There are a few ways that stocks come across my desk. One is running some screens for issuers that fit my desired parameters (small to mid cap, low volume, among other characteristics). Sometimes I just randomly encounter companies that come up on various sector lists. Sometimes I just type in random ticker symbols and examine (seriously – try it). Another way is to go through 13F-HR filings of various fund managers I respect and try to examine some of their holdings.

Most popular fund managers realize that people like myself have parasitic tenancies in investment. Warren Buffett is a great example of this (think about Berkshire’s investment in Amazon).

One of the huge advantages of being a relatively small investor is that you can get in and out of positions without having to go through the pain of combating high frequency trading and the other chicanery of building or disposing of a position. As a result, smart managers do try to obfuscate this information to a degree, so 13F-HR filings are not the risk-free treasure trove of information one would initially suspect.

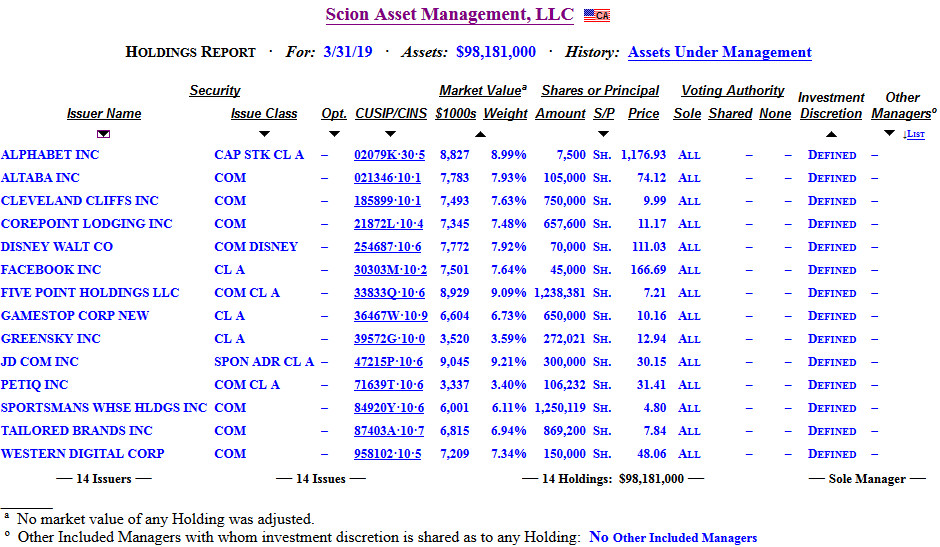

An example today is Scion (of Michael Burry fame) and their 13F-HR filing:

There are 14 positions to deal with, a most manageable number. Note that 13F-HR filings do not have to disclose short positions, nor do they have to disclose securities that are not included in a gigantic listing of 13F-HR disclosable securities, which mainly consist of USA-tradable securities (and foreign securities that trade on US exchanges).

So managers also have the option of trading securities that are not on this list to cover their tracks.

1. Alphabet – Why would I invest in Google? Pass.

2. Altaba – Same, too big. Pass.

3. Cleveland Cliffs – More interesting. Iron Ore producer. Canadian analogy is TSX:LIF which I kick myself today for not investing in early 2016 when it was on my radar and I gave it a thorough look. My knowledge of the iron ore industry is less than adequate, but the financials of Cliffs was less than inspiring in relation to its market value. They may have some competitive advantage by virtue of being the only regional game in town, coupled with Trump’s tariffs, which could bode well for it. But otherwise, don’t know enough to make a decision. Pass.

4. Corepoint Lodging – Hotel REITs are cyclical entities. When room rates rise, everybody and their grandmother seeks to build new hotels and they can be bought at $2-3 million a pop, in markets with relatively low barriers to entry. They are at a high point right now. The next recession will be wiping out a lot of equity value. Corepoint’s financials don’t show an entity making a ton of money on operations and are instead banking on land. Pass.

5. Disney – too big. Pass.

6. Facebook – I don’t even use Facebook. I’m a Luddite. Pass.

7. Five Point Holdings – Land developer, small scale, San Fran, LA and Orange county. Any business doing business in California has tolerance for a massive amount of self-abuse, which gives some incumbency protection. Not a terribly broken business, dual class structure. Relatively new entity, started trading 2017. Income statement showing very lumpy revenue streams. Huge non-controlling interest. Probably not worth further research, but can’t totally dismiss.

8. Gamestop – too many eyeballs on it. Pass.

9. Greensky – Another dual-share structure with a large non-controlling interest, dealing with payment processing and real-time lending solutions. Probably another pass.

10. JD – Do I have any expertise on Japanese online retailing? Nope. Pass.

11. PetIQ – This one is interesting. A lot of money has been lost on the retail side of animal care, but this company deals with the branding and distribution of foods and veterinary care products. Financials are not a complete disaster, but they are in an expansion phase and need capital to do this. The income statement is very low margin and the industry is competitive to the point where they’d need to be the lowest cost producer on the virtue of localized economies of scale – this has been tried before in many instances. Worth further research, but skeptical. Also they announced a major acquisition a couple weeks ago, which usually means huge integration pains for at least a year to come.

12. Sportsman Warehouse Holdings – What’s amazing is how this company can still continue to make money. Lots of money to be made on the equity side if you predict they can keep their gross profits at the levels they are at and keep a cap on their SG&A expenses. Will Amazon/Walmart kill them? Not my cup of tea to analyze, but the stock is trading low enough that there is a compelling case to be made if you have an inclination that they are not doomed to Circuit City-type retail oblivion.

13. Tailored Brands – Otherwise known as the old Men’s Warehouse. Unlike most other clothing companies, Amazon doesn’t really compete very well in the suits category. They had a gigantic amount of debt to work with, but they are still chipping away at it. Valuation is actually not that bad, all things considered! I did look at them many, many, many years ago, so I do have some familiarity with the company.

14. Western Digital – Too big, but a respected hard drive manufacturer. Pass.

So after this screen, I found a few prospects to do further due diligence on.