There is no focus to this post, so be warned. It is mid-way through the 3rd quarter. I’ve been tempted to hit the “sell everything” button and go away for a few months and stick the rest of the cash into some mundane short-term cashable instrument earning 1.5%.

The S&P 500 is up 16.1% year-to-date, while the TSX is up a whopping 2.4%, likely due to the weightings of the commodity market, which have been hacked to death if you were not involved in the sales of hydrocarbons.

I look at the interest rate graphs of both the US and Canadian bond markets – the Canadian bond market is at 2.68% for 10-year money:

The USA 10-year bond is at about 2.83% for the same term. Either way, in both jurisdictions, interest rates have gone up a percentage point in a compressed time period, which is significant. With governments in deficit and high debt levels to be refinanced, higher interest rates means that the interest bite will be higher, and this will continue to act as a serious drag on the economy. Relatively speaking, Canada is better positioned to weather this than the USA, but Canada is more reliant on the commodity market, which does pose some concentration risk.

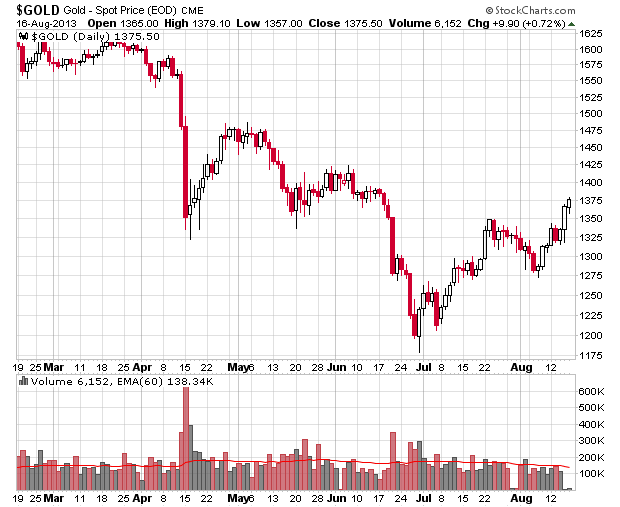

Gold has made a slight comeback from the dead:

I still see significant headwinds for this commodity, mainly due to the appreciation of US currency and the breakage of the notion that gold is any safer than paper currency. The specific moment when I know gold will have finally bottomed is when I see a certain number of “gold for cash” retail outlets finally shut down and put up a “for lease” sign on their door front. Not yet, at present.

I am still very curious whether Fairfax’s macroeconomic call (making a fairly directional bet on deflation in the medium term future) is going to be realized or not. The market is giving Prem Watsa a bit more credit now, likely from his steadfast bet on the collapse of the US housing market. However, looking at their financials, they have virtually given up most of the upside the S&P 500 had over the past year and also are caught on the wrong side of the long term bond market. Their market value of $420/share is well above their book value (less goodwill and intangibles) of $360 and they look expensive at current prices. Still, if they went down some 15% or so, they would be a pretty good way of capitalizing on an economic collapse.

Right now I am sitting on slightly over a quarter of my portfolio in cash. I am waiting patiently. It is in the summer doldrums where relatively few major decisions are made by institutional managers because they are all out on vacation. After they get back in September I am anticipating things will be a little more interesting. However, there are a couple temptations out there which I believe people should be avoiding, most of which I have written about here before:

– The temptation to borrow short at low interest rates and to put the money into higher yielding instruments. Fantastic examples include those in the mortgage REIT categories, such as Annaly Capital Management (NYSE: NLY) or Two Harbors (NYSE: TWO) – sure, both of these give out yields in the low teens, but over the past three months did you want to see 30% of your capital evaporating? Canada’s equivalents, Equitable (TSX: ETC) and Home Capital (TSX: HCG) are somewhat similar businesses (with the notable exception that a good chunk of their packaged securities are backed with CMHC guarantees), but the key difference is that they are not insanely leveraged (just merely highly leveraged).

– The temptation to put cash into the markets just to have the money “working” and generating some sort of return. Sure, you can stick the cash into the S&P 500 and take a chance on it, but again, this is like a less extreme case than the previous bullet point, with just a bit more diversification. Rising costs of money, especially coming from the loosest monetary environment in modern history, will be causing distortions in the marketplace that will likely cause bouts of intense volatility. While there is a chance that some of this volatility might be upwards and you’ll miss out, why take the chance unless if you are targeting that cash into something genuinely trading under fair value with a good margin of error?

Being patient and waiting is boring, but it takes a bit of discipline to just simply wait. There is also the research radar which consumes time, but there hasn’t been much to pounce on other than a couple minor additions that I found in July. I’m not in a position to divulge either, but I was rather steamed that around the time one of those securities was making its all-time lows, somebody posted a rather good description of what I was thinking on Seeking Alpha (essentially the reason why it was truly undervalued and posed an excellent risk/reward ratio) and the security started to bounce back from its incredibly depressed levels and is currently up nearly 1/3rd from its low. What had been a reasonable and thoughtful accumulation (and indeed, when I see the “52-week low” price, that trade was MINE on the buy side), got completely hijacked by this article and pretty much nullified what was going to be a 15% position into a 5% position. Yuck. It pretty much cheesed me off that so much future performance got stripped by a public article when there was so much more value to be harvested from silly panic sellers. Oh well.