I have been saying here since January 2016 and repeating ever since that Donald Trump will become the next president. Friends of mine will know the words out of my mouth back in August 2015, where I said “not only will Donald Trump win the Republican nomination, but he will become the next president of the United States” – and everybody else started laughing. “No, I’m serious! You laugh today, but just wait and watch”.

Making these sorts of predictions looks easy in retrospect, but there is a lot of genetic psychology that makes it quite difficult to be the one to stand out in a crowd with a very unconventional viewpoint (especially in a country where basically 90% of the people supported Hillary). Either you are regarded as crazy (as my friends clearly did), or shunned, or both. The funny thing is even when you are proven correct, those attitudes generally don’t change much. The only solace on marketable pieces of information such as this (or a lot of what goes on in the financial marketplace) is that correctly contrarian viewpoints tend to make a lot of money.

The markets have basically V’ed since the election (and indeed, I kept a real-time chart of the S&P 500 futures on my desktop as the election results came through, and it was very impressive how trading took it down and up on the returns of various polling stations in key states like Florida).

But there are some macroeconomic parameters that need to be factored into a Donald Trump presidency. While the US system is designed to make sure that you can’t enact too much change with a stroke of the pen (the US Constitution is an amazing structure demonstrating separation of powers), it is pretty clear that companies dependent on Canadian trade with the USA are going to have a more difficult time if there is any perception of protectionism in that particular industry.

Energy policy in the USA will be fairly obvious – there will be more friendly regulations concerning fossil fuel extraction.

In particular, in the political climate of Canada, Justin Trudeau already has staked a bit of his political credibility on his future relationship with Hillary Clinton, and that has now gone to dust. It will indeed be very interesting to see what happens when Trump wants to renegotiate NAFTA – the impression I will be getting is one if I was in a boxing ring with Mike Tyson.

The other quick conclusion I can reach is that it is more probable than not that interest rates will rise quicker than most people generally realize. My hypothesis for this is that the institutions behind the US Government are quite Democratic-party dominated at present and they will want to hamper anything that will come out of the President’s office. And the easiest way to do this is to starve the nation by raising interest rates. Watch the Federal Reserve this December raise rates.

So in general, we have the following parameters:

1. Sell long-term bonds or anything with medium to lengthy durations.

2. Long US dollars.

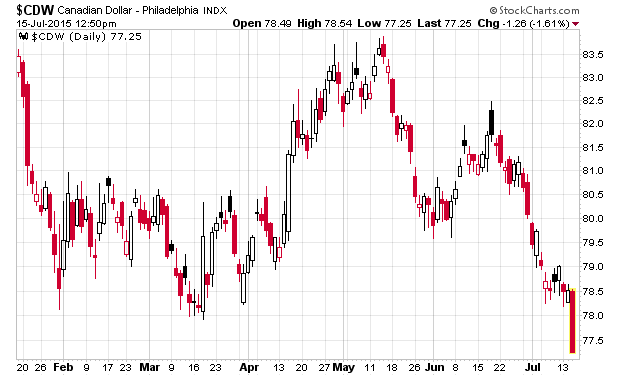

3. Get rid of anything Canadian that is US trade-sensitive.

4. Get rid of anything strongly dependent on Democratic-related domestic subsidies in the USA.

One of Obama’s legacies is saddling the nation with another US$10 trillion dollars in fiscal debt in his 8 year tenure. Even for a nation as rich as the USA, this is a lot of money (about US$30k per capita). This clearly cannot be sustained and unlike other forms of political actions, the direct connection to the standard of life and the increase in the nation’s debt is diffuse and won’t be felt until later – but I suspect the impact of the huge increase in debt will happen over the next few years.