(Link: BoC interest rate announcement)

The Bank of Canada surprised somewhat with a non-change in interest rates, but giving obvious forward guidance that rates next meeting are likely to head higher. Today’s BoC meeting is coincidentally aligned with the US Federal Reserve meeting, which also held pat, but announced they were going to stop the additional purchases of government and mortgage-backed debt starting in March.

The two key sentences are in the last part of the Bank of Canada statement:

The Governing Council therefore decided to end its extraordinary commitment to hold its policy rate at the effective lower bound. Looking ahead, the Governing Council expects interest rates will need to increase, with the timing and pace of those increases guided by the Bank’s commitment to achieving the 2% inflation target.

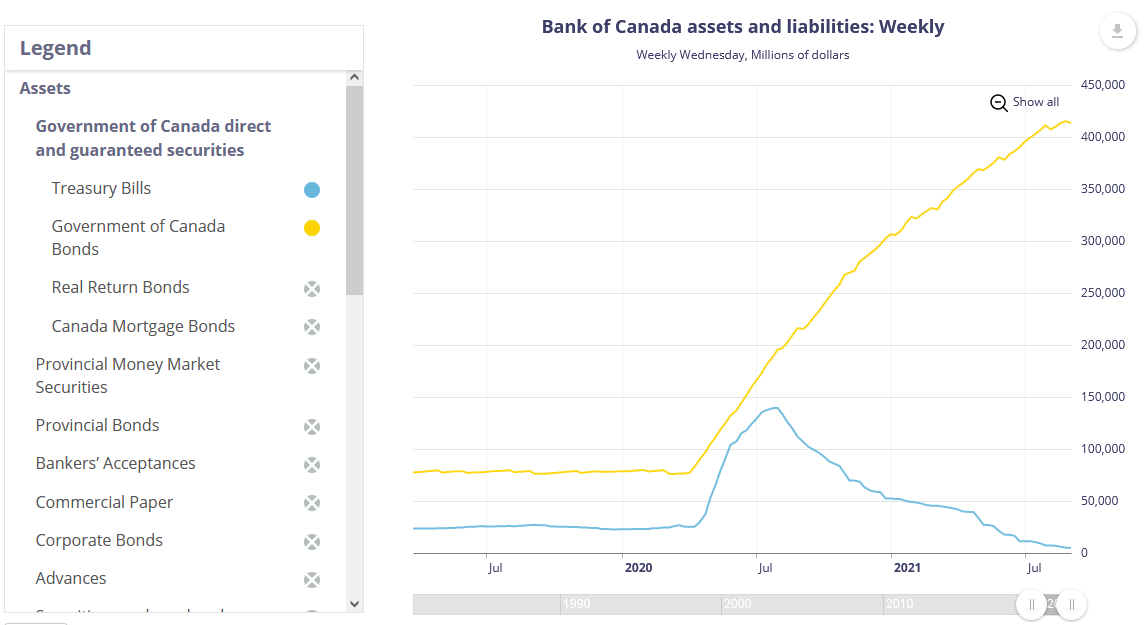

The Bank will keep its holdings of Government of Canada bonds on its balance sheet roughly constant at least until it begins to raise the policy interest rate. At that time, the Governing Council will consider exiting the reinvestment phase and reducing the size of its balance sheet by allowing roll-off of maturing Government of Canada bonds.

This suggests that the target rate will rise (from 0.25% to 0.5%?) on March 2nd, coupled with a slow rollback of their ~$450 billion balance sheet of government and provincial bonds.

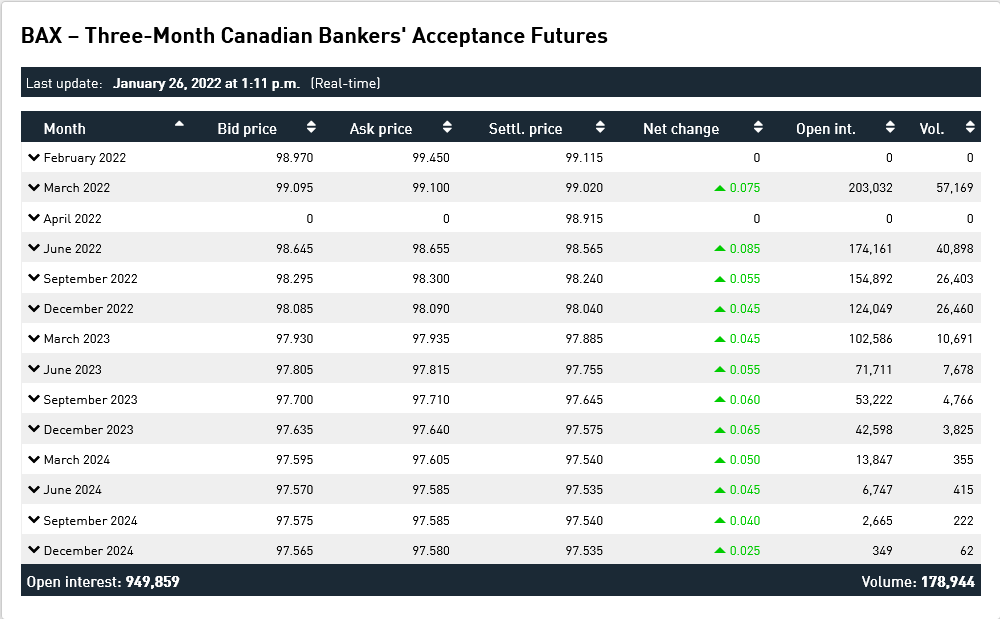

The interest rate futures markets were somewhat surprised at the non-rate rise:

… the prices are implying a 1% increase in rates by the end of the year and another quarter-point in early 2023.

One other observation is that the 5-year government bond yield is down to about 160bps – it got up to about 170bps last week which is the highest it has been in some time (great for those rate-reset preferred shares if they’re due to be reset soon – about 50bps higher than they were 5 years ago).

Within the monetary policy report, some items of note:

The neutral nominal policy interest rate is defined as the real neutral rate plus 2% for inflation. The neutral real rate is defined as the rate consistent with both output remaining sustainably at its potential and inflation remaining at target, on an ongoing basis. It is a medium- to long-term equilibrium concept. For Canada, the economic projection is based on an assumption that the nominal neutral rate is at the midpoint of the estimated range of 1.75% to 2.75%. This range was last reassessed in the April 2021 Report.

Notably with the above, the market is predicting an interest rate at the lower range.

Consumer price index (CPI) inflation is expected to be higher than projected in October. The outlook for CPI inflation in 2022 is revised up by about three-quarters of a percentage point to 4.2% and remains unchanged in 2023 at 2.3%. This upward revision mainly reflects larger impacts from various supply issues, notably those affecting shelter costs and food prices.

The projected CPI will continue to make headlines as the monthly reports come in. Considering the huge price spikes on the inputs to consumer supply (energy, wood, metals, etc.) it is difficult to see how costs will not be rapidly increasing in the future – especially considering the other component – which is human know-how – will be rapidly rising in price as well, likely in excess of commodity prices themselves.

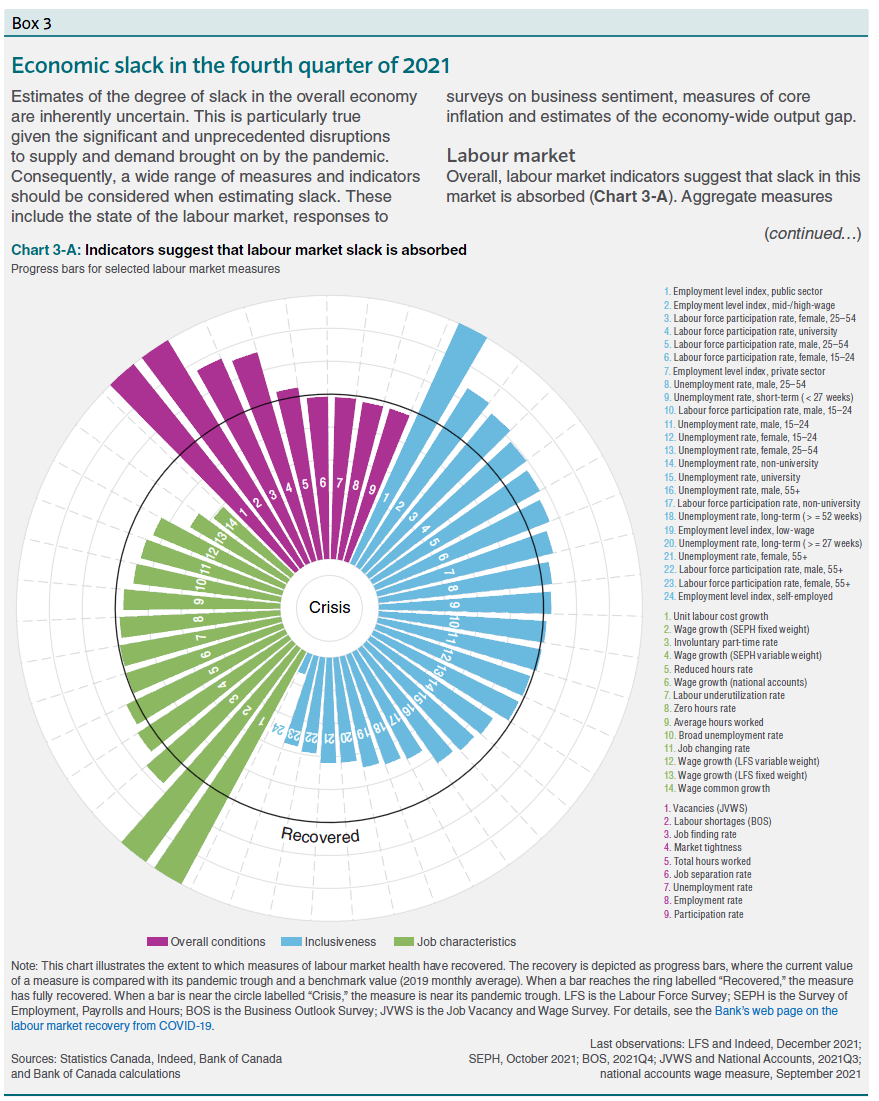

And in what I consider to be the award for the month for the “most unnecessarily complex data visualization”, we have the following gem:

Should anybody be shocked that the purple #1 (upper-left hand side) represents “Employment level index, public sector”?

Here is my take-away: The Bank of Canada is heavily anticipating that things will ‘correct themselves’ through two effects – supply chain resolution, coupled with restoration of global conditions (allowing for exports). They assume domestic spending and consumption will resume as the Covid effects abate, and this will drain the accumulation of savings that were distributed in the past couple years.

I don’t see it this way. The separation of employment characteristics, for example, by age/gender and “public sector”, and “mid-high wage”, does not tell the story at all. It is very much unexplained (at least in the eyes of the Bank of Canada) why there are persistent labour shortages. The most obvious explanation is that what is being offered vs. the headaches of employment compared to what such employment purchases is out of proportion. In other words, wages need to rise dramatically, or what the existing wages can purchase need to increase – the latter case is not going to happen due to continual monetary debasement. People are basically deciding to exit the game – and some perhaps are becoming full-time cryptocurrency traders.

The best thing the central banks can do is engage in a massive monetary draining. The bitter pill would last a couple years, similar to what former FOMC chair Paul Volcker did when he raised interest rates into the double digits in the late 70’s and early 80’s. This facilitated a monetary cleansing. The central banks will not do this, one reason being it would collapse the asset markets and given the amount of debt that is collateralized by such asset values, will cause a huge amount of financial disruption.