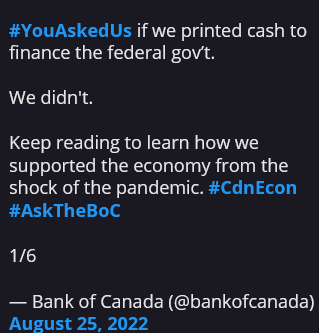

Right on the front of the Bank of Canada website:

A lot of press was made about this, and the distraction phrase here is “cash”. Yes, they did not print cash, but they sure as hell injected a bunch of money into the system in the form of bank reserves!

The logic is as disingenuous as writing the following:

“#YouAskedUs if we killed kittens to finance the federal gov’t.

We didn’t.”

The original inception of the central bank is that it is supposed to perform independently of the government to fulfill its mandate (which is set by the government and is currently to maintain inflation at a level of 2%). Independence is supposed to give the central bank credibility, but since we are now in the era of the politicization of everything, the central bank is now playing politics, which certainly won’t help its credibility.

Anyway, back to the present, the Bank of Canada raised 0.75% today, largely on expectations.

Key points in the release, with my comments:

* consumption grew by about 9½% and business investment was up by close to 12%.

It is very easy for consumption to increase this level when inflation is 7.6%! This is a lagging indicator.

* Given the outlook for inflation, the Governing Council still judges that the policy interest rate will need to rise further.

October 26: 0.25% increase to 3.5% unless if something really, really terrible happens in the next seven weeks (say, a stock market crash). The non-market consensus outlook that I’m putting some probability towards is that they will continue to raise 0.25% each meeting until there is the obvious break in demand.

Implications and thoughts

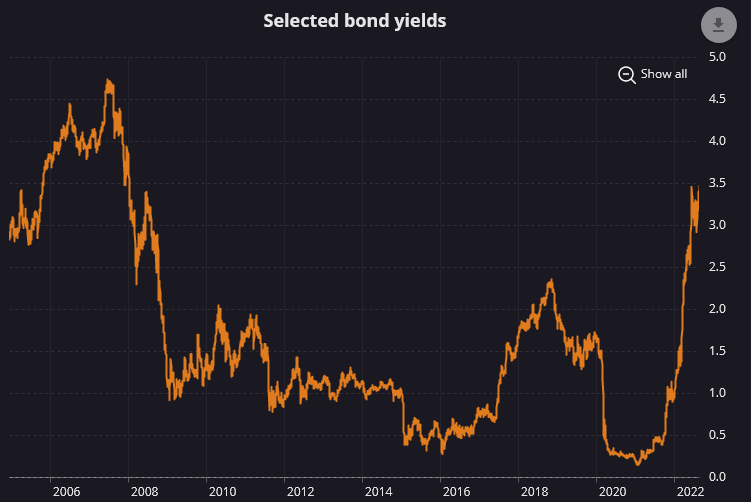

It has been a very long time (about 15 years) where short term interest rates were at these levels, just before the 2008 economic crisis. The risk-free rate is a relevant parameter for most financial calculations. Right now, you can lend the Government of Canada your money for a year and receive a 3.75% guaranteed (nominal!) return. When going out to the corporate bond market, this represents an effective floor on an investment – why bother lending your money to Nortel or Shopify at 3.75% when you can just do it with the government for zero risk?

One reason could be that the corporate world will give you a return for longer than a year – and indeed, a 5-year government bond now yields 3.3%. The question of where long term interest rates go from here is a fascinating one, but if we ever return to the zero-rate environment again, a guaranteed 3% return is golden.

It is instructive to look at the progression of quantitative tightening. December 22, 2021 was the peak of Bank of Canada holdings of government bonds, approximately $435 billion. There is also a (relatively) small amount of provincial and mortgage debt on the books, but we will focus on the bonds. As of August 31, 2022 the Bank of Canada holds $381 billion ($54 billion or 12%). We have data on the “Members to Payments Canada” (bank reserves held in the Bank of Canada) – a reduction of $78 billion there. There’s a $24 billion gap there. What happened?

One factor is that the Government of Canada has been raising more money than expected. Their net cash position with the Bank of Canada rose $30 billion in the prevailing time period. On the fiscal side of things, there is much less pressure on the financial markets to raise debt capital simply because tax revenues have been skyrocketing – this is one of the effects of inflation – everything is valued with nominal dollars. This fiscal cushion gives monetary policy some extra runway before having adverse effects on the longer term interest rates. The government will continue to roll over its debt at higher rates of interest, but they have a very large cash cushion to work with, and if the indications suggest, they will be reporting a significantly lowered budget deficit when they do the fiscal update this November (just in time for more spending to “alleviate the cost of living”!).

What will this mean for the equity markets and asset markets in general? Tough times! It is much, much more difficult to make significant sums of money in a tightening monetary policy environment. Instead of the customary multiple boosts, returns (if any!) will likely be much more correlated to traditional metrics, such as net income and free cash flow, and any gains in corporate profitability will likely be offset to a degree by the P/E multiple compressing due to the risk-free rate rising. Be cautious.