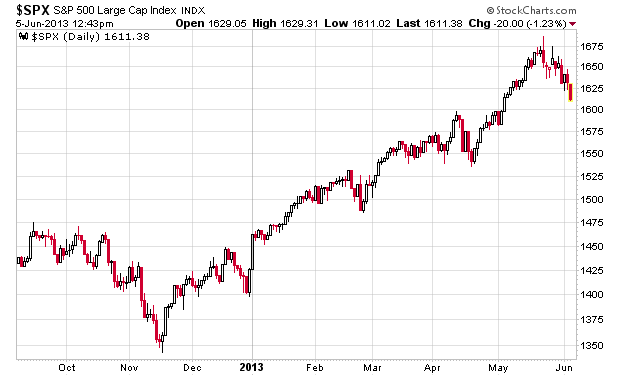

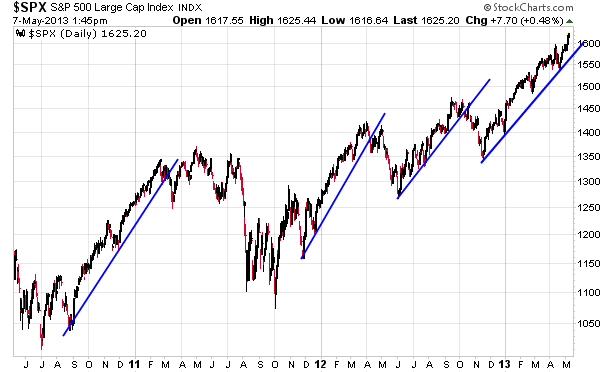

There hasn’t been a heck of a lot to report in the markets lately other than the S&P 500 continuing its rise up as the perception of the recovery continues.

That said, I believe it is unstable and historical norms would suggest that if one applies a bit of regression to the mean that we’re probably closer to the inevitable local high than the local low.

This is exactly why I have been slowly unloading some positions as they have gone higher. I’m no longer in a net negative cash position, and the cash percentage will continue to increase as the market continues to increase.

A few other observations.

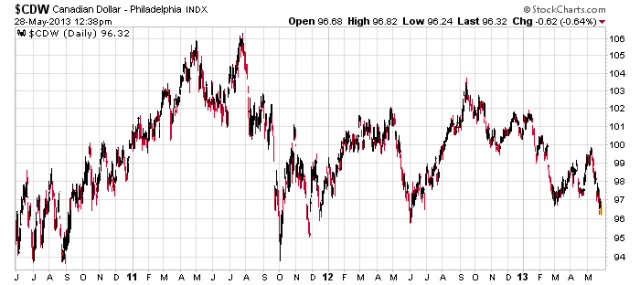

One is that the Canadian dollar is testing lows. They have traded very narrowly since the 2008-2009 economic crisis and they are at the low end of the range. With the perception of Canada being a commodity market and the perception that our interest rates are not going to be rising anytime soon, this may signal a continued decline of Canadian currency relative to the USA.

The other observation are about long-term bond yields creeping up:

I am not sure what to make of this. Certainly bond traders are adding supply to the market and dumping it into equities, but this is the classic “risk-on” type formula where you have anticorrelation between bond prices and equity prices. Right now equity and any non-fixed income assets are winning.

I look at the year-to-date performance which is still significantly positive and my gut is telling me to cash out and call it a day until rainier days hit the markets. This will continue to happen as markets continue to rise.