In January, which felt like a very long time ago, I wrote about Torstar. In fact, at one point I owned shares in the company, but during the CoronaCrisis, I dumped my small stake (which to my mystification, was one of the few companies to receive a bid at the time) simply because the rest of the stock market was on sale.

What is ironic, however, is that a couple business days ago, I put in an order to buy in the low 30’s, but never got hit.

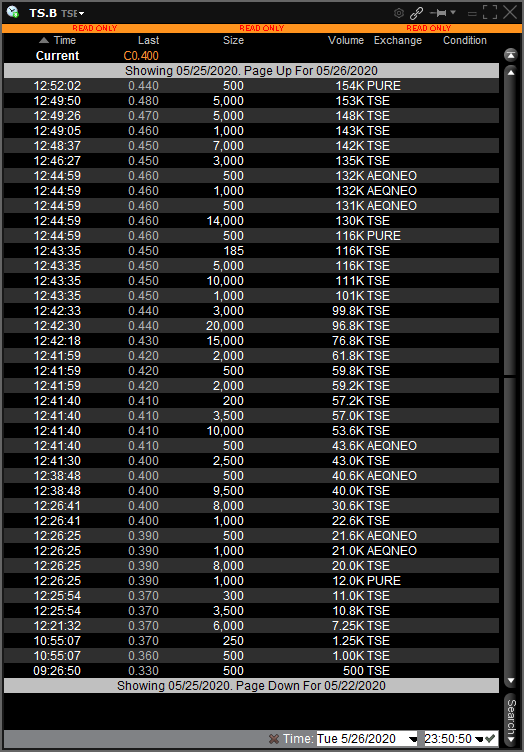

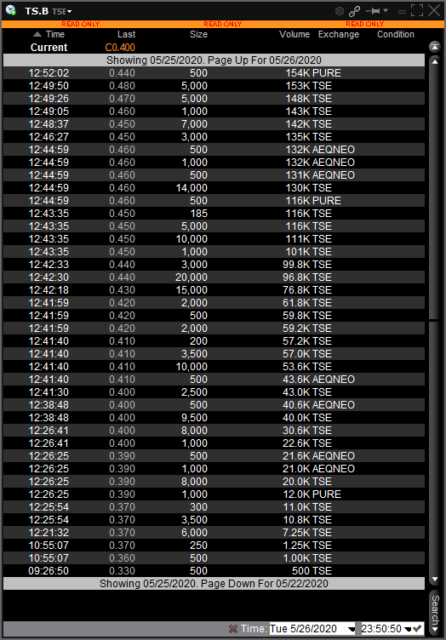

A couple trading days ago (Monday, May 25, 2020), the stock rocketed up from about 33 cents up to 48 cents on about 150,000 shares of volume (this is really unusual for Torstar stock, which is very slow moving):

On first glance, this appears like blatant insider trading. How could it not?

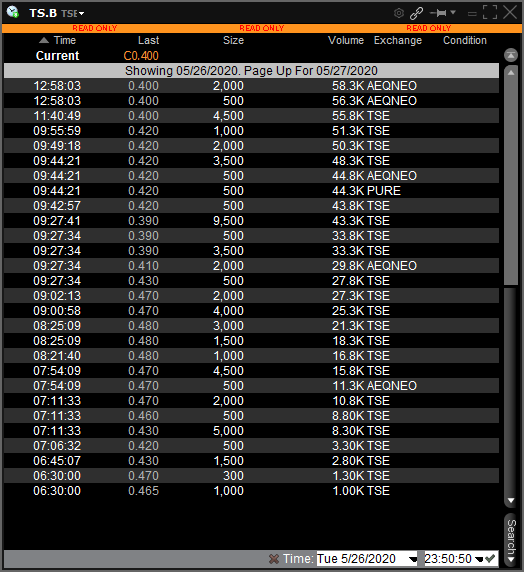

Today (May 26, 2020), the stock buying tapered and some people clearly not in the know dumped stock:

And finally, Tuesday evening, the announcement that NordStar will be buying Torstar for 63 cents per share, cash. NordStar is run by a prominent former Fairfax executive (that still sits on the board). Fairfax already owns about 40% of the non-voting Class B shares and got the consent of the Class A owners, who cashed out at a price that is magnitudes different than how things were a decade ago.

I am guessing Fairfax’s involvement will be acquiring some media clout for a relatively inexpensive price. At 63 cents per share, NordStar is paying $51 million (minus FFH’s ownership, $33 million) in exchange for a company with $69 million in unrestricted cash on their balance sheet, with relatively little on the liability side on their balance sheet. The big black eye is the 56% equity investment in VerticalScope, which is barely generating cash but has a $150 million debt on their balance sheet (I suspect when the ownership changes, that NordStar will be jettisoning this anchor in short order). Operationally speaking, however, I suspect advertising revenues are going to continue to crash and it will be interesting to see how NordStar can re-purpose this investment.

Finally, it isn’t quite clear how much influence Fairfax will have in this, but something makes me suspect there is more behind the scenes.

While I am slightly unhappy that I did not get some Torstar shares in the low 30’s (I was rather late to pulling the trigger), the number of shares I was looking to purchase would not have been material even if I had received an execution on my order. Basically I was caught sleeping and this was another instance of a company that had pulled away from my limit orders.

At least I can take this thing off my watchlist now.