I note that the market has basically baked in a guess that the Canadian Budget 2017 is not going to be very happy for mortgage insurance:

We’ll see in less than an hour!

Canadian Finance and Economics

I note that the market has basically baked in a guess that the Canadian Budget 2017 is not going to be very happy for mortgage insurance:

We’ll see in less than an hour!

The market has run so dry, it has finally come to this – I’ve had to resort to looking at prospectuses of primary market offerings.

Questrade has a rather interesting link to offerings that they’re trying to peddle to the unsuspecting public. And being the sucker I am for these sorts of things, I glossed through a couple prospectuses.

Hampton Financial Corporation (TSXV: HFC) is trying to raise $20 million in preferred shares (plus warrants on their common shares that are nearly double the current market price). The preferred shares have a perpetual, uncallable (by either side) 8% yield. The head honcho owns a lifetime control stake in the company (and a decent economic interest) and a very sweet-looking employment contract. Try negotiating this on your employer (I’ve replaced the person’s real name with Mr. CEO as I don’t want to foul up his pristine search engine profile on his name):

“In consideration of Mr. CEO’s services, the Corporation has agreed to pay Mr. CEO an annual base salary of $200,000, which is to be increased by a minimum of 25% each year from the first anniversary of the commencement date of the employment and a one-time cash bonus of $200,000 payable at any time during the first year of the executive employment agreement, at the discretion of Mr. CEO. In addition, Mr. CEO is entitled to receive annual bonuses at the discretion of the board which may be paid in part by shares or equity-related instruments of the Corporation and a perquisite package of $24,000 per annum.”

There’s other stuff in the prospectus that is juicy, but suffice to say, I’m not too inclined to support this particular public offering, especially considering they don’t make money and they have about $3 million in stockholder’s equity. They also have some very interesting lawsuits that have judgements rendered which give a very good insight on the culture of the firm.

Who the heck would invest in this? If it actually sells, it’s certainly a sign that the market is willing to pay for anything with yield.

With most of these offerings, keep your hands on your wallet.

(Update, March 21, 2017: At the request of one of the issuers, I have amended this post.)

Pengrowth Energy (TSX: PGF) managed to execute an asset sale on its conventional production property north of Edmonton, the Swan Hills assets for CAD$180 million.

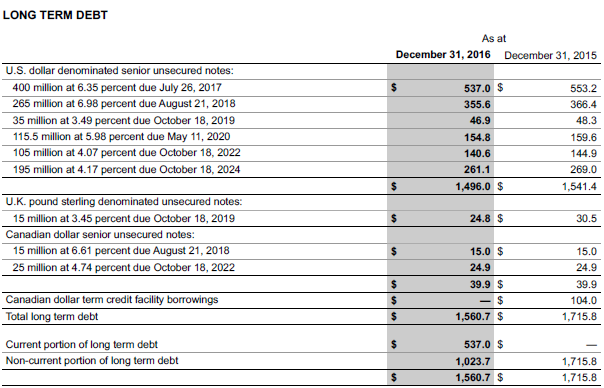

The debt profile at December 31, 2016 looked like this:

Right now the CAD/USD ratio is 0.75.

At the end of December 31, 2016 they also had CAD$287 million cash in the bank, plus another CAD$250 million for the 4% gross royalty sale on their Lindbergh asset.

They will be redeeming CAD$126.5 million in convertible debentures on March 31, 2017. They also have redeemed US$300 million of their 2017 debt maturity, and will redeem the rest after this transaction concludes at the end of May.

The company announced that after this sale, they have a pro-forma net debt of CAD$970 million.

My math suggests that after the 2017 redemption, they would have CAD$57 million cash left, assuming their operations consume zero cash (not a correct assumption!).

Payment of the debt will result in an interest expense decrease of $42 million per year.

They still need to have CAD$368 million on-hand on August 2018 in order to pay off their next debt maturity. It is possible they will run into covenant issues given that oil hasn’t moved around the US$50/barrel mark – their existing senior debt to adjusted EBITDA ratio would be the most material of it. They have about CAD$1.02 billion outstanding and their EBITDA needs to be above CAD$290 million in order to clear this hurdle.

Although the EBITDA value for covenant purposes was CAD$582 million, this is a skewed figure due to the employment of hedging. People not versed in accounting procedures for commodity hedging will have a tough time figuring out the mess, but I will just point out that management closed out their hedges in 2016 (which had been a VERY profitable transaction to them that otherwise would have guaranteed CCAA had they not had the foresight to doing so when times were much better).

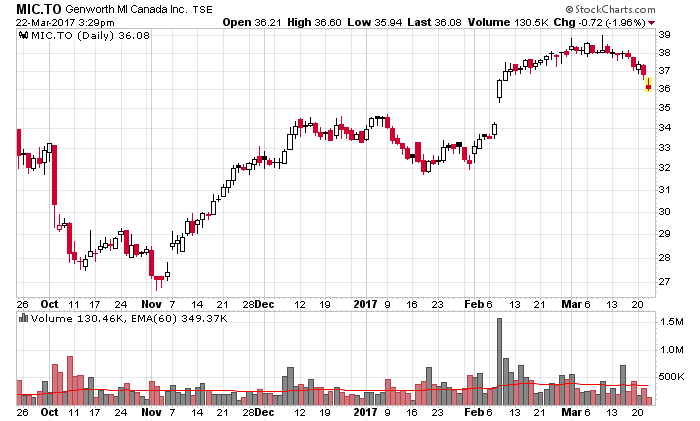

The Q1-2017 report is going to be shockingly positive. Genworth MI (TSX: MIC) used to be my largest holding, but I have trimmed the position (mainly for diversification and deleveraging reasons). It still is a decent size of the portfolio, but not as prominent as it used to be.

My largest position after Genworth MI was KCG Holdings (NYSE: KCG).

Yesterday, near the close of trading, they confirmed that they received an unsolicited takeover proposal of US$18.50-20.00 per share from Virtu (Nasdaq: VIRT), another (very credible) high frequency trading firm. KCG did not file with the SEC.

Virtu filed 8-K with the SEC confirming they “made a preliminary, non-binding proposal to acquire KCG”.

Both entities have been quite silent otherwise. There is likely a lot of backroom jockeying going on.

KCG’s stock shot up from about $13.60 a share to $18/share today on over 6 million shares of volume. The company has about 66.4 million shares outstanding, and Jefferies (a wholly owned subsidiary of Leucadia (NYSE: LUK)) owns 15.41 million shares, and insiders own another 3 million shares, leaving a float of about 48 million shares that can be actively traded. 6.65 million shares traded today and suffice to say there is quite a large amount of speculation about what is going to happen.

My take on the matter is the following (in no particular order):

1. Tangible book value of KCG Holdings is $18.71/share as reported in their 10-K filing. A US$18.50 takeover price would allow Virtu to effectively take over KCG for free. This is the primary reason why I wouldn’t think this takeover would go anywhere as-is. My guess is that if Virtu was serious they would have to offer some equity as well, or some sort of premium to book value.

2. Virtu is a logical strategic acquirer to KCG – the synergies are quite obvious to both businesses. There might even be anti-trust issues with this acquisition.

3. Even though the acquisition at the low price range would be “free” for Virtu, it leaves the question of how they would immediately finance it.

4. The Jefferies control block is vital to the situation – if they can be persuaded to sell out, then management will likely have to follow. The question is whether they are motivated to sell out or not – obviously they will at the right price, but US$18.50 is too low.

5. The CEO was granted a huge amount of options at $22.50/share (priced well out-of-the-money at the time of the grant) and probably doesn’t have much of an incentive at this point to selling out the company for cheap.

6. Operationally, KCG is treading water in terms of cash flow, but this is because of unprecedented low market volatility conditions that is practically the worst environment for the firm (and also Virtu). In more normal conditions, one could easily estimate a value of US$25-30/share for the firm which is where I think management is targetting. They’ll probably sell out at 24ish if the bid got there.

7. Who leaked this unsolicited offer? Obviously KCG did – probably trying to drum up any counter-proposals out there as there are some other financial institutions that would be interested in acquiring the business. Perhaps management knows the end-game is nearing and this was a last ditch attempt to prevent a forced merger.

The decision forward is a high-stakes game for a lot of participants!

Disclosure: I own common shares of KCG, call options, and also their senior secured debt. Sometimes you really do hit the lottery in the marketplace.

Reading press releases like this one makes me quite happy to not being an index investor:

SMITHS FALLS, ON, March 10, 2017 /CNW/ – Canopy Growth Corporation (TSX: WEED) (“Canopy Growth” or “the Company”) today announced that by being added to the S&P/TSX Composite Index, it has achieved another major “first” in the cannabis industry. Management expects this to drive liquidity and increase the percentage of institutions holding Canopy Growth positions. In short, more investors than ever will be buying and holding WEED.

It is pretty obvious that future outsized gains to be made in the marketplace are going to be in companies that are not in the major indexes.