believe they objective with Caldas Gold is to get their ownership in the company under 50% so that way they no longer have to consolidate their expenses (and losses) in their main financial statements. Watch out for another acquisition using Caldas stock to achieve this purpose.

I don’t own any GCM stock, but I do own the notes (GCM.NT.U) which I expected to be called away on or shortly after March 31, 2021. I still think at present prices GCM (and Caldas) should be raising equity capital while the going is good. If for whatever reason gold makes a sustained decline, history will be repeating itself with this firm.