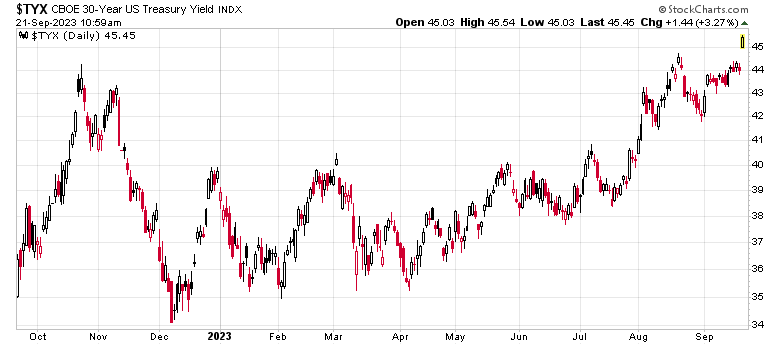

Rising interest rates are going to break things, and this one in particular (Globe and Mail article on negative amortizing mortgages) is going to be interesting.

Snippets:

BMO disclosed that mortgages worth $32.8-billion were negatively amortizing in the third quarter ended July 31. That is the equivalent of 22 per cent of the bank’s Canadian residential loan book. For the second quarter ended April 30, the total was $28.4-billion, equivalent to 20 per cent of BMO’s loan book.

TD had mortgages worth $45.7-billion negatively amortizing in the third quarter, the equivalent of 18 per cent of its Canadian residential loan book. That was higher than the $39.6-billion, or 16 per cent of its loan book, in the fourth quarter of last year.

…

In this year’s third quarter, CIBC had mortgages worth $49.8-billion, the equivalent of 19 per cent of its Canadian residential loan book, in negative amortization. That was higher than the $44.2-billion, or 17 per cent of its portfolio, in the second quarter, according to its financial results.

It appears about 20% of mortgages presently are negatively amortizing. This is presumably due to the interest component of floating rate mortgages rising coupled with fixed payments being insufficient to pay the interest component. This would not apply to mortgages that have their payments vary with rising interest rates.

What will be even more interesting is when fixed rate mortgages renew. Five years ago the lowest rate you could get was 3.19%. Today this is 5.44%. By definition when people renew their mortgages they will continue amortizing their principal, but many of them will be facing increased payments. For example, somebody taking a $1,000,000 mortgage 5 years ago at 3.19% on a 25-year amortization would have a monthly payment of $4,830/month. If, after five years, they wish to renew the remaining principal (approx. $858k) at 5.44% with a 20-year amortization, that monthly payment goes up to $5,843/month. If they wish to keep their $4,830/month payment, the amortization on renewal goes to 29.6 years!

It is a valid point, however, that negative amortization is meaningless without the specific quantum involved. For instance, if your mortgage is negatively amortizing at 5% a year, while your property value is appreciating 10% a year, you are actually decreasing your loan-to-value ratio over time. This headline may be a little less ominous than it sounds without digging deeper into the data – which sadly was not provided.

The debt party will end very badly when real estate valuations collapse (if they ever do). Given the propensity of the Canadian government to functionally open their borders to anybody interested (especially in the form of student visas), the influx of population has provided an increasing level of demand for real estate on a very slowly rising supply base. As long as this remains the case, absent of any dramatic rise in unemployment, it appears unlikely there will be any deep downward catalysts on residential real estate valuations.