Preferred share spreads (in relation to government) have compressed significantly since last February and it appears that the macro side of the preferred share market has mostly normalized and accounted for the incredible drop of dividends on the 5-year rate reset shares due to the 5-year government bond rate plummeting (0.62% at present with short-term interest rate futures not projecting rate increases until at least 2018).

We are still seeing significant dividend decreases as rates continue to be reset.

I have looked at the universe of Canadian preferred shares (Scotiabank produces a relatively good automated screen) and further appreciation in capital is likely to be achieved through credit improvement (e.g. speculation that Bombardier will actually be able to generate cash indefinitely) concerns rather than overall compression in yields.

As such, one should most certainly not extrapolate the previous three months of performance into the future. Future returns are likely to primarily consist of yields as opposed to capital appreciation.

While investment in preferred shares, in most cases, is better than holding zero-yielding cash (in addition to dividends being tax-preferred), one can also speculate whether there will be some sort of credit crisis in the intermediate future that would cause yield spreads to widen again. If your financial crystal ball is able to give you such dates, you can continue picking up your quarterly dividends in front of the steamroller, but inevitably there will always be times where it is better to cash out and then re-invest when everything is trading at a (1%, 2%, 3%, etc.) higher yield.

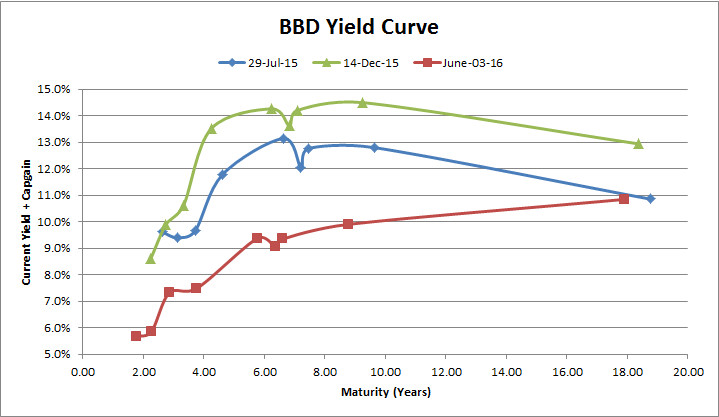

I am also finding the same slim pickings in the Canadian debenture marketplace.

Valuations have turned into such that while I’m not rapidly hitting the sell button, I’m not adding anything either and will continue to collect cash yields until such a time one can re-deploy capital at a proper risk/reward ratio. If I do see continued compression on yields I will be much more prone to start raising significant fractions of cash again. Things are very different in 2016 compared to 2015 in this respect – in 2015 I averaged about 40% cash, while in 2016 I have deployed most of it.