There’s a lot that’s happened over the weekend in the Canadian finance world, so I’m just going to do some more quick posts.

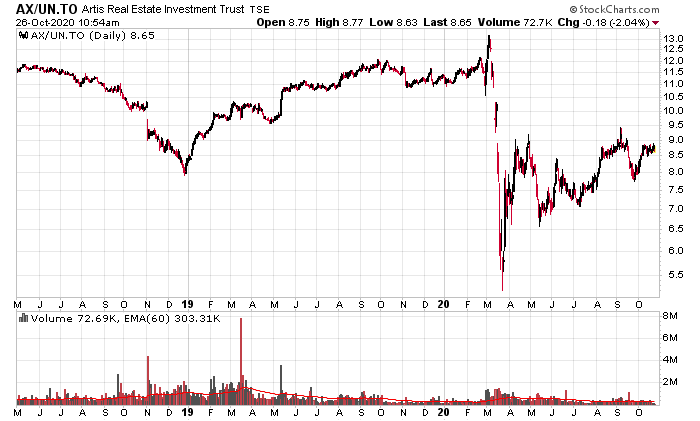

Artis (TSX: AX.UN) has consistently shown on the top tiers of my investment screens, but I’ve avoided them for some reasons that Sandpiper is bringing up – it was very obvious that the top management was mostly entrenched and very handsomely compensated. The property portfolio itself was a hodge-podge and did not seem in any manner to be exceptional (either negatively or positively), with roughly half of it in the USA and half in Canada (by NOI), and mixed usage.

A couple years ago (November 2018), Artis invoked a somewhat different capital allocation strategy, where they cut their distribution by nearly half and initiated a common unit buyback, coupled with asset divestitures. This threw away a bunch of capital in exchange for increasing the debt. One act of capital allocation lunacy was throwing a ton of money away by redeeming their G-series preferred shares for par (June 2019) when the market value was around 80 cents on the dollar.

Artis almost managed to sell itself off, highly rumoured to Morguard (March 2020), but this thing called COVID-19 derailed things. There was also clear disagreement on the proposed transaction (resulting in a Trustee resigning shortly after). I’d speculate management leaked the news to either kill the deal or to induce higher bidding among the rumoured suitors.

Finally, in September they announced a “debt reduction initiative” (which contradicts the leveraging strategy they took in November 2018) and a spin-off of their retail properties.

This apparently was the last straw for Sandpiper, which launched a proxy battle and had a special unitholders’ meeting called.

Today, Sandpiper announced they have 35% unitholder support for their slate of trustees, which is likely to result in them sealing the deal against management if it comes to a vote in said meeting. Given that 62% of unitholders voted in the September 2020 annual general meeting, controlling a 35% block is likely to be a majority of votes.

Management set a very late date for the requested special meeting (February 23, 2021), which gives them time to maneuver around, but they are likely to make it as painful as possible for the existing unitholder base before they make an ungraceful exit. There is a possibility that they will do a golden handshake deal to end things quicker. Either way, when the change occurs it will take a considerable amount of time for new management to unwind the entrenchment of the soon-to-be outgoing management.

No positions, but this is a fascinating case from a corporate governance perspective.