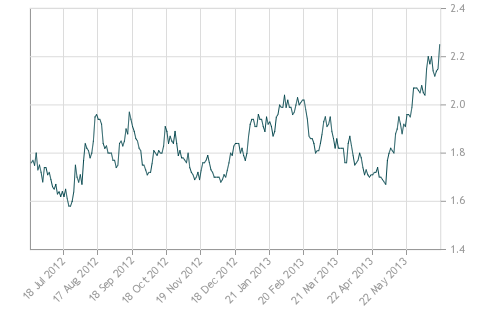

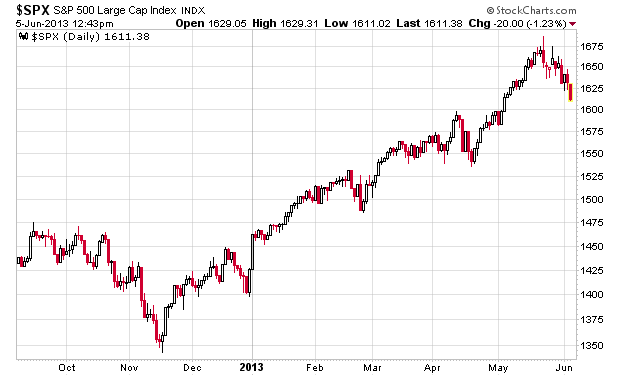

Investors that are doing the simple “borrow at 2%, invest in a fixed income product at 5%” are getting a lesson on leverage today when they see charts like this:

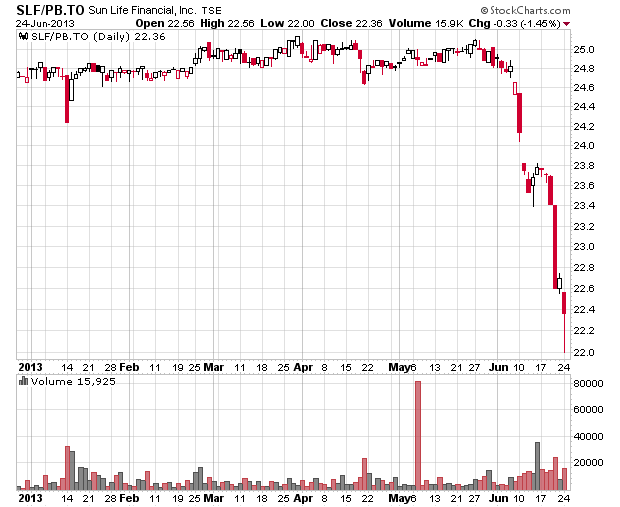

I just chose Sun Life Preferred Series B for just a complete random example and is no way an endorsement of this security – however, this series of preferred shares gives off a lazy 30 cent per quarter dividend and just one month ago was trading near par value, which would have given its investors a 4.8% yield.

Now, investors are waking up to see they have lost 10% of their capital, which is about two years’ worth of yield if the price doesn’t subsequently appreciate.

The odd thing is that predicting when the bottom ends is a very difficult guessing game of how desperate everybody is to liquidate income products in exchange for capital. If people are still leveraged and their equity is running low to the point where they still need to raise capital to maintain their positions, then we will still see further dumping into the market and lower prices.

We do have a good example of what happens when this occurs – in the depths of the economic crisis in 2008-2009, this preferred share traded as low as $13 – or 52% of par value.

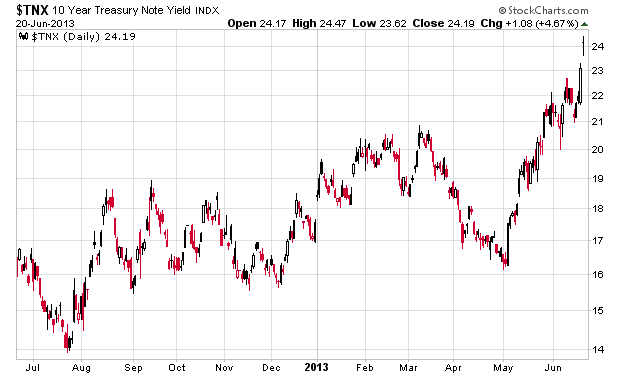

All of this is likely a function of the underlying fixed income instruments (30-year, 10-year treasuries) getting bidded up in a volatile fashion and the subsequent capital losses there are reverberating into the more junior markets in terms of balancing portfolios. In other words, anything with a yield is getting liquified.