There have been drawn out periods where I have done literally nothing and 2014 has had that kind of start for me. Writing about how I am twiddling my thumbs is very unexciting, so I will talk about something which has caught my radar: The Canadian dollar.

Just like any patriotic Canadian, cross-border shopping (and just generally enjoying recreation in fantastic and not-too-contaminated by mass population areas like the Oregon Coast) is something that is easily accessible due to the relative strength of the Canadian dollar.

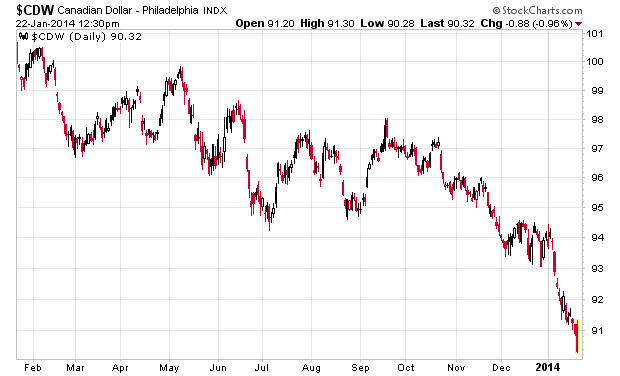

As you can see from the chart above, our purchasing power has just eroded by about 10% over the past year, which is mildly disturbing and makes inexpensive vacation prospects slightly more expensive. When something makes my recreational agenda more expensive, I take notice.

Not helping was today’s announcement by the Bank of Canada, declaring that inflation is “further below” their 2% target, which creates more pressure that interest rates are not going to be rising anytime soon, ergo the currency drops to the USA, which is starting to see signs of their short term rate increasing:

The thoughts swimming in my head is whether the drop in the Canadian currency is a predictive indicator of what is going to happen to the Canadian economy and equities as a whole (adjusting for the impact that they are now cheaper to purchase with US funds!)?

We will see. My market exposure is relatively low and I have not been inspired by anything I have seen out of the marketplace. It might be some time before I write again given this “do nothing” stance.