Enbridge Enterprise Partners (NYSE: EEP) is an MLP that owns two oil pipelines – The Lakehead Pipeline system (primarily Line 3), which connects the Northern USA (via a Canadian pipeline) to Chicago/Sarnia, ON and a partial ownership in a smaller feeder pipeline that connects the North Dakota Bakken shale to the aforementioned line. Strategically it is a very important pipeline for Canadian oil distribution. They also own a storage facility. EEP is controlled by Enbridge (as general partner), and Enbridge owns (through a moderately convoluted structure) about a 1/3rd economic ownership in EEP. They did a restructuring of the partnership in 2017, and the new structure gave the GP 13% of distributions above $0.295/quarter to $0.35/quarter and 23% above this in the form of Class F units. The GP receives a flat rate of 2%. The current distribution is $0.35/quarter.

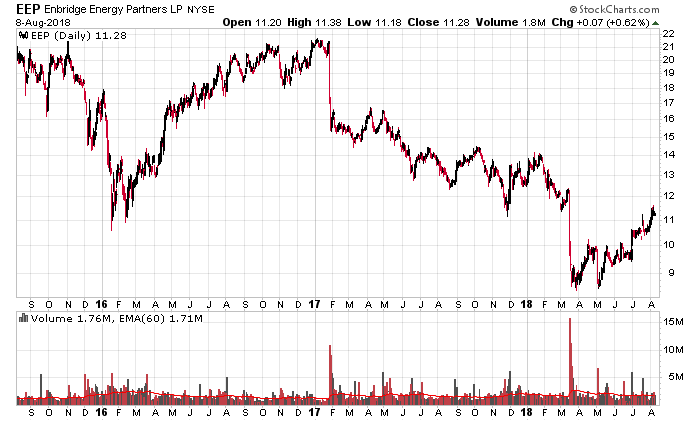

When reading the chart below, it is instructive that EEP reduced distributions from $0.583/quarter to $0.35/quarter on April 28, 2017. The big drop in January 2017 was the announcement that initiated the strategic review. Before this point, EEP was trading at about a 11% distribution yield and after the April 28, 2017 announcement it was trading at about 9% (incorporating the reduced distribution). These yields should be taken into context of a flat-growth entity.

EEP was a dumping ground for some US-based assets for Enbridge and a logical candidate for the MLP structure. This has become less “politically correct” in the financial realm as now the US has enacted a significant corporate tax decrease and also the FERC rulings that I have been writing about earlier.

The large risk for EEP was the approval of its aging Line 3 pipeline in the state of Minnesota. It is an aging pipeline and without state approval to replace it, EEP would have been in serious trouble especially considering the existing line runs across a (hostile to Enbridge) US Native Indian Reservation on a land-lease that expires in 10 years. The new proposed pipeline skirts the reservations. The big hurdle for this pipeline was cleared on June 28, 2018, which the market was pricing considerable risk due to the obvious politics of pipelines and also an administrative judge’s ruling that the pipeline should be replaced along its present route rather than what the company proposed (and Enbridge should be quite relieved that the Minnesota Utilities Commission rejected that ruling when making their decision).

That said, after the initial March FERC ruling, EEP units have crashed even further than its previous valuations. They were as low as $8.50/unit (or about 16% yield on distribution) but now are trading at a more reasonable 12.5% yield on distribution.

I will point out that retail MLP investors are typically focused on distributions and not total return. MLPs that retain earnings in excess of distributions are effectively passing on that extra retained income to their unitholders – i.e. unitholders pay income taxes on that income, but they do not see the cash from the investment (unless if they sell units in the market). This is not dissimilar from dividend equity investors – if the company retains earnings instead of issuing dividends, the shareholder in theory can “create” a dividend for him/her self by just selling the appreciated stock and nobody is for the worse if you ignore taxes.

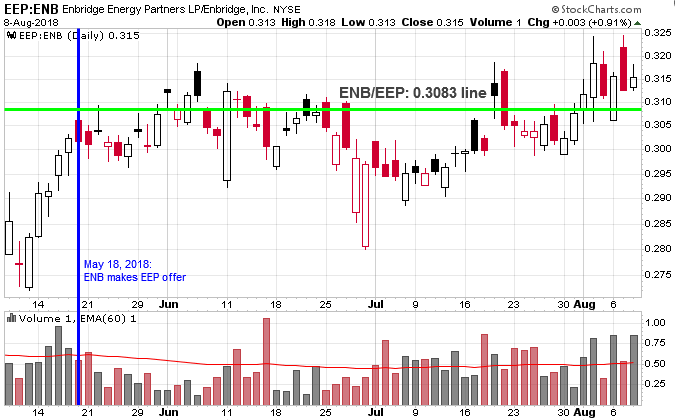

On May 18, 2018, EEP announced they received a proposal from ENB to take over EEP for 0.3083 shares per unit of EEP. The announcement was made on the morning of May 17, 2018 by ENB. They are trying to take the Line 3 system for a much cheaper valuation than it has been trading at historically. Looking at the existing trend of trading since then, we have the following ratio of ENB to EEP:

What’s interesting here is that one would think that the internal valuation of EEP is higher after the Line 3 approval. Most certainly if Line 3 was rejected ENB would likely get their desired 0.3083 ratio. The market is slightly speculating that ENB will sweeten – currently the ratio is 0.315, or about a 2-3% sweetening. This doesn’t sound like too much.

The question is now speculation on whether ENB will sweeten the offer as they need to receive at least 2/3rds approval of the partnership in order for the vote to proceed. Since ENB already has a third of the vote, they still need to convince a significant minority that the offer is worthwhile.

Valuation-wise, EEP generated $616 million cash through operations in the first half of the year and spent $333 million in capital expenditures. Distributions totaled $260 million. This can be annualized to roughly approximation of the going-rate for the existing entity (the Line 3 approval will allow for more oil to flow thorugh the pipeline starting 2019 and hence would improve financial results considerably – ENB knows this and wants to take EEP out before this will happen). Units outstanding was 428 million, hence the entity is producing about $2.90/unit in cash or roughly less than 4x operating cash flow. Accounting-wise this is a somewhat misleading positive story because of the non-controlling interests involved in the parent entity’s balance sheet. I will spare the reader the agony of the technical details of what “non-controlling interest” is, but just say that represents the amount that EEP has consolidated on its own books, but is not owned by EEP. This stems from the funding structures how ENB has provided financing to EEP to construct these various projects.

EBITDA on their liquids business for the first half of the year was $793 million. Since the “I” in EBITDA is significant, it should be noted that most of roughly $7.5 billion in debt is financed through various bond offerings with medium to long term duration, plus a term loan facility that is backed by Enbridge. (Note 13 of their last 10-K contains a handy table).

Balance-sheet wise, EEP has net equity of approximately $16/unit, mainly consisting of pipeline construction costs. EEP has agreements with ENB concerning the financing and EEP does have very good access to credit. There is no distress situation at play financially.

Another negative was that the revised FERC ruling will take EEP’s cash down about $90 million on an annualized basis.

The speculation here is that ENB is underpaying for EEP, especially considering that Line 3 revenues are going to be much higher after it is expected to be operating in 2H-2019. Just on distributions alone EEP is trading at 12.5% yield, but there is a lot more potential in the MLP post-Line 3 construction. It is no wonder why Enbridge wants to take EEP over right now.

Back to the valuation, if EEP was to trade at 11% of distributions, they would be priced at $12.70/unit. The level of distributions, however, is an artificial construct. More accurately, it should be judged on the basis of future cash available for distribution. Management has significant discretion to “create” this number (retaining capital for construction, etc.) but the published number for the first half was $325 million (noting actual distributions were $260 million for the same time period). Annualizing this and subtracting $90 million for FERC, if EEP were to trade at 11%, this is a $11.90 valuation. This does not factor in future gains in cash after the new Line 3 becomes operative – i.e. if the MLP is actually a growing entity, it should deserve a higher valuation.

The question then becomes – how desperate is ENB willing to fold everything back into the parent entity, and how willing are EEP investors willing to play a game of financial chicken with their general partner?

On balance, the 0.3083 ratio probably represents a floor and not a ceiling. The offer was made during the depths of the Line 3 regulatory approval uncertainty and having this lifted will probably mean ENB has to pay up a little further to get it done – I’m guessing around $12-13/unit.