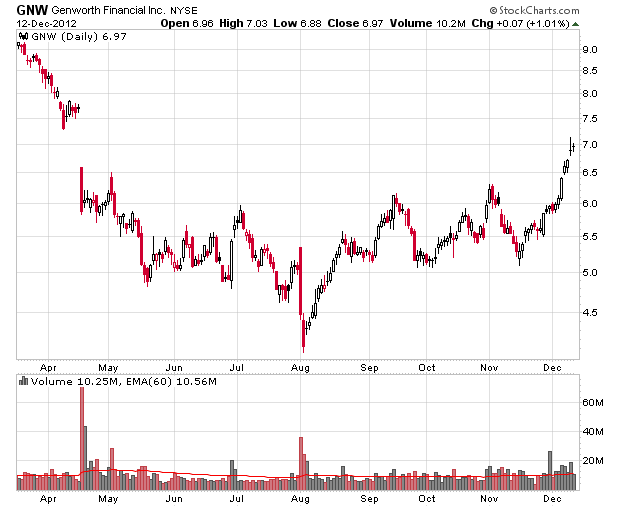

Genworth (NYSE: GNW) shares have risen by about 25% over the past month:

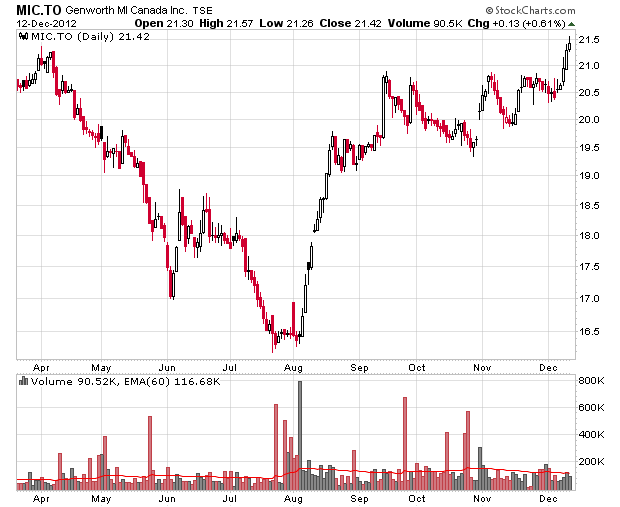

This is presumably due to their reduction of exposure to US mortgage insurance liability. They also recently hired a new CEO. I tried analyzing them earlier when doing my purchase of Genworth MI Canada (TSX: MIC) without coming to any conclusions that made me feel warm and fuzzy, but MIC is also has been a somewhat more muted recipient of positive price action:

Despite all the doom and gloom concerning the Canadian real estate market, at this time I do not believe that this is going to affect mortgage insurance. Increases in unemployment and subsequent employment instability will likely be the precursor to mortgage-related claims. Indeed, delinquency rates at present are considerably lower.

MIC should be trading closer to tangible book value (roughly $28-29/share) which I believe is a more accurate reflection of its market value. At a certain point if Genworth manages to stabilize its financial picture, its options with respect to MIC start to increase. While the market continues to figure out this picture, investors can continue to clip dividends ($1.28/year annualized) from the shares while the company is likely to report earnings around the $3/share range. This recovery in MIC’s market value will likely continue to accelerate if the recovery in the US housing market continues.