Federal Budget 2024 made headlines yesterday, primarily for the reason that the capital gains inclusion rate is increasing from 50% to 66 2/3% for corporations and trusts, and for individuals reporting capital gains above $250,000.

Two broad implications:

1. The concept of “integration” between the income earned in a corporation vs. that earned individually is further broken – it is significantly more advantageous for an individual to take the first $250k of capital gains. Small corporations now have an increased disincentive to engaging in activities that will net them capital gains (the net reward after such an action will be lessened with the increase in the inclusion rate);

2. This change is very obviously a tax grab for estates, and to a lesser degree, will disincentivize sales of non-primary residences.

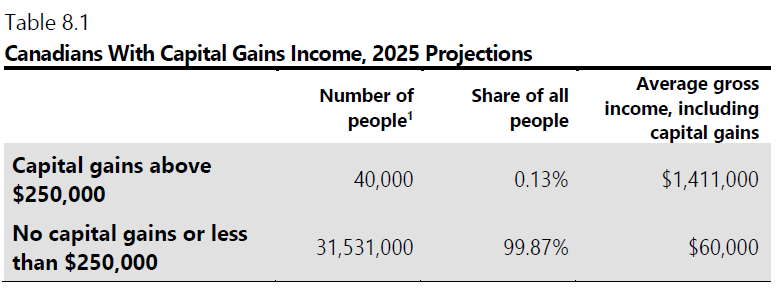

In particular, the cited reason for individuals (“tax fairness”, i.e. an excuse to tax more) was in the following chart:

For most individuals, there are two common triggering events that will cause capital gains going over $250,000: the disposal of a non-principal residence property that has been held for a considerable period of time, and death.

While it is true that Canada does not have an inheritance tax, there is a functional equivalent of it – the deemed disposition upon death.

In Canada, when you die, your capital assets undergo a “deemed disposition”, where it is assumed for tax purposes they are sold and re-acquired at the fair market value of the time of death.

For many people, this will result in a significant capital gain pushing estates above the $250,000 threshold. This especially applies for long-held assets that have had their nominal values increase over time due to inflation, but the real value has remained constant (say a cottage out in Ontario, or shares held in the Royal Bank for the past 20 years). The entire slab of capital gains becomes payable in a single tax year and the only element of taxation strategy is to choose to die early in the calendar year instead of later when you have a bunch of other (pension) income accumulated in the year!

By the time of death, there are few tax planning options to “smooth” this out. You inherently have to predict your passing in advance to construct an optimal tax plan. Needless to say, this is a morbid exercise, but one that potentially made much easier with one industry in Canada that is exhibiting huge growth rates – Medical Assistance in Death (MAID), AKA assisted suicide!