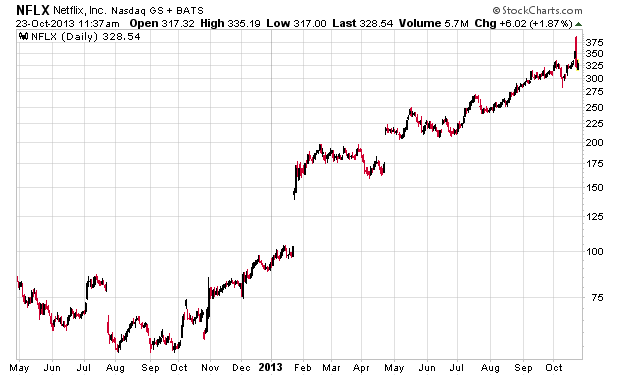

Most people think that good investors are able to buy undervalued companies. People forget that good investors also know when to sell. Take a look at Netflix (NFLX):

Carl Icahn apparently went in at $58/share, and sold half his stake in the $300s.

The headline quote in the media articles:

… as a hardened veteran of seven bear markets I have learned that when you are lucky and/or smart enough to have made a total return of 457 percent in only 14 months it is time to take some of the chips off the table.

I’d say this is a pretty good rule of thumb for anybody to follow if they are so fortunate.

Just as a matter of arithmetic, if you invested $100 in something that went up 457% and then sold half of it, you still have $278.50 worth of something left over, not an insubstantial amount in relation to the original investment. Another way of looking at this is you would have to sell 18% of your investment to play with “house money”, so to speak (although this is a huge misconception in retail finance as there is never such a thing as house money – it is your own!)